“The modern theory of the perpetuation of debt has drenched the earth with blood, and crushed its inhabitants under burdens ever accumulating.”- Thomas Jefferson.

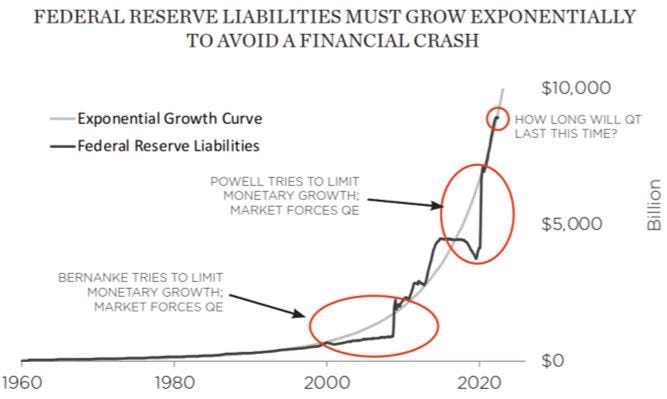

The demise of the “Gold Exchange Standard” in 1971 gave colossal power to central banks to print infinite “fiat” money without backing it with any kind of reserves. The Central Banks have since printed money out of thin air (via various monetary instruments and expanding balance sheets exponentially).

The world’s largest economy encountered a seismic shift post-2000 as the gigantic demographic transition commenced and society started to age.

Nevertheless, productivity gains enabled the economy to survive the stagnation, and GDP growth increased albeit slowly. Still, a confluence of factors such as rising social security costs, defence-related costs (wars), and fiscal sops such as student debt relief led to ballooning fiscal deficit. In short, the doom loop:

Rise in unproductive spending → Increase in fiscal deficit → Funded By Issuing More Debt → The Federal Reserve (CB) monetizing debt → Increase in Money Supply / Expansion of Balance Sheet → Inflation→ Higher Yields→ Higher Interest Cost/ More spending→ More borrowings

But have you ever considered the consequences of the debt binge that the world has now been addicted to?

How did we reach the point where the system will eventually break one day?

Let us start with something interesting that Margaret Thatcher said at Conservative Party Conference in 1983:

“Let us never forget this fundamental truth: The state has no source of money other than the money people earn themselves. If the state wishes to spend more, can do it only by borrowing your saving or by taxing you more. There is no good thinking that someone else would pay, that someone else is YOU. There is no thing such as public money; it’s just taxpayer’s money. Prosperity won’t come by inventing more and more public lavish programmes. You don’t go richer by ordering another chequebook from the bank. No nation ever grew prosperous by taxing its citizens beyond their capacity to pay!”

As the world enters into a demographic time bomb, and the mad obsession with more and more debt reaches record levels, troubles galore for the most indebted country (as % of GDP) in the world.

The Japanese Finance Minister Shunichi Suzuki shocked the world this week when he said:

“Japan's finances are becoming increasingly precarious.”

The Japanification of the developed world, along with countries such as China which is witnessing a rapid decline in working age population, is inevitable.

Today, we will understand the Modern Monetary Theory (MMT), the result of incessant printing in the last four decades, Japan’s upcoming bond market hurdle and what can be the endgame!

MMT: A Brief Explanation and 2020!

The success of capitalism has often been associated with the notion of the free market. The champions of the free-market advocate that the laws of supply and demand drive the economic system. Furthermore, the government in a free market has no business to be in business.

However, to win an election, leaders need free stuff such as social security and healthcare! The only obstacle is that these things aren’t guaranteed unless you go against the basic principle of the free market. Thus, the markets needed to be distorted, and Modern Monetary Theory was born!

Australian economist Bill Mitchell coined Modern Monetary Theory (MMT) in the early 90s. The contours of the theory were developed by economists Bill Mitchell, Warren Mosler, and L. Randall Wray in 1992.

According to Investopedia, the central idea of MMT is that:

Governments with a fiat currency system under their control can and should print (or create with a few keystrokes in today’s digital age) as much money as they need to spend because they cannot go broke or be insolvent unless a political decision to do so is taken.

Some people would argue that irresponsible “fiscal policy” under MMT would lead to high inflation (or even hyperinflation) and the accumulation of enormous unsustainable debt. However, the MMT theorists are of the view that:

The only limit that the government has when it comes to spending is the availability of real resources, like workers, construction supplies, etc. When government spending is too great with respect to the resources available, inflation can surge if decision-makers are not careful.

Taxes create an ongoing demand for currency and are a tool to take money out of an economy that is getting overheated, says MMT. This goes against the conventional idea that taxes are primarily meant to provide the government with money to spend to build infrastructure, fund social welfare programs, etc.

The MMT came into everyone’s focus once again in 2020, post the pandemic. The proponents of the theory lauded the government when primarily the US and other developed economies around the globe took extreme fiscal measures to support their battered economies.

Post the GFC in 2008, only the Central Banks took the lead and printed money, whereas the governments followed fiscal prudence and tried to limit spending and keep the fiscal deficits in check.

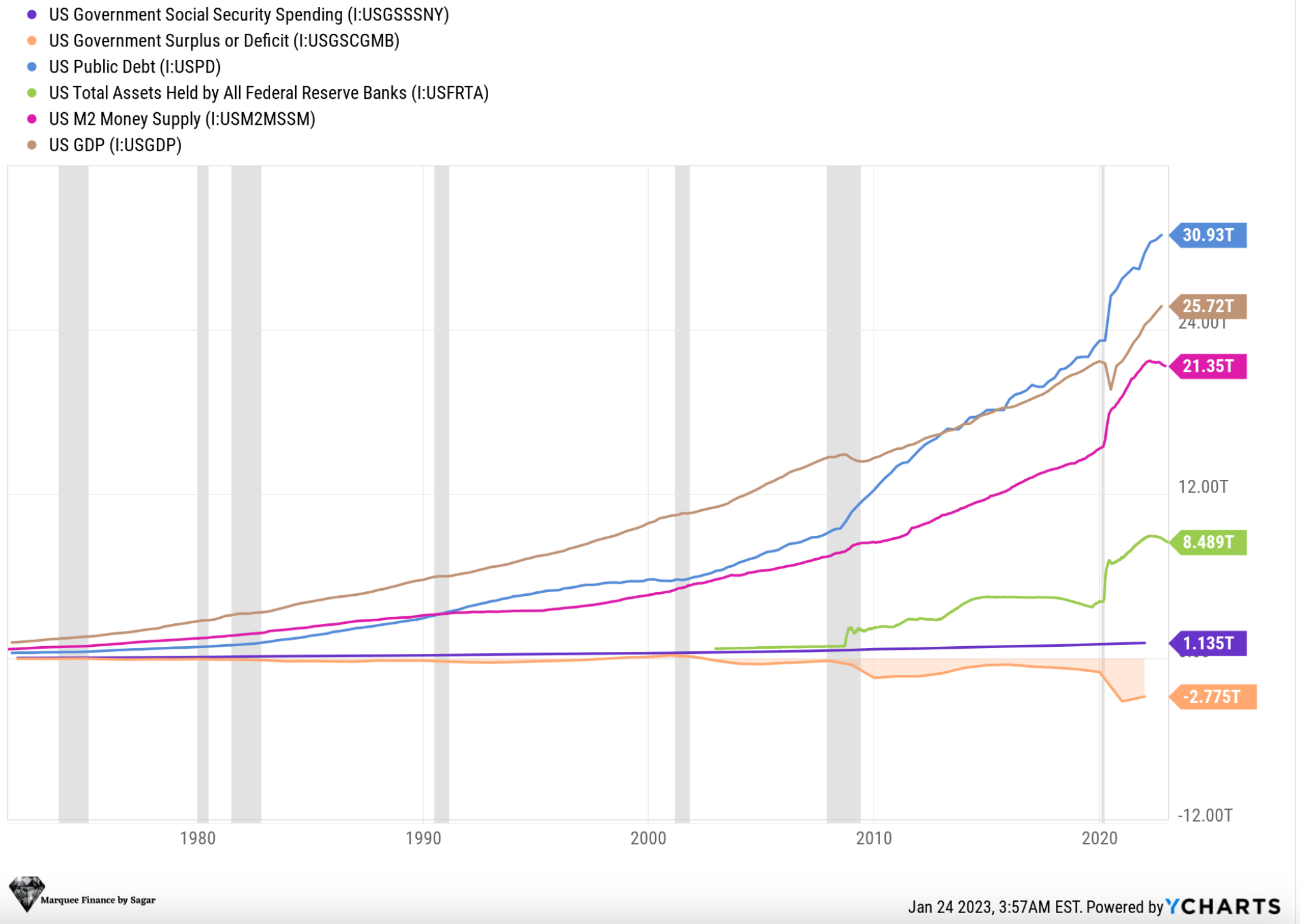

However, 2020 was the defining moment, and the MMT theorists rejoiced as the government loosened its fiscal purses. The result was the ballooning of the Federal Debt in the US and other developed economies:

Federal Debt, which was at $23.2 trillion at the end of 2019, swelled to $31 trillion by the end of 2022.

The MMT theorists failed as the worst fears of economists came true. The flood of stimulus money resulted in the “monstrous” sustained inflation.

The MMT guys often cite Japan’s example to validate their theory. According to them, enormous fiscal and monetary stimuli have failed to induce inflation in the Japanese economy. However, they fail to recognise that Japan has witnessed stagnation of unprecedented levels since the 1980s bubble burst (I covered the Japanese bubble in one of my newsletters: Anatomy of a Bubble 1)

So, why is the failure of MMT inevitable?

The accumulation of debt for unproductive purposes such as social welfare, healthcare and free education doesn’t produce the desired economic benefits. A the end of the day, as Thatcher said, it is the taxpayer’s money, and the high debt burden will be borne by the taxpayers in the form of higher taxes in the long run.

Debt Steroid And Implications!

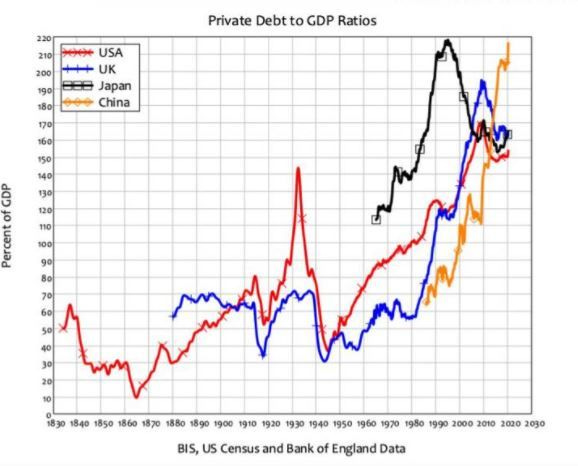

In a global context, IIF estimates that global debt now exceeds $300 trillion or 3.5x GDP, whereas in the 1980s, it was closer to 1.5x, and most economies now require at least 3x more debt to generate one unit of GDP.

The immediate concern is not the high debt burden but the pace of growth in debt due to the gargantuan and unsustainable fiscal deficits needed to support the ageing society. Nevertheless, the sky-high inflation post-pandemic has led to the debt being inflated, which has led to a minor fall in the Debt/GDP ratios of the most indebted countries.

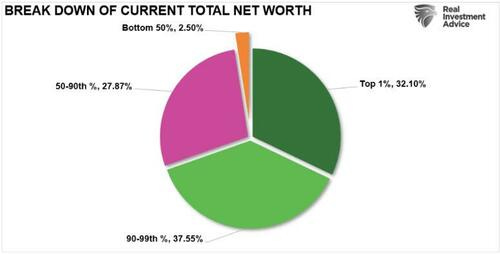

The implication of the “financialization” of the economy in the past four decades has been the malaise of income inequality which has led to the top 1% accumulating unprecedented wealth while people at the bottom of the pyramid are left with nothing and are increasingly “made” to depend on their respective governments.

The wealth disparity became more stark post the GFC as corporate executives took advantage of record low-interest rates (remember cheap unproductive debt) to buy back shares and enrich themselves with more ESOPS (Employee Stock Options).

While the pay for executives zoomed, in contrast, the average worker became poorer.

In fact, it’s not only the governments which borrowed heavily, but the private sector also joined the party.

We can clearly witness how it ends; Japan is the prime example of things to come in the developed world and in China. The deleveraging is extremely painful and takes decades to transpire.

We can only delay the inevitable but can’t halt it!

The Japanese Hurdle and Endgame!

“Overall JGB issuance, including rolling over bonds, remains at an extremely high level worth about 206 trillion yen. We will step up efforts to keep JGB issuance stable”-Shunichi Suzuki.

Every 1% rise in interest rates in Japan would boost debt service by 3.7 trillion yen to 32.5 trillion yen for the 2025/2026 fiscal year. This becomes a severe impediment to financial stability in Japan, as the higher interest costs will entail higher borrowings, thus creating a debt spiral.

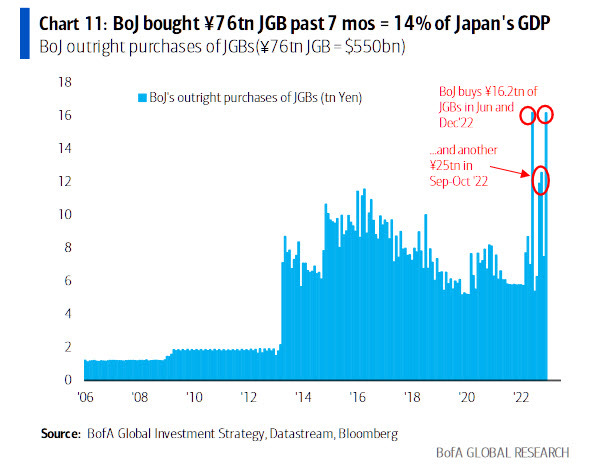

We have already witnessed that the Bank Of Japan (BoJ) is under severe pressure after it raised the YCC ceiling to 0.5%. In a shocking development, the BoJ, since raising the limit, has been buying bonds in regular “unscheduled” bond buying operations to keep a lid on the benchmark yields at 0.5%.

The JGB buying has resulted in tremendous stimulus and money printing; in mind-boggling figures, in the last 7 months alone, the BoJ has bought more than $550 billion of bonds or roughly equivalent to 14% of the Japanese GDP.

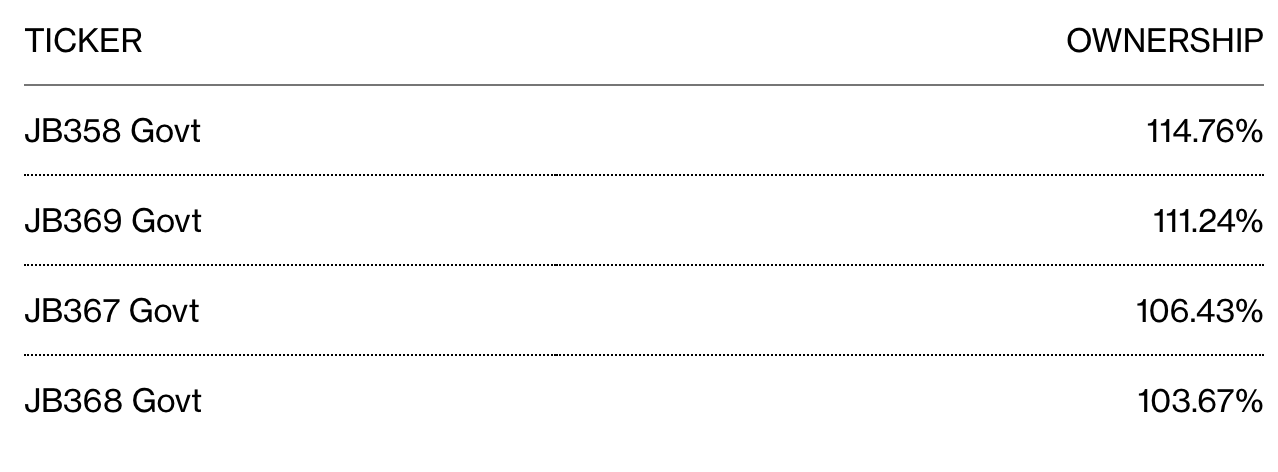

The bewildering fact is that the BoJ owns more than 100% of some of the outstanding bonds. As per Bloomberg: “Among over 300 securities owned by the BoJ, the BoJ owns four such issues where the ownership is more than 100% ”.

The likely reason for owning 100% of a particular security can be attributed to double counting as the BoJ lends out securities to alleviate a liquidity crunch in the market, but some of them get sold back to the CB.

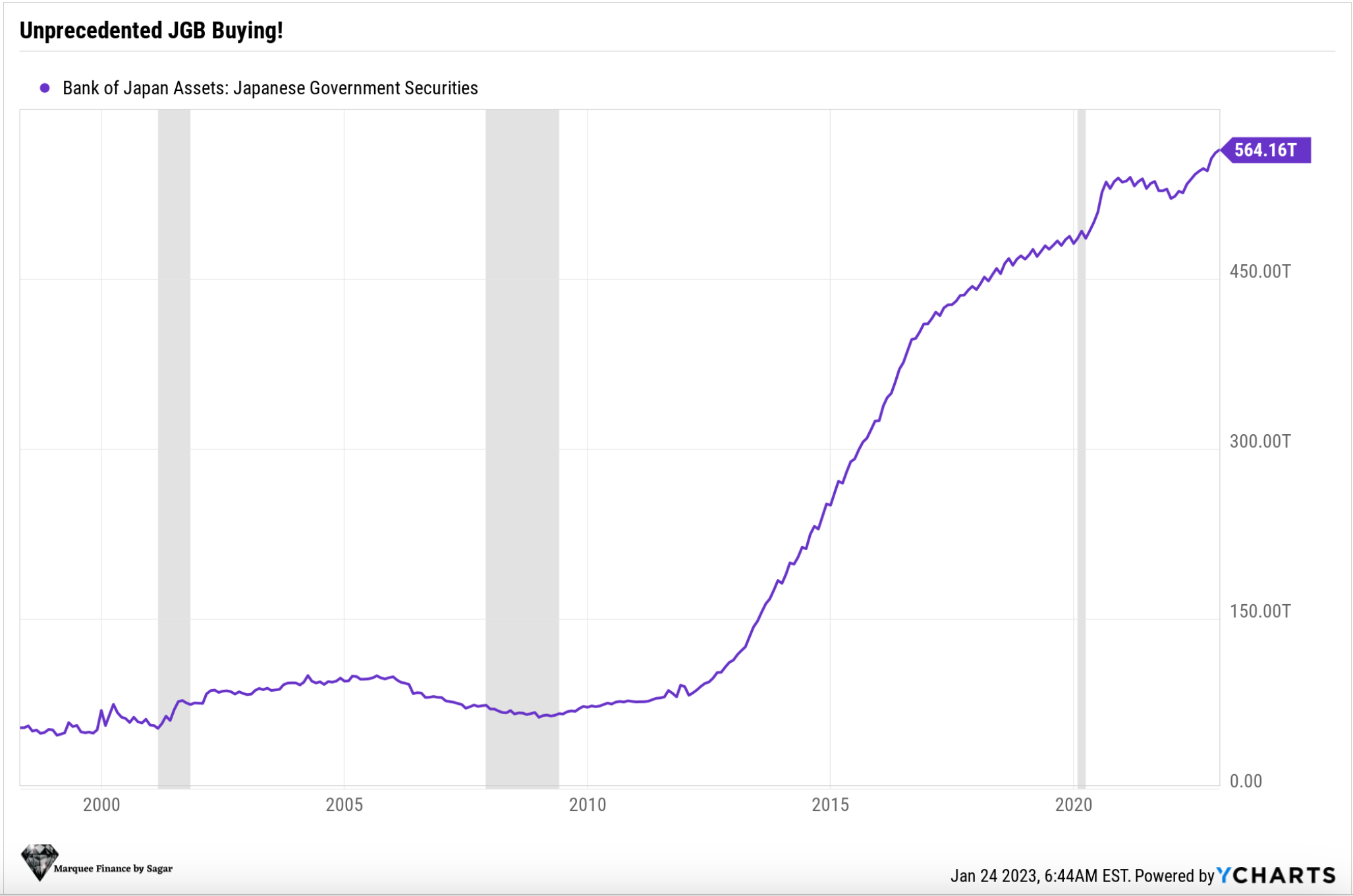

You will be astounded to know that the Japanese bond market is worth $7.9 trillion and thus is the largest in the world. Unfortunately, years of bond buying by the BoJ have resulted in dysfunctional markets, with no trades happening for days.

In a startling fact, all the JGB purchases have now resulted in the BoJ owning roughly 55% of the whole bond market (around 1000 trillion Yen), making the markets illiquid and driving the private players out.

Additionally, the BoJ focusing on the benchmark 10-year bond for its purchases has unintended consequences. The yield curve has a kink that can cause distortions in the corporate bond market. (More here)

The frantic buying in recent days has led to speculation that the BoJ is less than a year away from running out to buy bonds!

So What Is the Endgame?

What happens when the BoJ holds 100% of the Japanese bond markets, probably by the end of this year?

Here are two plausible scenarios that I can envision:

YCC is Abolished: Many market participants speculate that YCC will be abolished entirely after the new Governor assumes office. In this scenario, the purchases of JGBs might slow down as the elevated purchases in recent months were made to defend the YCC cap.

YCC Limit is Increased to 1%, and Inflation Accelerates: In this scenario, the purchases might remain elevated as the markets push the BoJ to further increase the limit due to heightened inflation. As a result, we will reach 100% way before than anticipated in this scenario.

Nonetheless, the BoJ will own the whole JGB market sooner or later. The repercussions of a completely illiquid and broken bond market will be massive.

As the non-financial private sector will have no incentive to buy government bonds, the money will flow into risk assets in the domestic market, fueling a speculative bubble, or money will move out of Japan, leading to enormous depreciation of the currency. Furthermore, corporate bond markets will feel the maximum pain of the BoJ’s madness.

Another doomsday scenario involves hyperinflation akin to Germany in the 1920s.

All in all, an illiquid government bond market is not healthy for the financial system and with Japan one of the biggest liquidity suppliers to the world and the largest holder of the USTs, the Japanese blowup can set off a chain of events which can be catastrophic for the global financial system. (Read Here How)

Conclusion!

The excessive unproductive debt related to the reckless profligacy of central banks worldwide has scary consequences.

The doomsday scenario is a nightmare of the CBs and governments’ own making.

As the world swims in the ocean of unsustainable debt, the demographics are declining rapidly, compounding problems for everyone. Until now, productivity growth has helped to overcome the demographic challenge, but maybe it’s not enough for the future.

This amazing video by Eric Basmaijan of EPB Macro beautifully explains the demographic challenge with some insightful data.

If you are an investor, trader, economist, or macroeconomic enthusiast, you cannot miss what’s happening in Japan.

Folks, our global financial system hangs by a balance. Thus, everyone should own a good chunk of hard/tangible assets (gold, RE) in their portfolios to hedge against an accident that can distort the global markets.

I may have a surprise for you guys next week!

So stay tuned! :)

Disclaimer

This publication and its author is not licensed investment professional. Nothing produced under Marquee Finance by Sagar should be construed as investment advice. Do your own research and contact your financial advisor before making investment decisions.