Month In Charts: February 2024!

Month In Charts: February 2024!

February was marked by a scorching rally in risk assets led by Bitcoin and fuelled by AI Names, primarily NVDA.

With the help of intriguing charts, today we will look at what’s driving this historic run in equities. On the contrary, the bond markets remain calm and continue to disappoint investors.

Let us begin with the February Month In Charts edition!

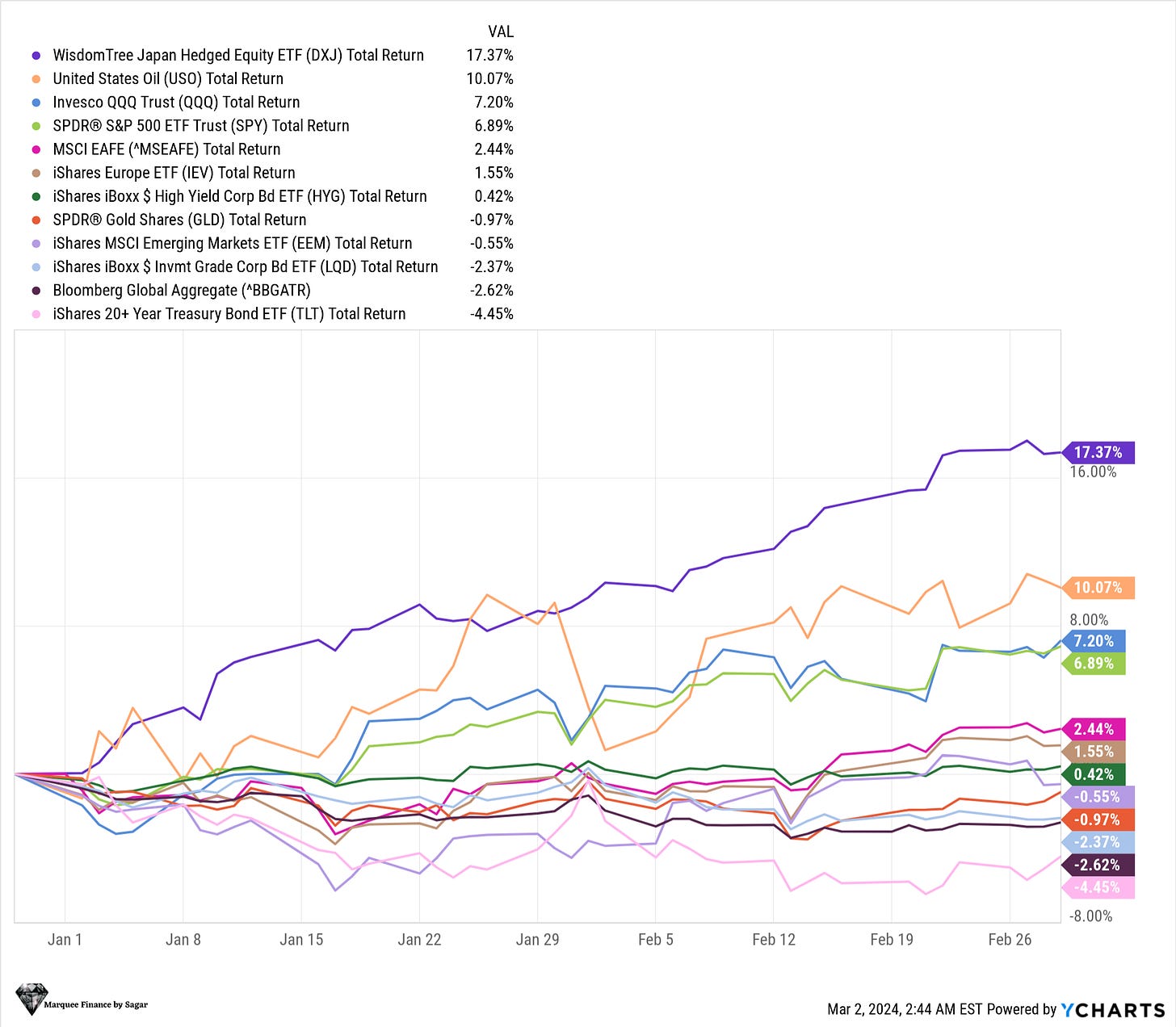

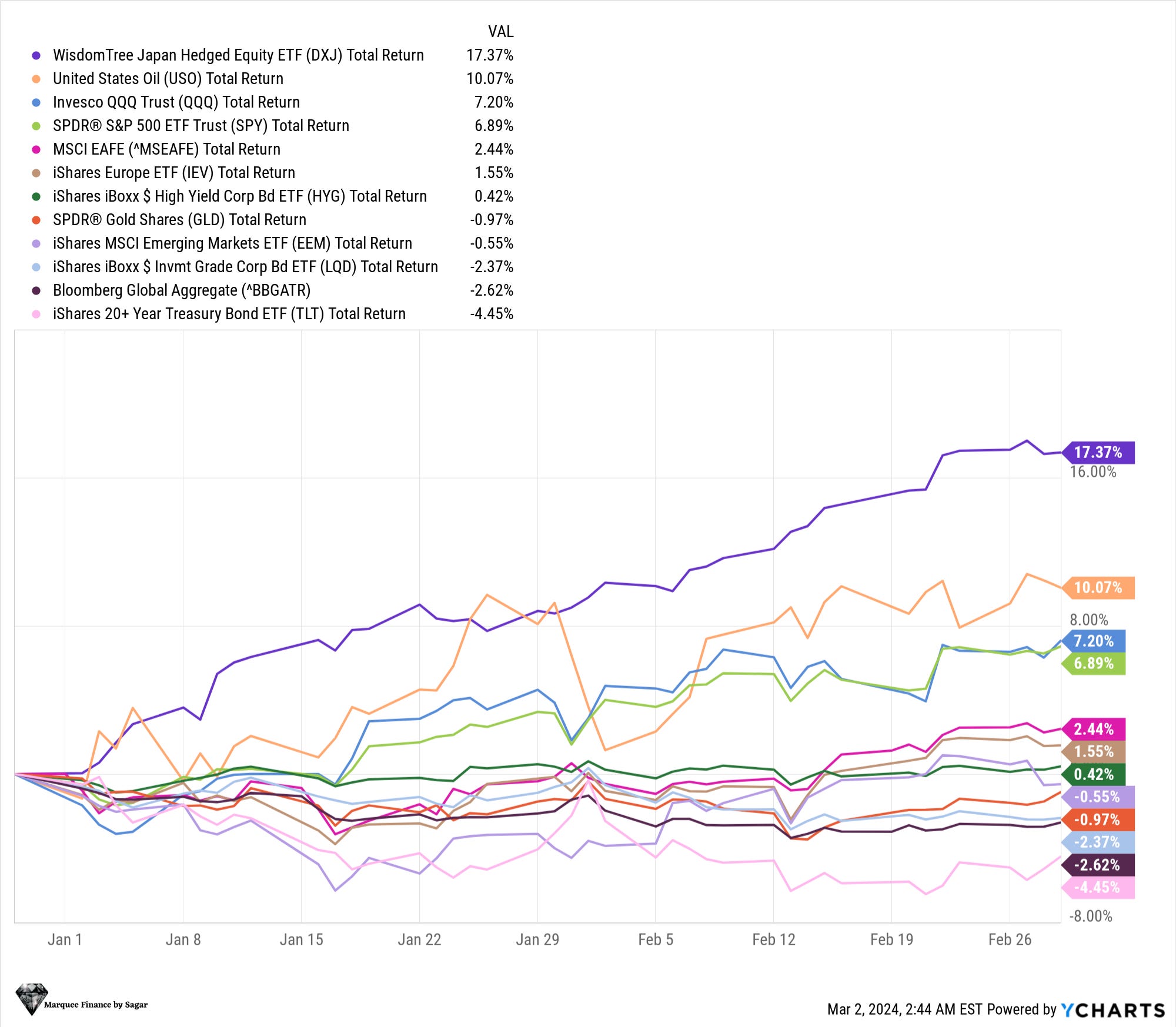

The risk on rally that has been in motion since October last year gained further momentum post the poster boy NVDA’s earnings. Japanese equities have been on a tear, with Nikkei up 20% in just two months (local currency).

Even crypto joined the party, with BTC up 47% YTD. Notably, the total crypto market cap has surpassed $2.2 trillion.

Nonetheless, long-term bonds have been a dampener and are still in negative territory.

The relentless equity rally has broken multiple records.

Notably, the S&P 500 has now advanced for 16 of the last 18 weeks. The last time that happened was in 1971, shortly before the end of the Bretton Woods system. The S&P 500 has now rallied 24% from its October lows.

Source: BBG

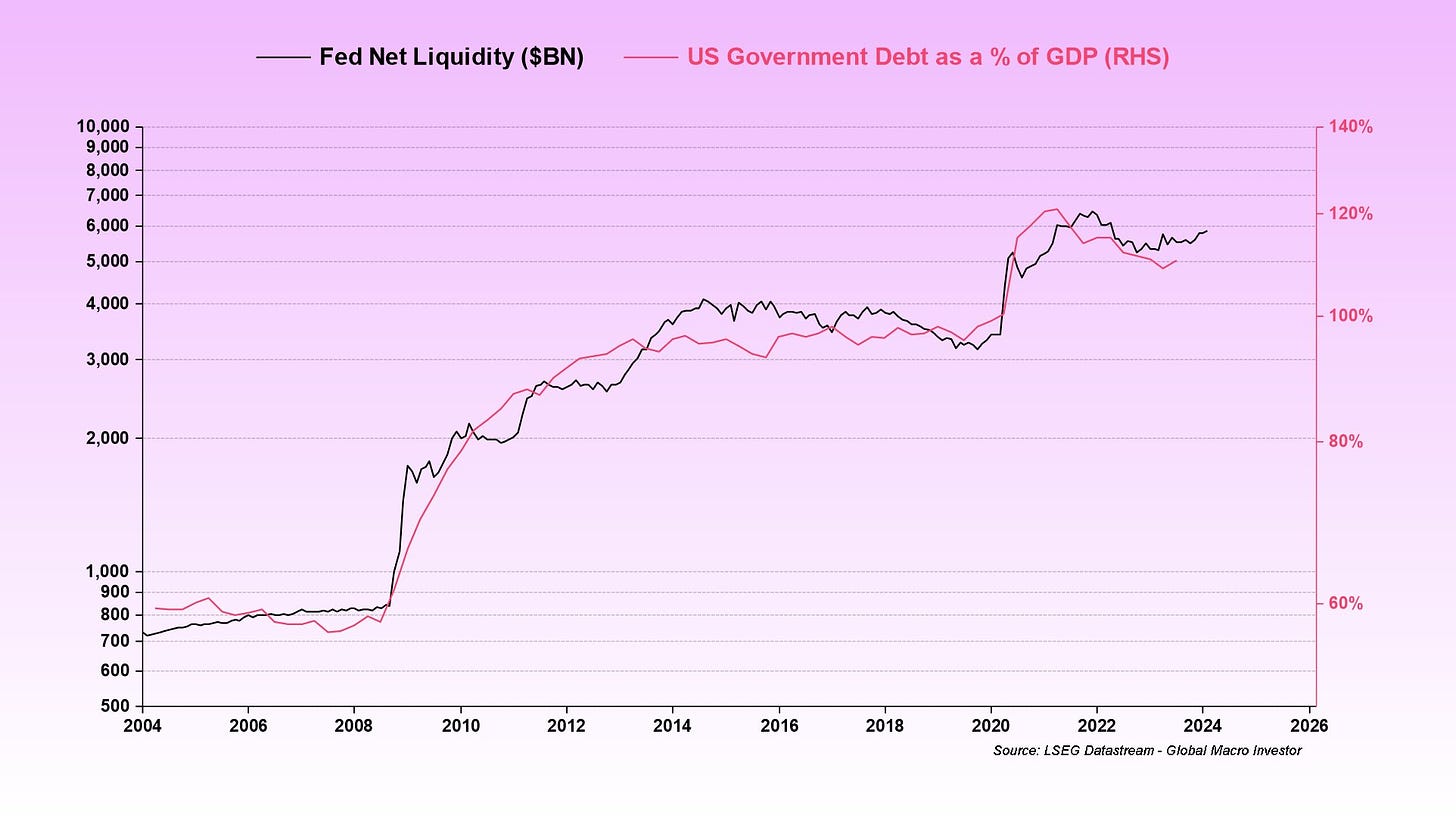

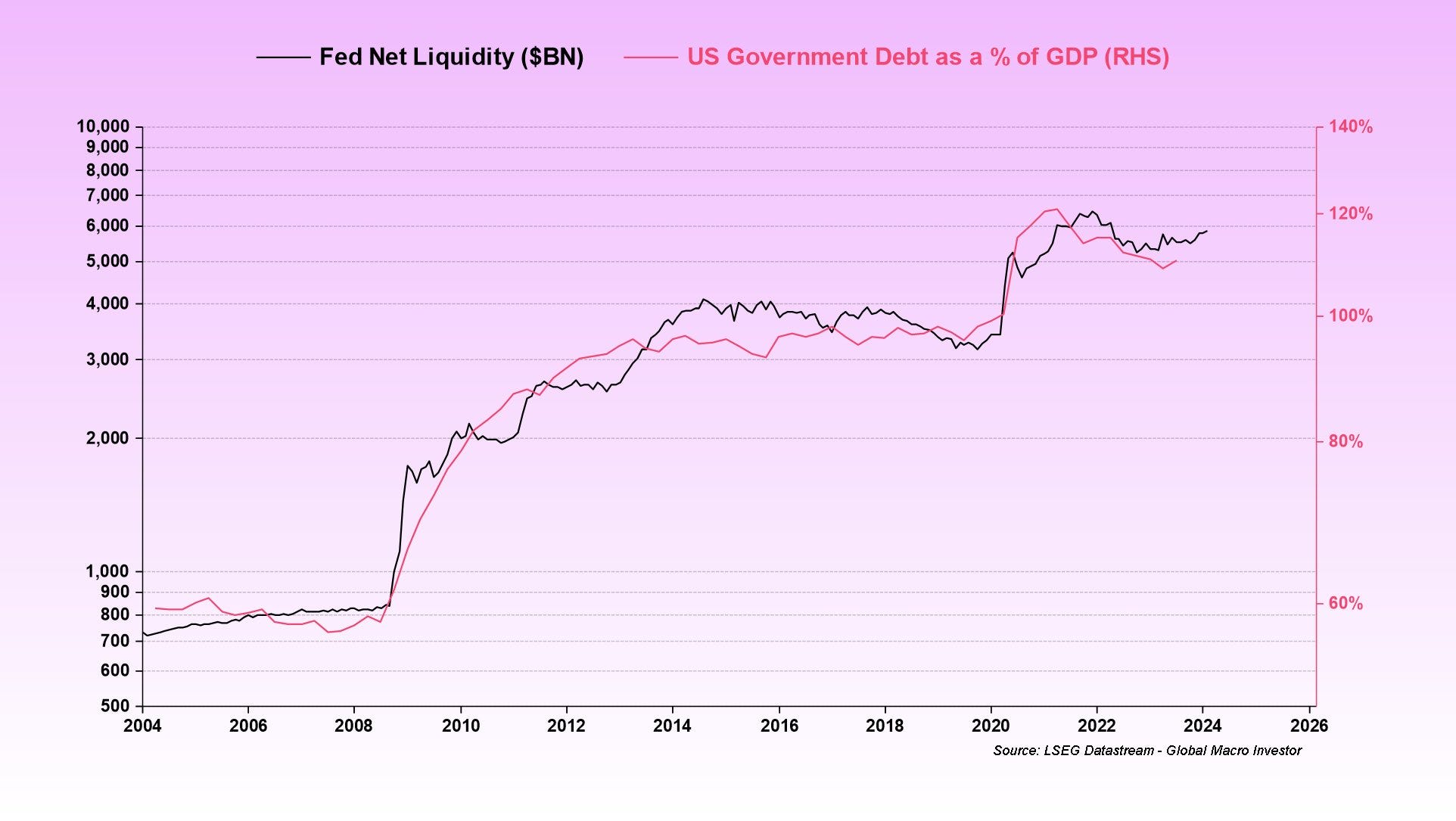

If you are wondering what’s behind this dream run, well there is no money for guessing that liquidity has been the sole driving force behind the unprecedented risk on rally that we have witnessed in the last four months.

Furthermore, the retail flows have been robust with option mania (primarily calls) back to its 2021 highs.

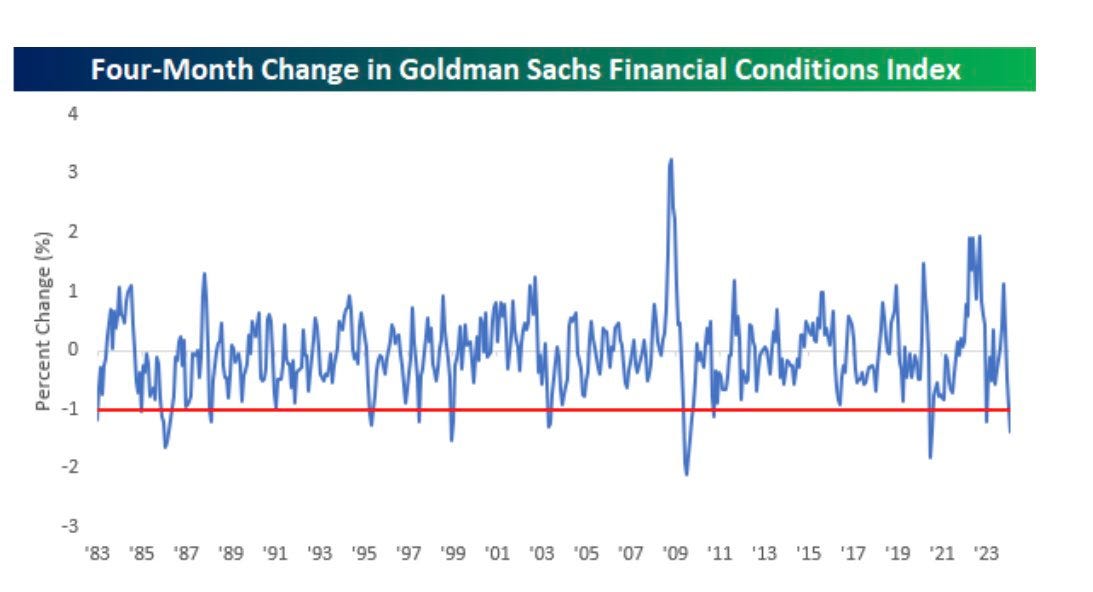

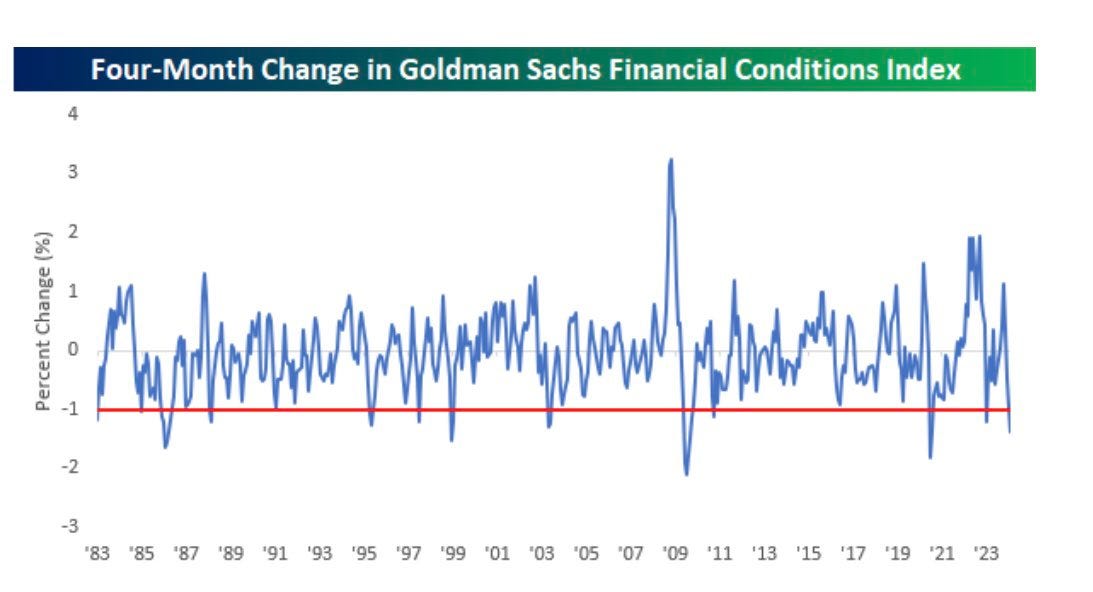

Source: LSEG As a result of the melt-up in equity markets and the rally in junk bonds, the Financial Conditions Index (FCI) has significantly eased. Thus, the FCI easing has done the job for the Fed with more than 100 bps of cuts already priced in by the markets.

In fact, the four-month change in the FCI has now been the largest since 1982.

Well, one more for the record books.

Source: Bespoke

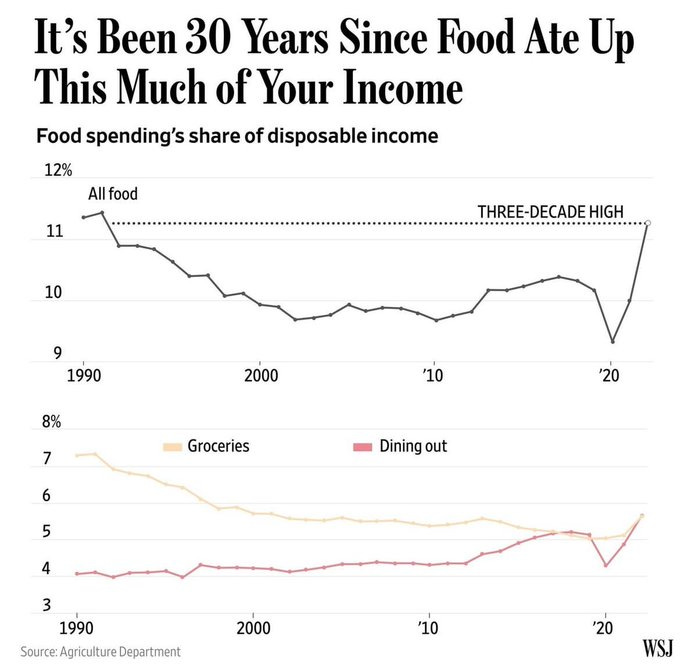

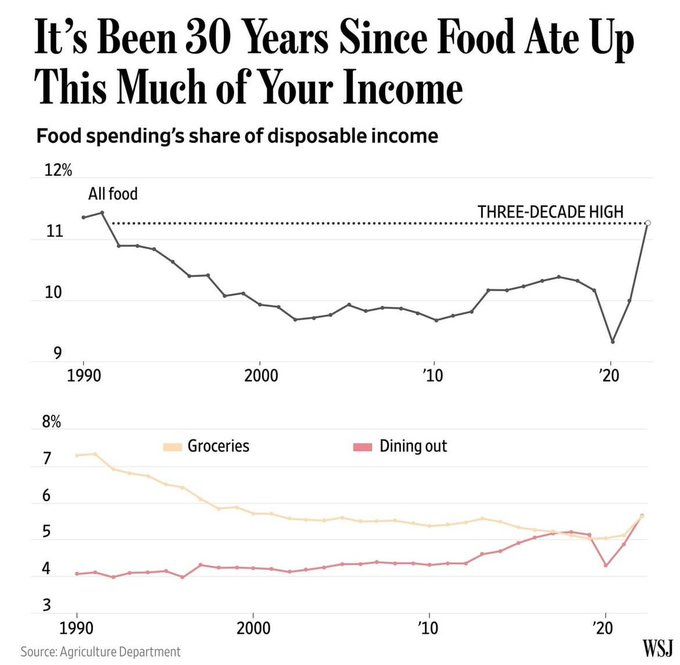

Coming to some macro data, inflation has significantly cooled off from the peak when it almost reached double digits in the US.

Nonetheless, the absolute price increases have been so enormous that food spending as % of disposable income has reached a three-decade high!

One more record! Huh!

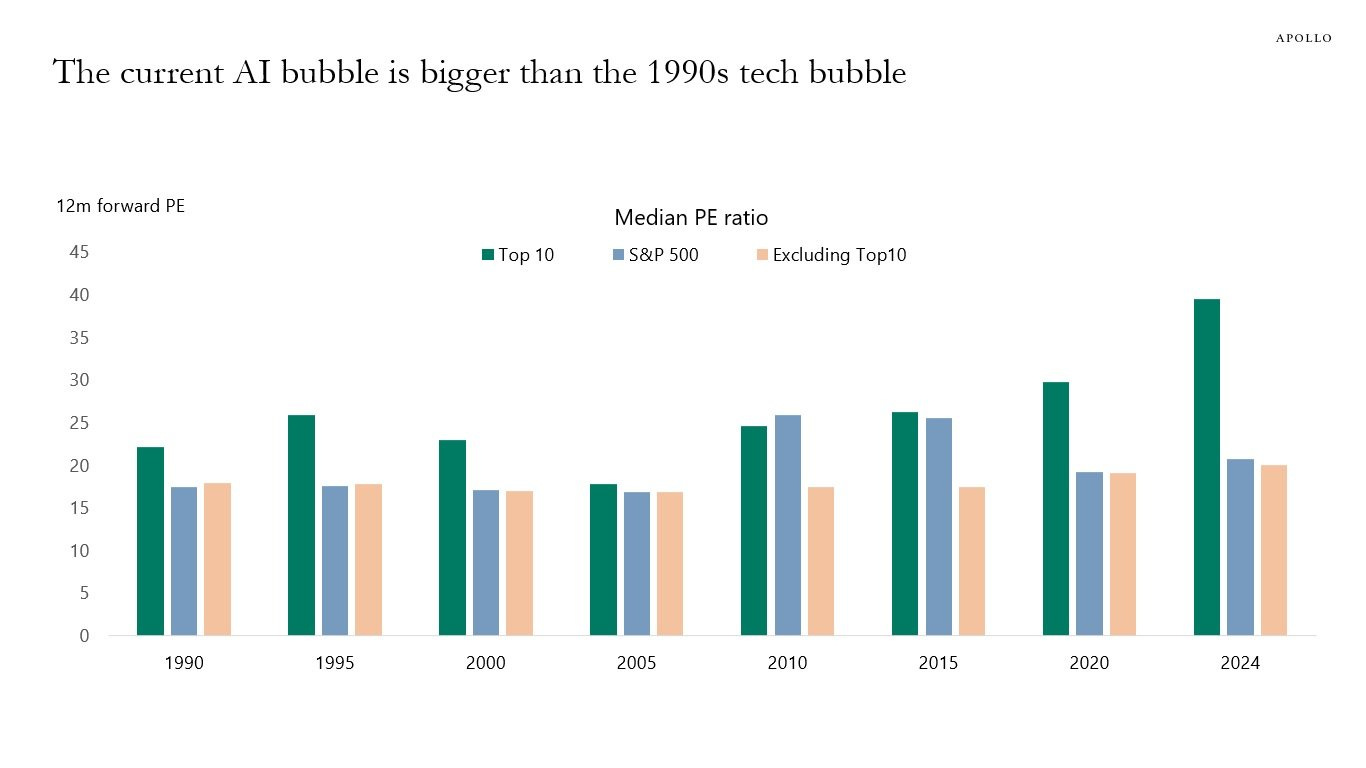

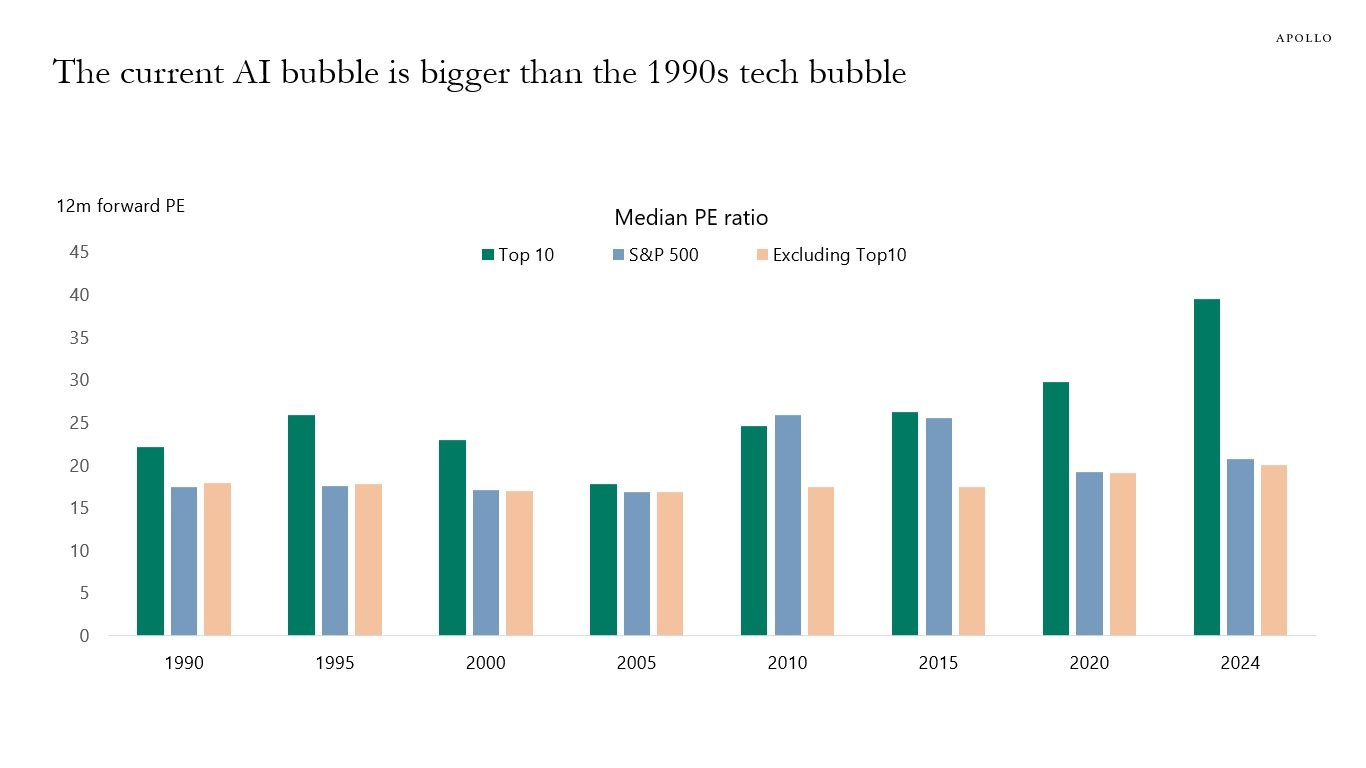

Before we end the US Section, there has been a raging debate about whether we are in a bubble.

Though we believe that the overall market (SPY) is overvalued by 10-15% as per our macro scenario, parts of the markets are indeed frothy and ripe for correction.

Some observations by Apollo:

“Forward P/E ratio for the top 10 tech stocks right now is ~40x. Compared to 2000, at the peak of the Dot-com bubble, the Forward P/E on the top 10 tech stocks was ~26x.”

Source: Apollo While the economic activity has witnessed a rebound in the US thanks to the enormous fiscal deficits that the US Government has been running, Europe has been hard hit by the twin crisis (energy and the tight monetary policy).

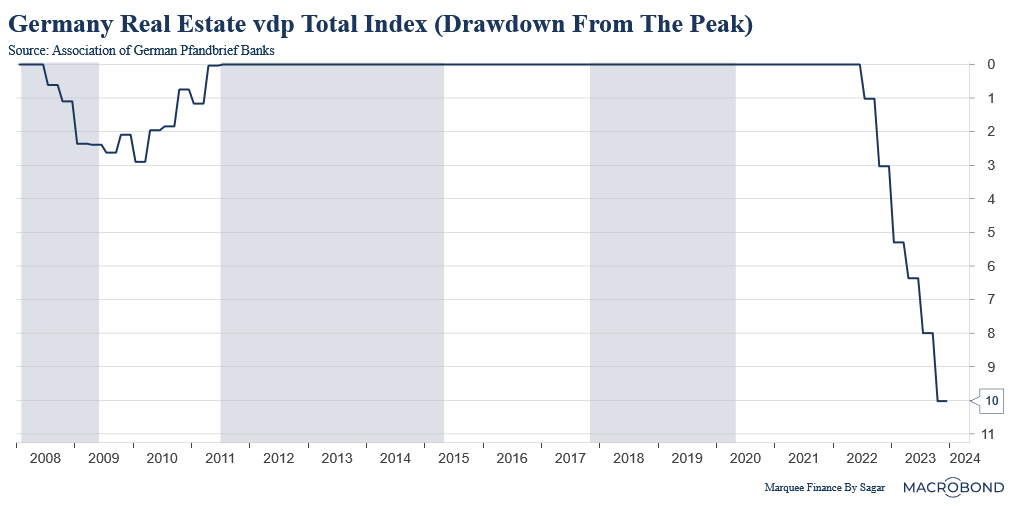

As a result, Germany has been coined the “Sick Man” of Europe. The cyclical activity has come to a grinding halt.

Some more macro data from Germany.

In stark contrast to the US, where housing prices have touched all-time highs despite 30-year high mortgage rates, Germany’s real estate prices are now in the midst of the worst drawdown ever.

Furthermore, there are concerns that the CRE problem will plague the European banks shortly.

On the other hand, the UK is witnessing a swift recovery thanks to higher real wages compared to its counterparts, which has been driving consumer sentiment up and leading to buoyant services activity.

Nonetheless, one needs to keep a close watch on the labour market.

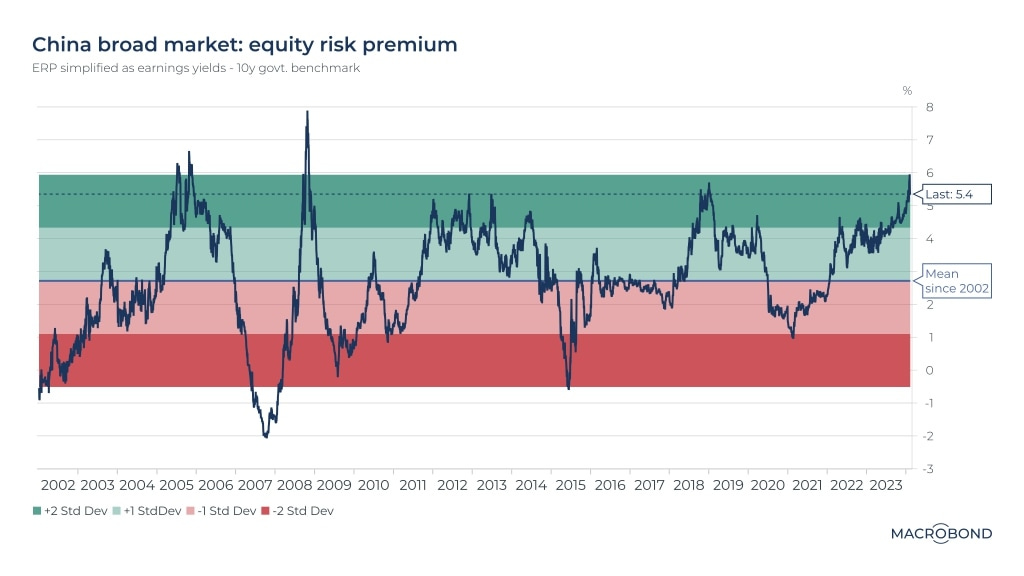

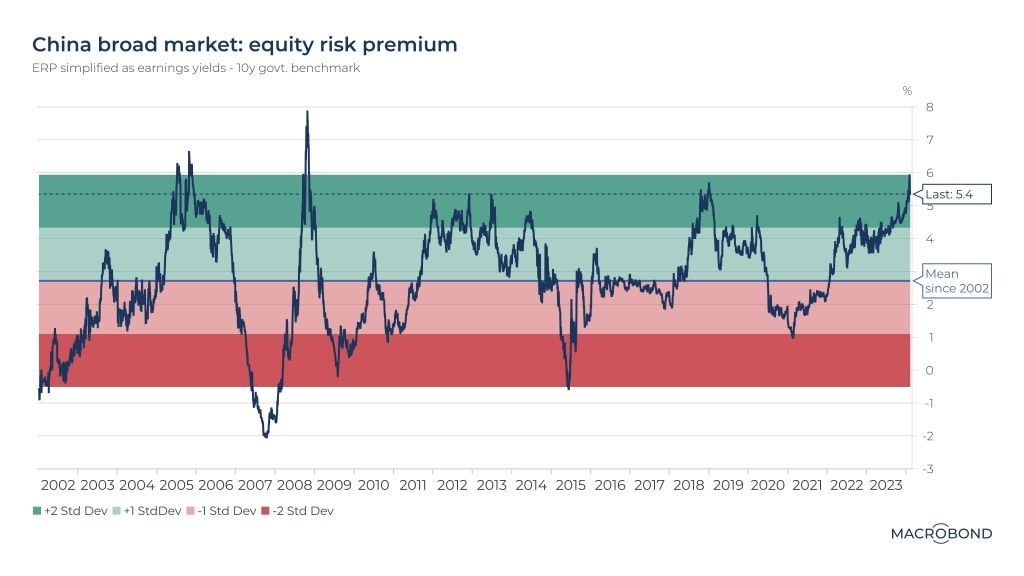

We all know that when a stock or an equity market is cheap, it is for a “REASON”. Ironically, we all know the reasons behind Chinese equity markets' “extreme” cheapness (demographics, property meltdown, weak consumer sentiment and geopolitical concerns).

Nevertheless, if history is a precedent, the Chinese market is ready for a stealth rally as the equity risk premium has “nearly” become the most favourable ever.

One of the intriguing features of the “New” Chinese economy is its determination to shift its entire manufacturing focus to the sunrise sectors.

As a result, we are witnessing a gigantic growth in the Renewables addition, and lately, Chinese EV OEMs have been on a wild ride with exporting EVs worldwide.

Unsurprisingly, China is now one of the largest auto exporters in the world!

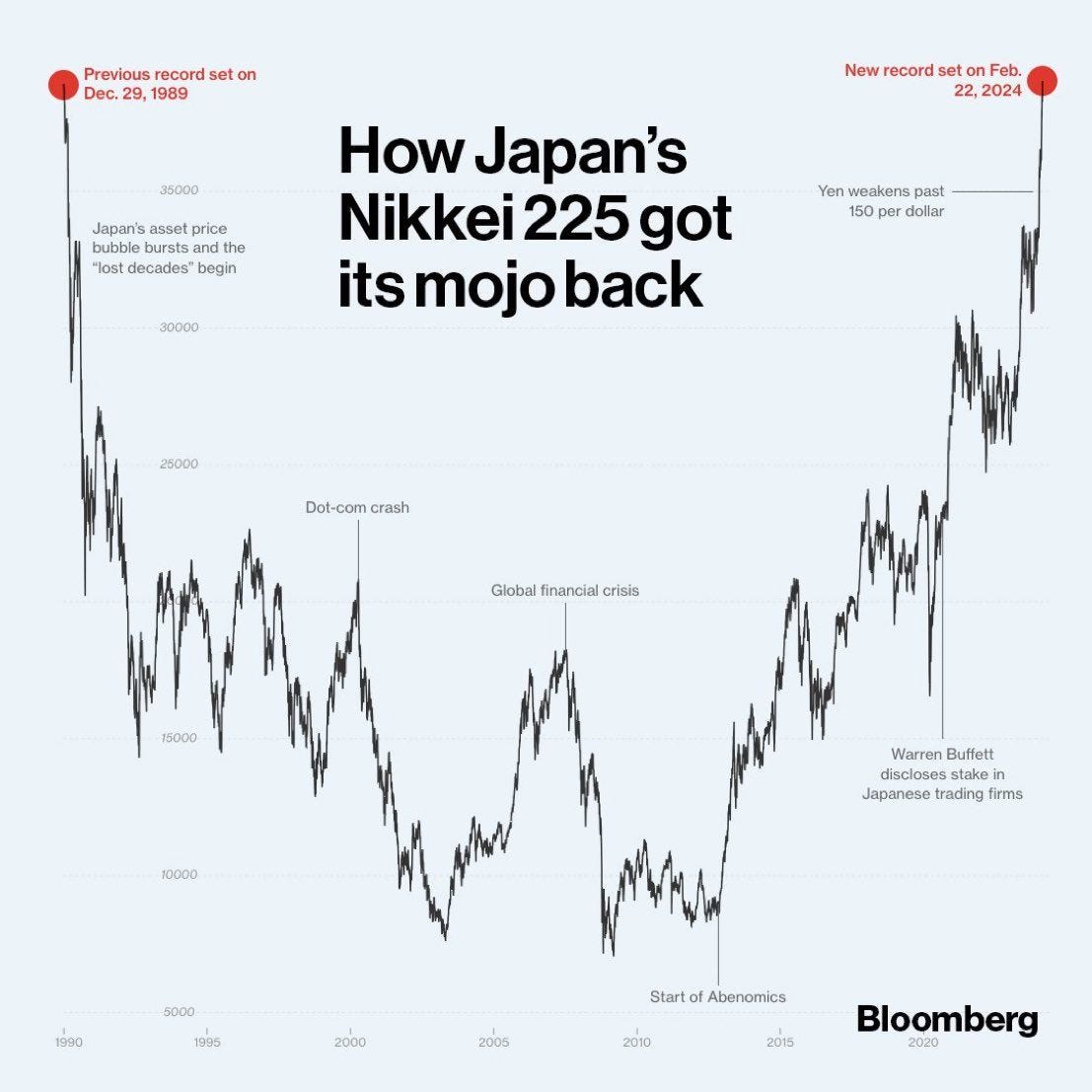

After a long wait of over 34 years, Nikkei225 has finally risen to All Time Highs.

It all began with Abenomics, with the BoJ buying equity ETFs.

The final nail in the coffin was the sharp depreciation of the JPY as the “Contrarian Central Bank” kept the status quo on QQE, YCC and NIRP.

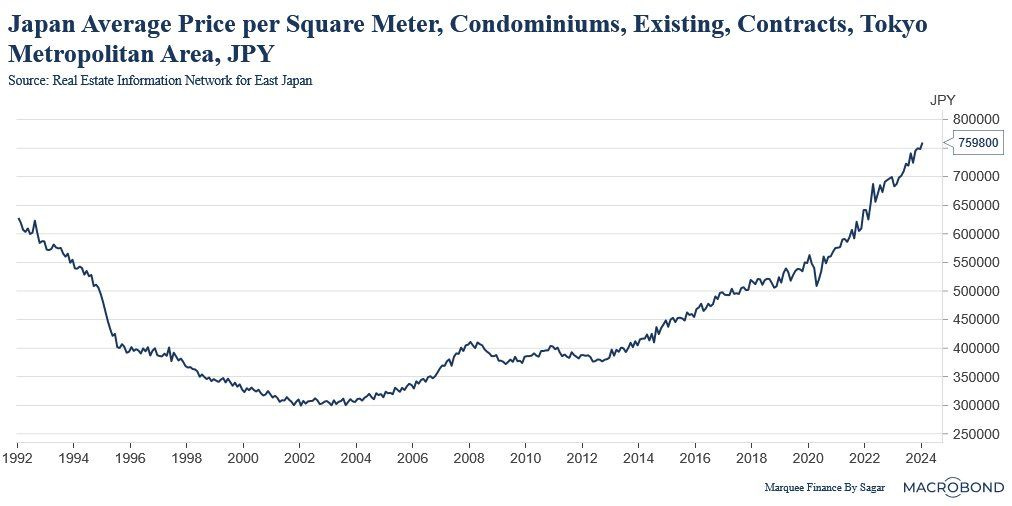

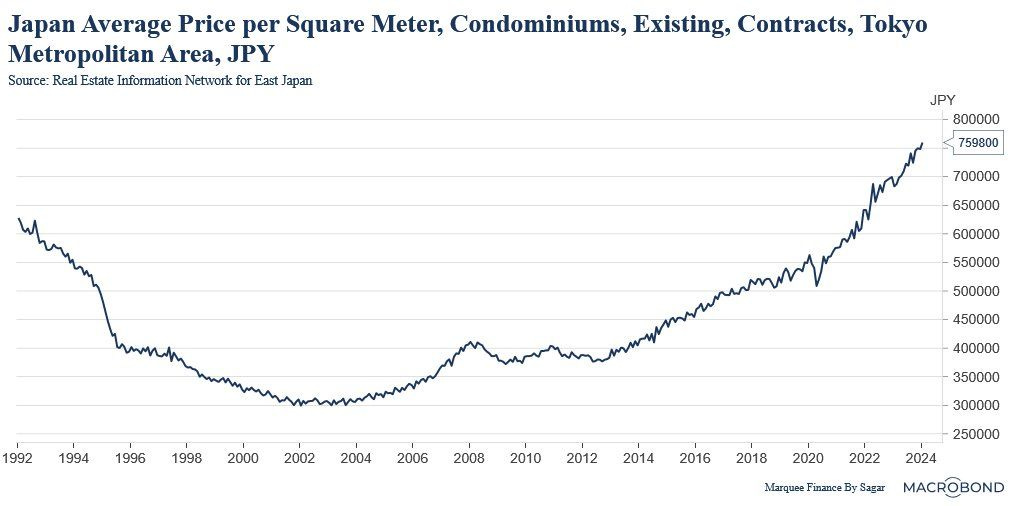

It’s not only equity markets but deeply negative real rates and the imported inflation that have also led to a rise in the Japanese Real Estate market.

Prices in key metropolitan cities such as Tokyo have now surpassed/reached the 1989 bubble levels when the Imperial Palace was valued more than the entire California!

CHOCOLATE LOVERS BEAWARE: Chocolate lovers are in for a rude shock as the Cocoa prices are off the roof.

Prepare to shell out more for your favourite chocolates, as the cocoa supply deficit will not ease in a few days or months.

Chart: BBG BONUS CHART:

One of the biggest bubbles has formed in the East, with millions of Indians driven by FOMO and dreams of being rich overnight, punting on options like never before.

More than 85.3 billion contracts were traded in 2023, almost 8X more than the US!

Well, this, indeed, will not end well!!

Source: BBG

Disclaimer

This publication and its author is not a licensed investment professional. The author & any other individuals associated with this newsletter are NOT registered as Securities broker-dealers or financial investment advisors either with the U.S. Securities and Exchange Commission, Commodity Futures Trading Commission, or any other securities/regulatory authority. Nothing produced under Marquee Finance by Sagar should be construed as investment advice. Do your own research and contact your certified financial planner or other dedicated professional before making investment decisions. Investments carry risk and may lose value; Marquee Finance By Sagar LLC, Marqueefinancebysagar.substack.com or Sagar Singh Setia is not responsible for loss of value; all investment decisions you make are yours alone.