A Paradigm Shift?

It’s a known fact that the global markets across assets: FX, Bonds, Equities, etc, are run by all mighty powerful algos who are trained using extensive historical data.

These algos use millions of data points and historical correlations to place high-frequency trades to benefit from the incoming macro data.

However, since the last few weeks (and for Gold last 2 years), the correlations have broken for various asset classes.

To recap what’s transpiring in the financial markets:

USD-Commodities -ve correlation

Gold- Real Yields -ve correlation

Yields- Equities -ve correlation

USD-Gold -ve correlation

Yields- Gold -ve correlation

The above historical correlations in the markets are no longer working, and thus, we may be on the cusp of a paradigm shift in the global financial system.

The reasons are plenty, beginning with the fiscal dominance concerns in the US, the extraordinary liquidity pump by Chinese and Japanese Central Banks, and the FX universe upheaval with the sharp depreciation of JPY and CNH.

Further exploring what can be termed the total collapse of fiscal discipline, the US Government decided this week to waive the student debt of nearly 30 million students.

This is a shocking move as the US fiscal position is already in a dire state due to the ballooning peacetime fiscal deficits.

Focusing on appeasement politics in an election year instead of building a fiscal consolidation roadmap will erode the confidence of bond investors who have already lost trust in Jerome Powell.

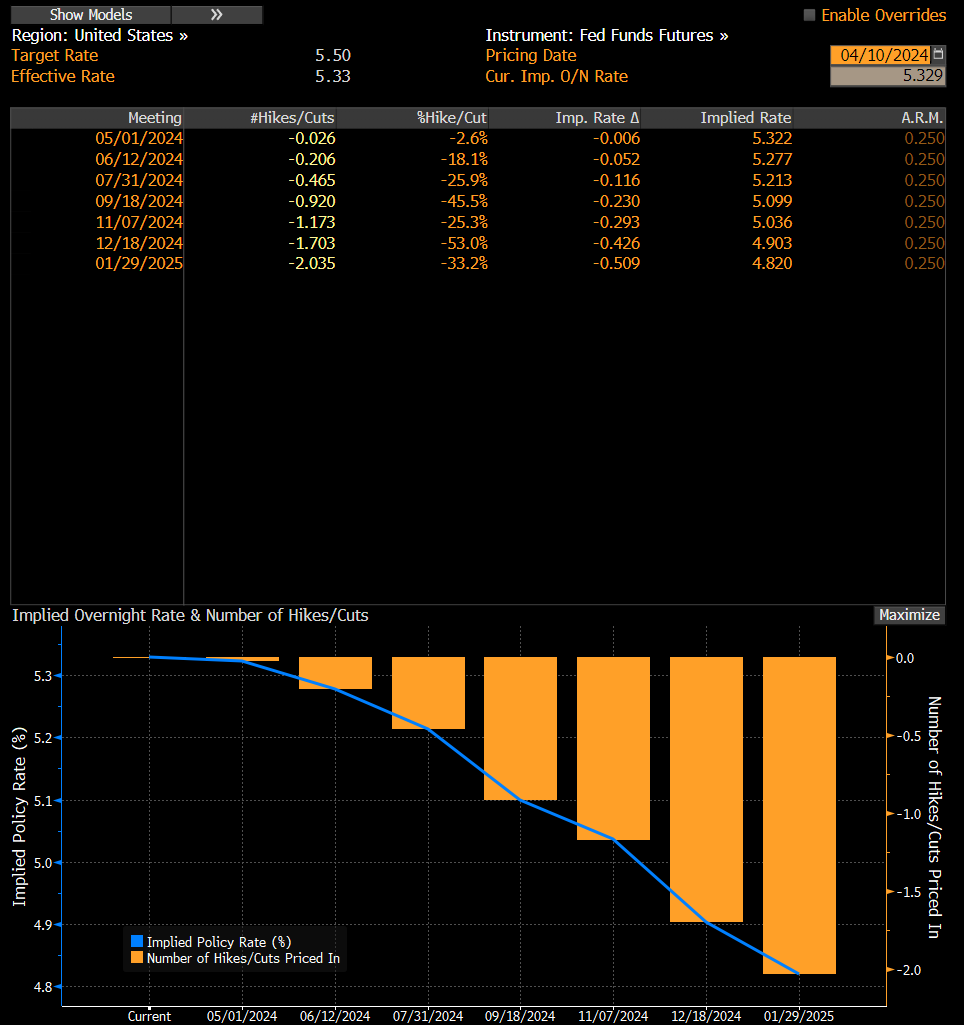

Bond bulls are a worried lot. After the unexpected macro data, the pipe dream of seven rate cuts has now been reduced to just two cuts this year.

With this backdrop, let’s dig deeper into the macro universe and understand the future trajectory of growth and inflation.

US!

The much-awaited data release for the month and the week came in hotter than expected, leading to higher yields and driving the greenback higher to levels last seen in October.

Well, if you are a long-time reader, you would not be surprised about the second wave, as we have been writing since last year.

In fact, we were the first to write about it on Substack in September 2023 (I have removed the paywall for the post).

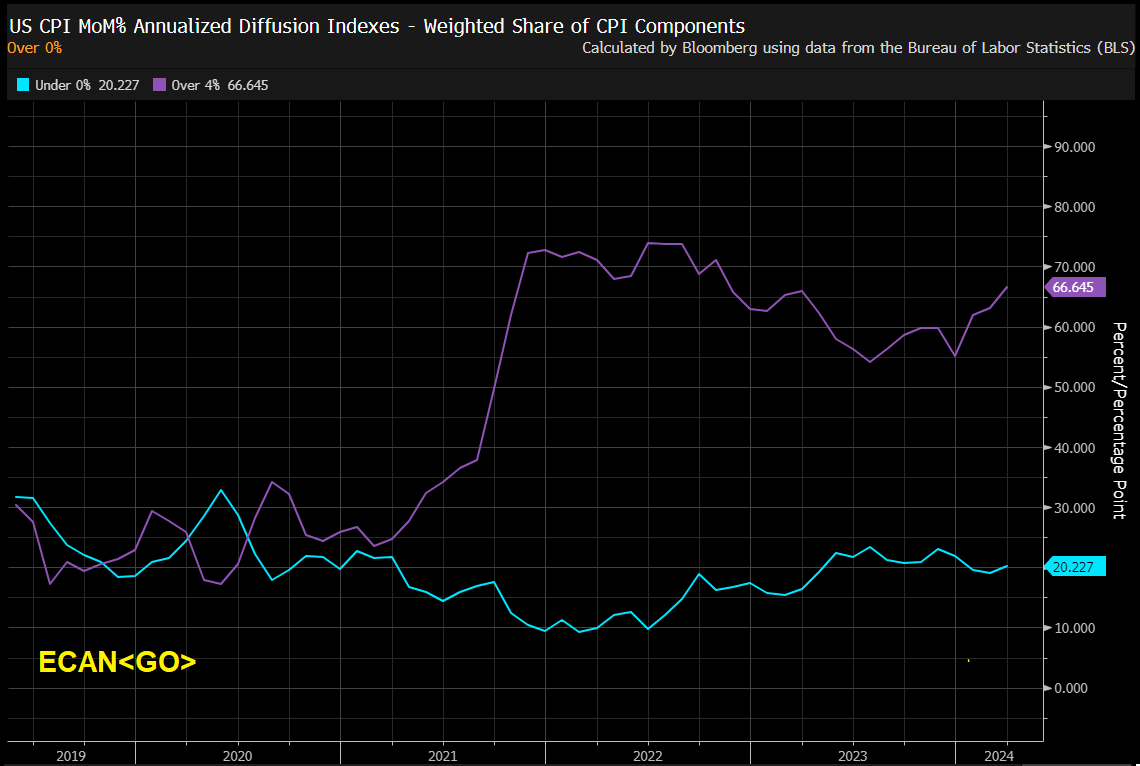

Nevertheless, analysing the data indicates that the disinflation process has completely stalled, with more than 66% of the components now running at a 4% annualised pace.

Furthermore, 20% of the disinflationary basket (less than 0%) comprises core goods, led by used cars and fuel, which will likely bottom as the base effect wanes in the coming months.

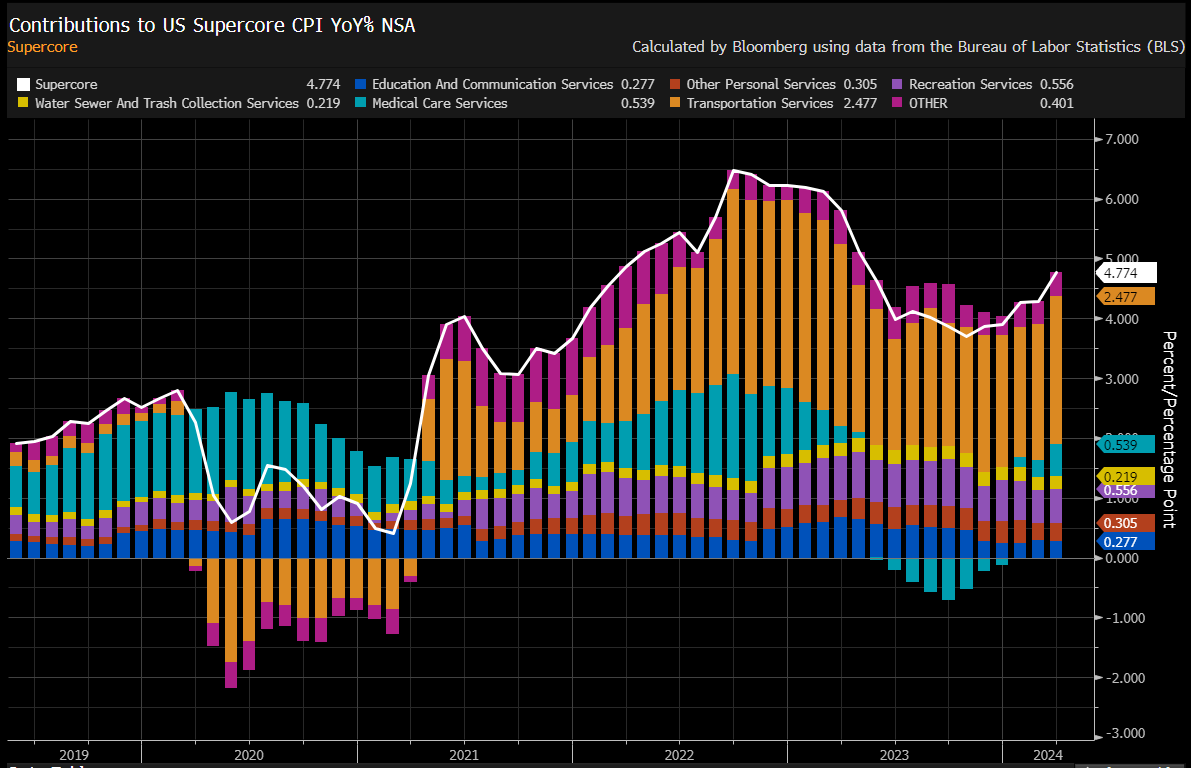

JayPo’s favourite indicator, Supercore (Services Ex-Shelter), which he popularised to justify the hikes, is at uncomfortable levels.

While MoM was scorching hot (annualised at an unbelievable 8%), even the YoY print was 4.77%.

The culprit here is transportation services, which we have repeatedly demonstrated is a result of the rate hikes themselves (a higher prime rate feeding to higher inflation).

Nonetheless, what matters now is the future trajectory of inflation, which looks horrendous.

While the bond market price out cuts, as per our calculations, higher fuel prices and their pass-through, along with the base effect, will lead to

Keep reading with a 7-day free trial

Subscribe to Marquee Finance by Sagar to keep reading this post and get 7 days of free access to the full post archives.