Disruption- PART 2?

The book “Chip Wars” laid the foundation for the mega rally in semiconductors that transpired in the last two years.

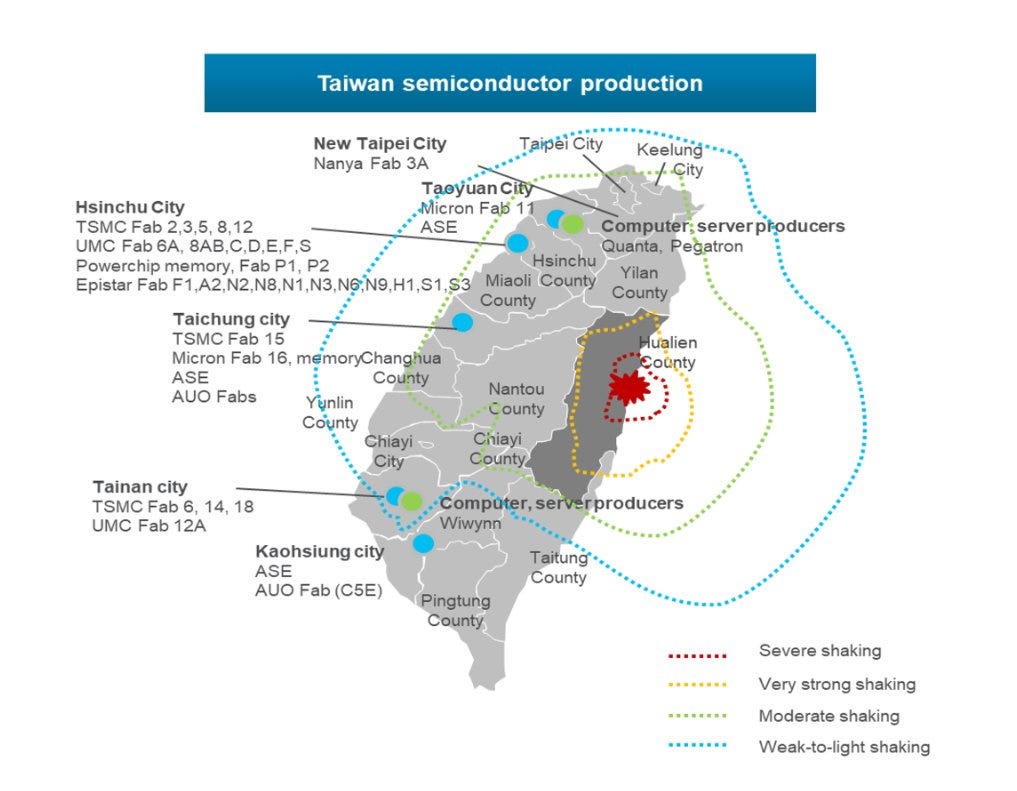

Those who have read the book know that the heart of the semiconductor universe is meticulously situated in the tiny Asian island nation of Taiwan.

Nothing on this planet can match Taiwan Semiconductor Manufacturing Company Limited (TSMC) 's cutting-edge technology, scale, and expertise.

We dumbfoundedly witnessed how the COVID disruption in the critical “Chips” caused months, if not years, of delay in the supply of goods ranging from automobiles to numerous consumer durables.

Unfortunately, Taiwan was hit by a mammoth earthquake this week, which has raised concerns about a potential hit to TSMC facilities.

If the disruption lasts more than a fortnight, we might be heading for a scary scenario of supply disruptions leading to soaring prices “once again.”

As a result, the macro data and the supply disruptions arising from the blockade of the Suez Canal to TSMC’s plants can lead to a severe headache for the world’s largest central bank, which has virtually lost credibility.

Furthermore, the problems have compounded significantly for the Biden administration as geopolitical activity heats up in the Middle East after Israel’s deadly attack on Iran’s Embassy in Syria.

As geopolitical risk premia rises significantly due to the uncertain ME environment, OPEC+ cuts set in, Ukrain’s relentless attack on Russian refineries increases manifold, and the Chinese resort to massive stimulus, oil prices have surged to $90/b+.

Undoubtedly, 2024 is turning out to be a tumultuous year on all fronts.

Analysing the slew of macro data released this week can help us understand the direction of the global economy and its implications for cross-asset performance.

US!

For the new subscribers, ISM Manufacturing is our favourite measure to gauge the cyclical activity in the US.

Though many market participants have recently echoed concerns about soft data (surveys) and claimed that they are irrelevant in today’s services-heavy economy, we remain adamant about using ISM data to determine the stage of the business cycle.

Interestingly, after a 17-month consecutive streak of contraction for the ISM Manufacturing PMI, the headline number finally came above 50, signalling expansion.

Nonetheless, our favourite gauge, New Orders Less Inventories, moved down, indicating that ISM Manufacturing might not sustain higher for long as inventories build up might begin soon (inventories have been contracting for months now).

The shocker, however, was not the beat on the headline number but the significant expansion in the ISM Prices Paid component, which registered a reading of 55.8.

On the contrary, as measured by ISM Manufacturing Employment, the labour market’s cyclical sector (manufacturing, etc) remained in contraction territory, demonstrating that the labour market’s cooling is underway.

The million-dollar question: What’s the trajectory of the Prices Paid or, in other words, inflation?

Well, folks, we believe that the current reading higher was due to:

Keep reading with a 7-day free trial

Subscribe to Marquee Finance by Sagar to keep reading this post and get 7 days of free access to the full post archives.