Explosive Setup Part 2.0?

In late January, when everybody was extremely bullish on risk assets (especially the US), we wrote “Explosive Setup,” in which we explained how the US and Japanese equity markets were poised for a significant decline, while the European and Chinese markets were ready for a substantial move higher.

In fact, just after we wrote the piece, the Deepseek model was released, which led to a significant drawdown in the US tech names (especially semis), and the outperformance of the Chinese and European markets began.

Though we got the Gold move wrong, we correctly predicted the moves in the rest of the asset classes.

We are now at the cusp of a similar move across assets, and we are already positioned for it.

We will discuss the direction of the move later and examine the technical indicators and macro setup, which we believe will be responsible for the move.

Regarding our performance, our timely bets on Silver and Oil have led to new all-time highs for the PF, and significant outperformance continues, with a return over 250 bps higher than our benchmark.

P.S.: The benchmark changed on May 1st (60% MSCI ACWI and 40% BBG Global Aggregate), as US equities form a significant portion of the equity portfolio.

A gentle reminder for new subscribers: please download the Substack app, as the notifications are beneficial for those who actively trade (in the chat section).

Let us now begin today’s newsletter and comprehend the data releases in the macro universe!

US/Bonds/Gold/Silver/Oil/Dollar!

Our preferred measure for tracking the cyclical sector of the economy is the ISM Manufacturing Index.

Over the past 2-3 months, the ISM Manufacturing Index, like other soft and hard data, has been noisy due to the front-loading of tariffs. We expect normalisation to transpire in the next month or so.

This month, we saw a significant contraction in inventories (as the tariff front-loading ended, inventories will contract, and new orders will plunge).

We also saw an enormous decline in imports, as expected (a reading below 40 is rare and typically occurs in extreme events).

Nevertheless, new export orders are the ones that we will closely examine, as they would indicate a weak global economy.

The headline index and our favourite indicator, New Orders Less Inventories, won’t represent the true picture due to tariff front-loading, as we discussed.

Nevertheless, if the trend of higher New Orders Less Inventories persists in June and July, we can expect higher ISM readings.

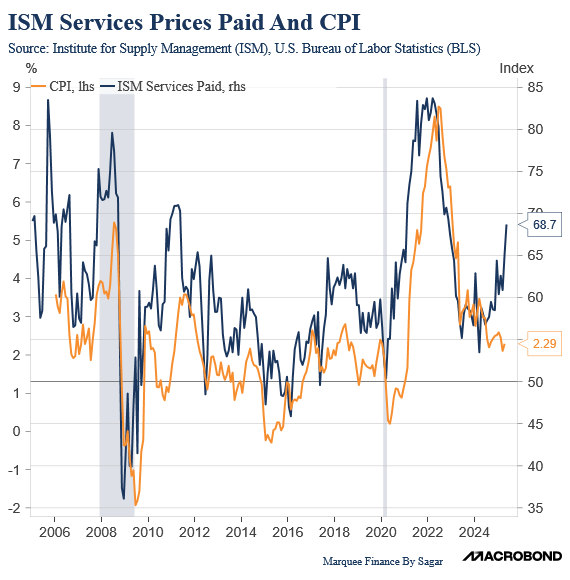

One component of both ISM Manufacturing and ISM Services, which has been sticky (and in fact rising), is the ISM Prices Paid.

Though some of it could be attributed to the tariffs’ impact, if the trend prevails for a quarter or so, it would be alarming for the Fed.

If the ISM Prices Paid is to be believed, the CPI is ready to move “significantly” higher in the coming months, and the next week’s reading will be the lowest we will witness for months to come.

Before we delve into the labour market, we finally have the data on the issue that we have focused on over the last few weeks to determine the trajectory of inflation. As per the…

Keep reading with a 7-day free trial

Subscribe to Marquee Finance by Sagar to keep reading this post and get 7 days of free access to the full post archives.