It's Showtime!

“We think Financial Conditions are weighing on the economy.”- Jerome Powell, 20th March 2024.

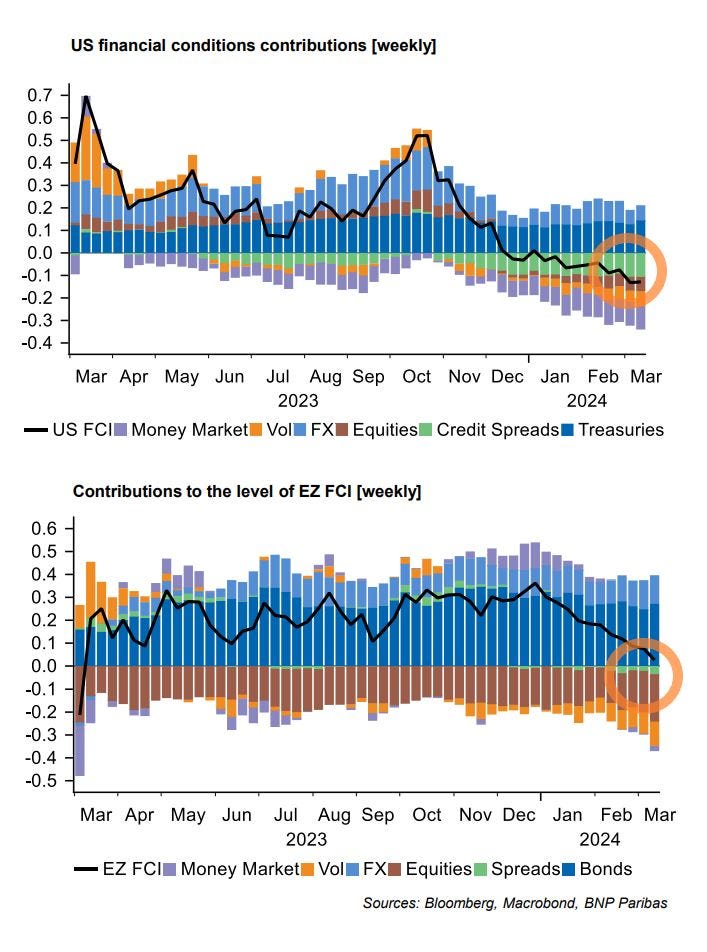

Despite record easing of financial conditions, equivalent to the period seen post enormous GFC and COVID stimulus, the world’s most powerful Central Banker refuses to acknowledge the same, thus propelling risk assets to the moon.

In fact, the Financial Conditions Index (FCI) is now as loose as it was when the Fed began raising rates or when rates were nearly zero.

As a result, the speculative mania in assets like crypto is on the verge of topping the 2021 bubble as markets consider CBs policy supportive of liquidity and easy financial conditions.

Last week, we wrote about how “Historic unwinding” has the potential to snowball into an outcome that could lead to wild cross-asset moves.

Undoubtedly, the FOMC outcome and the SNB surprise cut have set the stage for the synchronised unwinding of the monetary policy by the developed CBs globally.

PS: We may be near/got the macro trigger to partially end the speculative mania (paid subscribers can directly jump to the conclusion).

Let’s analyse the nuances of the monetary policies and make sense of some macro data released this week.

US!

“Doesn’t see rates going back to ultra-low levels.”- JayPo.

Yes, folks, we may no longer see negative interest rates again in our lifetimes.

There has been a paradigm shift in inflation post-COVID.

Twelve years of super-loose monetary policy could not accomplish what a multipolar world, helicopter money (fiscal stimulus), deglobalisation, and supply chain disruption have achieved.

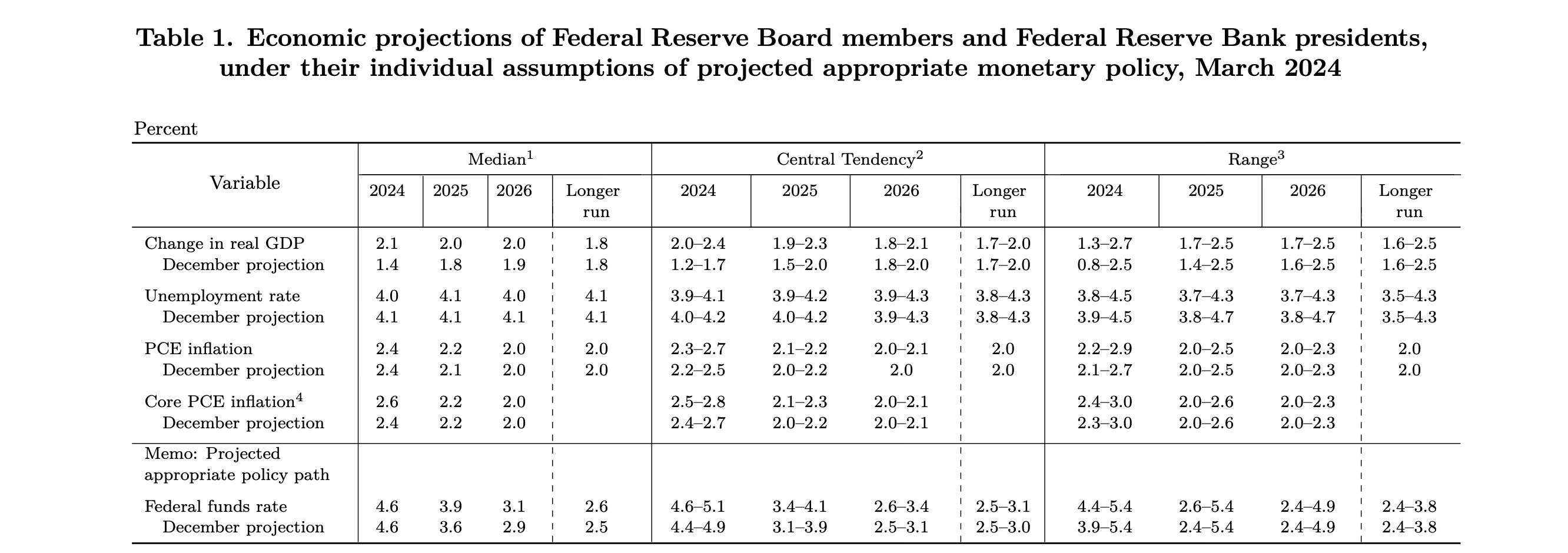

The SEP projections laid an intriguing path for inflation, growth and UR.

While growth and inflation figures were revised upwards, the unemployment rate (UR) was slightly revised downwards.

There is a growing consensus that the Fed will comfortably tolerate slightly higher inflation (around 2.5%) for a longer time and won’t wait for the exact 2% to lower rates. This was visible:

As the longer run FFR was raised higher, albeit by only 10 bps to 2.6% from 2.5%.

More FOMC members are comfortable tolerating higher inflation and simultaneously cutting rates, as they likely believe that rates are restrictive enough.

Furthermore, JayPo literally spelt out what we had been advocating for weeks now. In fact, we even began to position our portfolio for the likely outcome.

JayPo ruthlessly mentioned:

Keep reading with a 7-day free trial

Subscribe to Marquee Finance by Sagar to keep reading this post and get 7 days of free access to the full post archives.