Month In Charts: May 2025!

After a nerve-wrecking April, investors cheered the month of May as risk assets rallied, while concerns persisted about the bond markets, which underwent a rollercoaster ride.

The equity markets rallied by a record 6%, marking the best monthly performance for the S&P 500 in the last 25 years.

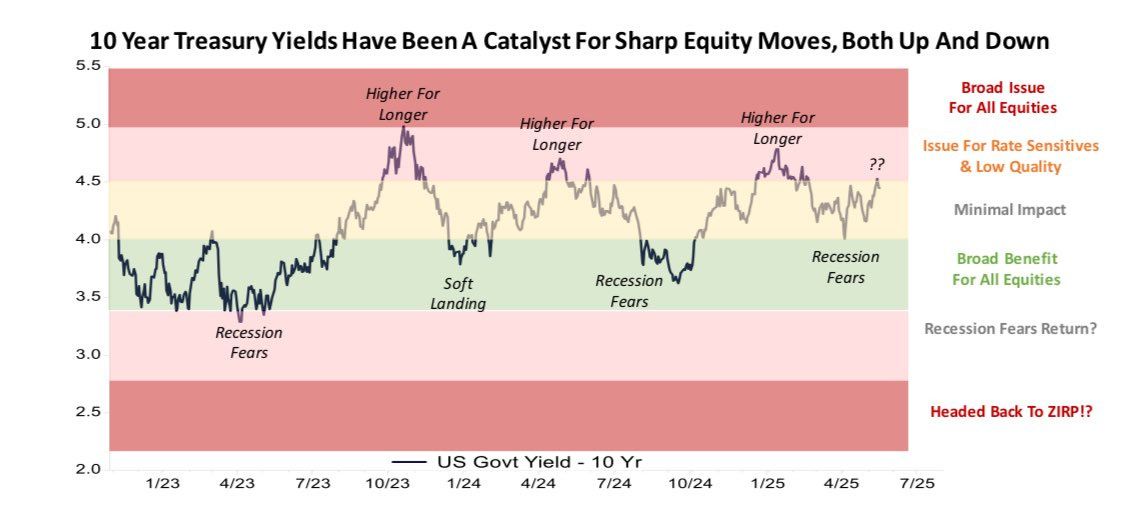

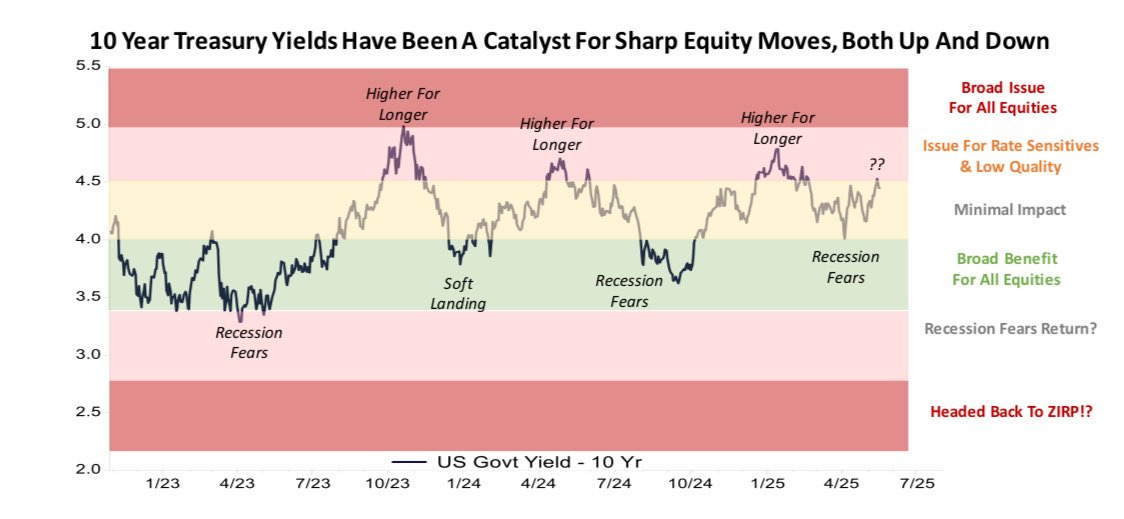

On the contrary, the 30Y bond yield once again approached the 5%, which last triggered the “Bessent Put”.

Let’s comprehend what transpired in global financial markets and the macroeconomic universe in May 2025.

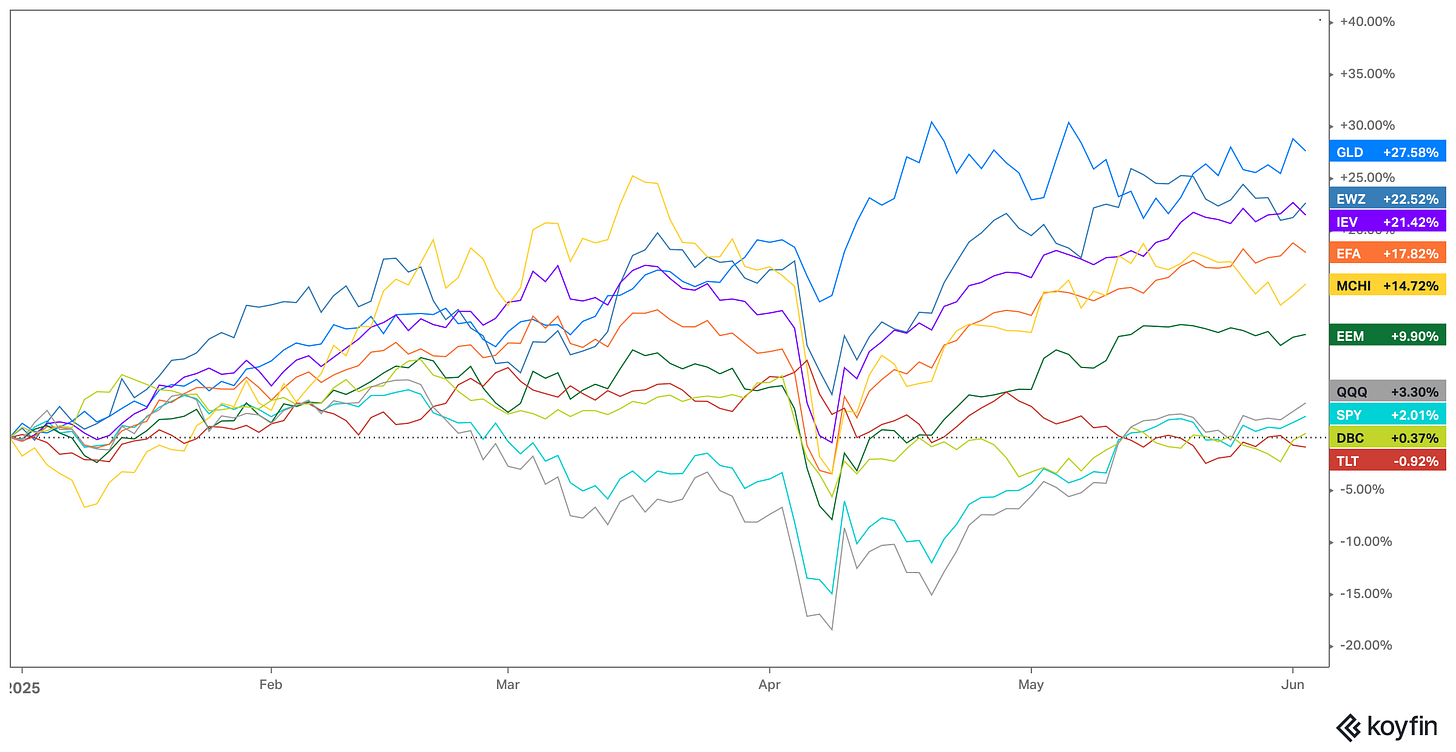

Despite the US equity markets’ outperformance in May, they are still massively underperforming the global markets YTD. While some of the global unhedged ETFs have significantly outperformed due to the enormous currency appreciation (Dollar depreciation), the US assets underperforming the global markets is a trend which has persisted this year.

The shiny yellow metals remain the best-performing global asset with a return of 27.5% YTD. On the contrary, the bear market in the bond market continued, with TLT in negative territory.

Commodities Ex-Gold, Silver and Copper have also been underperformers, with DBC barely positive.

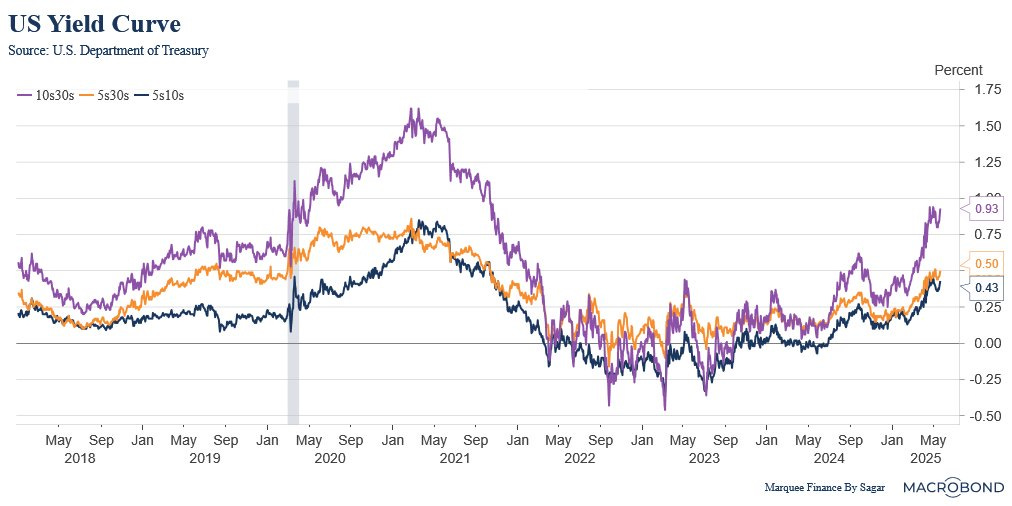

We will discuss the bond markets extensively today. It was no brainer six months ago that the yield curve would steepen.

However, only a few of the market participants got it right as the yield curve underwent a “Bear steepening”, which is when the long-term yields rise more than the short-term yields.

One of the reasons for the bear steepening has been the market discounting higher growth and inflation in the future and pricing out rate cuts far into 2026.

The reason the Fed has been cautious in cutting rates, despite pressure from POTUS, is the uncertainty surrounding the tariffs.

Although the Fed believes that the inflation resulting from the tariffs will be “transitory,” it’s not taking any chances.

Source: BBG

Historically, treasury yields have been one of the most reliable indicators for equity investors, as they help determine the equity risk premium.

Nevertheless, equity markets tend to remain irrational for long periods, driven by the hopes of a new era.

We observed a negative equity risk premium for many months in 2001, and we saw the same trend last year as well.

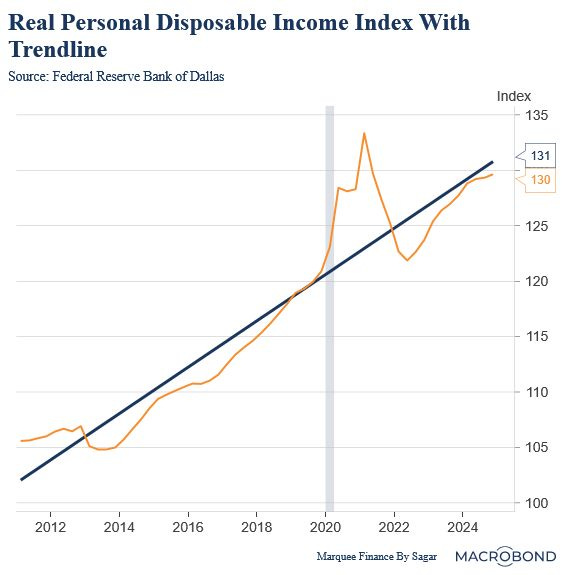

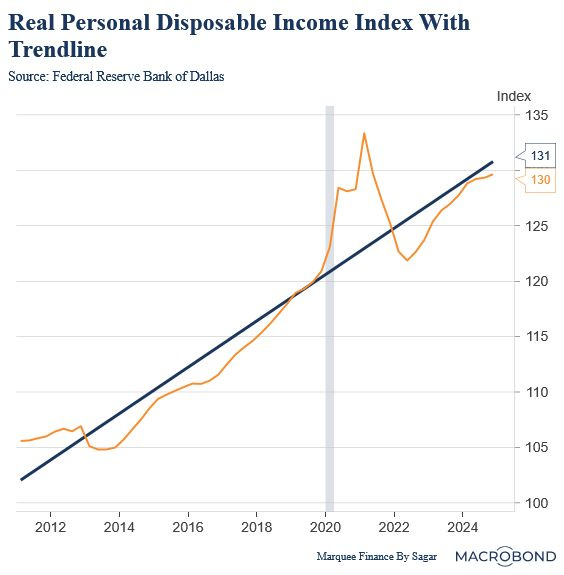

Source: Kantro The soft data has been shaky in the last two months. However, the hard data has been resilient thanks to the buoyant consumers propelled by the positive wealth effect, as all the assets (equities, BTC, housing, and Gold) have been hovering around ATHs.

However, the recovery has been K-shaped, with the bottom end of the consumer reeling under the pressure of high cost of living and higher rates.

The inflation pain is also visible in real disposable incomes (real = adjusted for inflation).

Looking at the long-term trend, we can confirm that despite trillions of dollars of stimulus post-COVID, which led to enormous accumulated savings, the real personal disposable incomes have failed to recover.

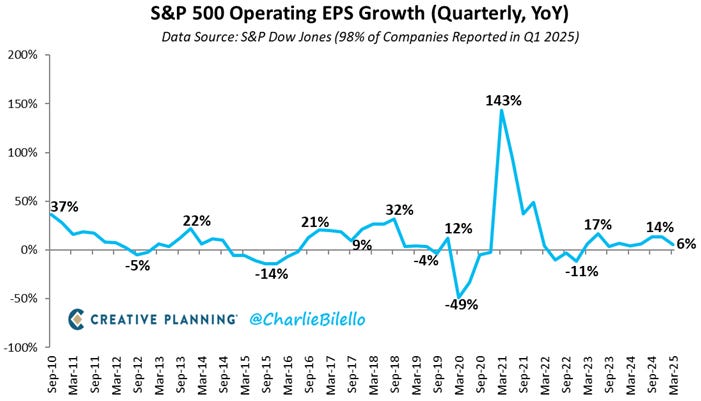

Coming back to equity markets, the S&P 500 saw a 6% increase in Operating EPS this quarter (98% of the companies).

Thanks to Mag 7 (ex-TSLA and AAPL), the S&P 500 have been shy of negative EPS growth. However, one must be cautious as the growth of companies focused on AI is slowing.

Source: Charlie Bilello

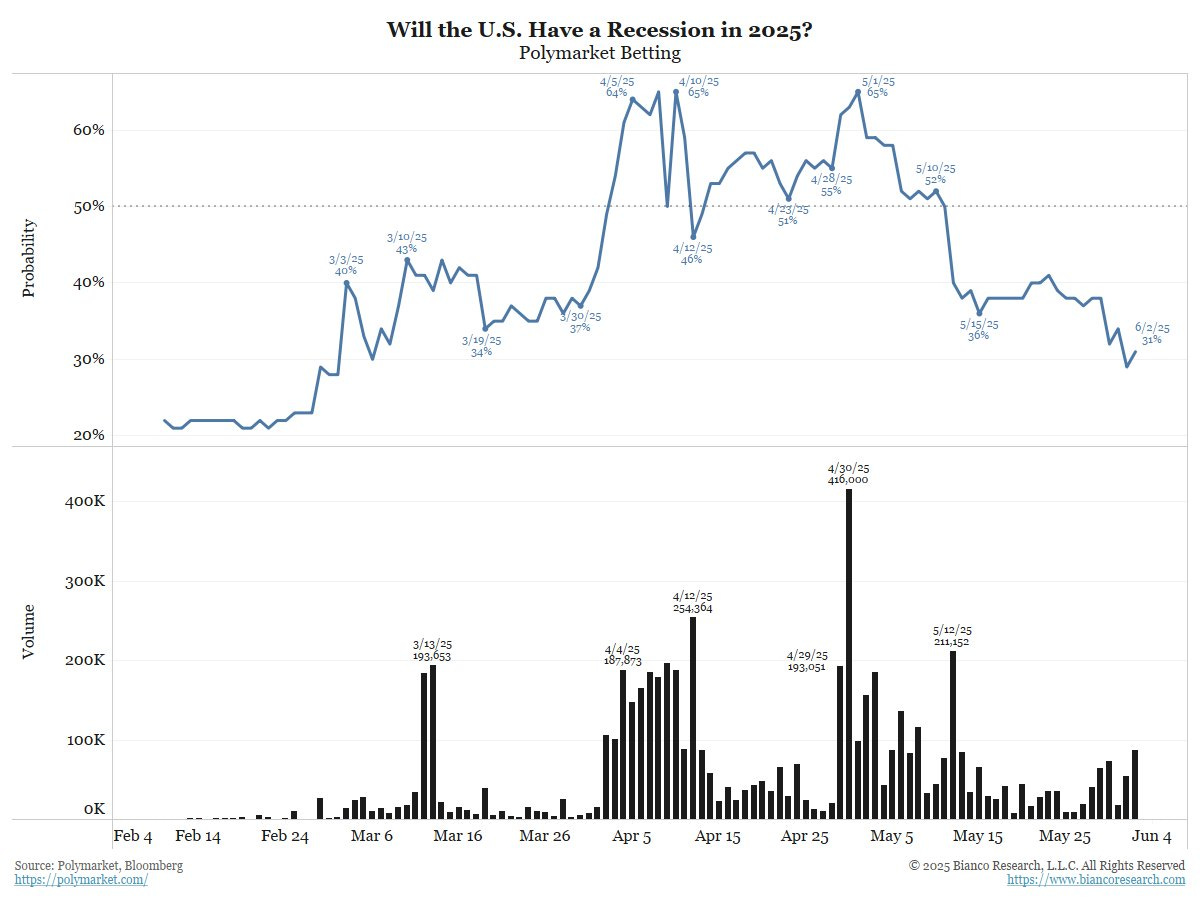

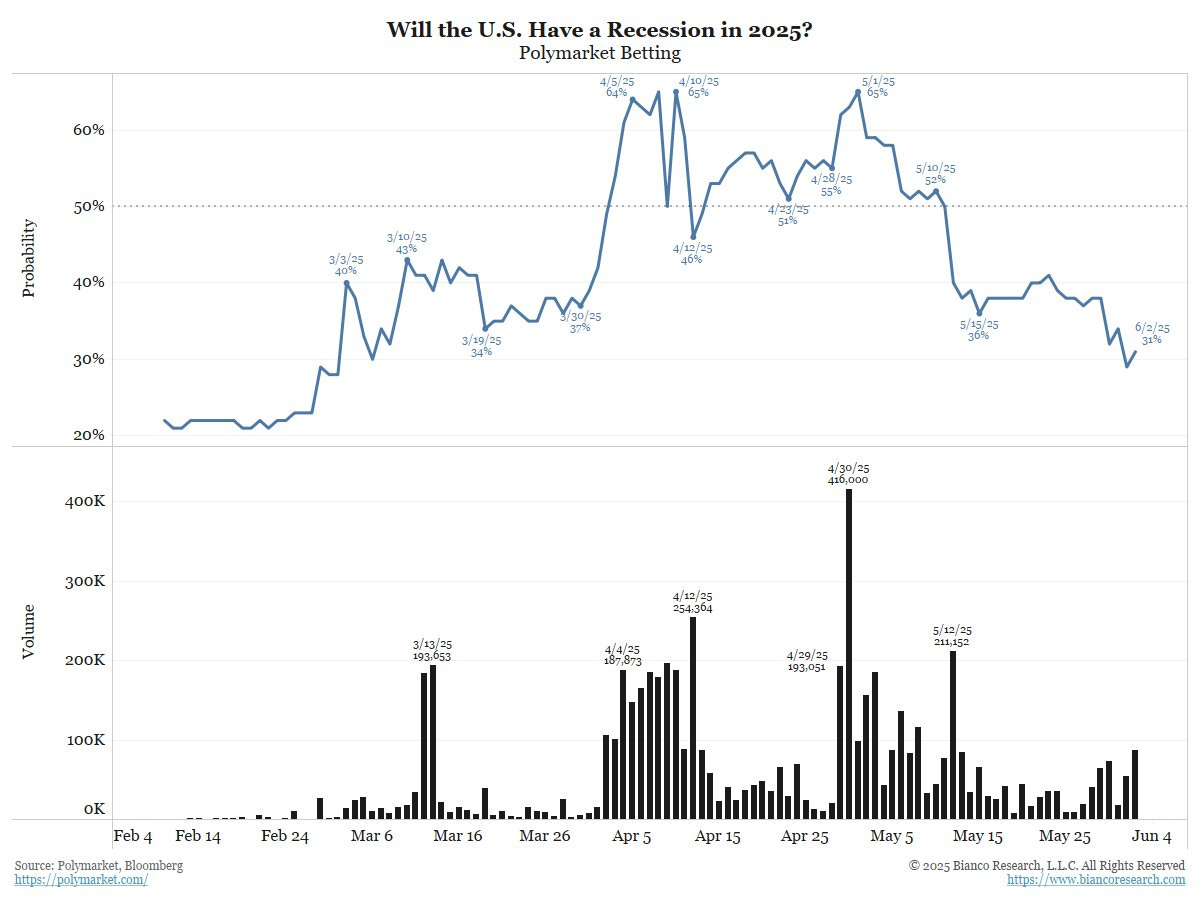

With the equity market recovery, the odds of a recession in the US have plummeted.

The recession odds, as per “Polymarket”, peaked on May 1st (when they reached 65%) and are now down to 31%.

Will the betting markets be right again?

Source: Jim Bianco

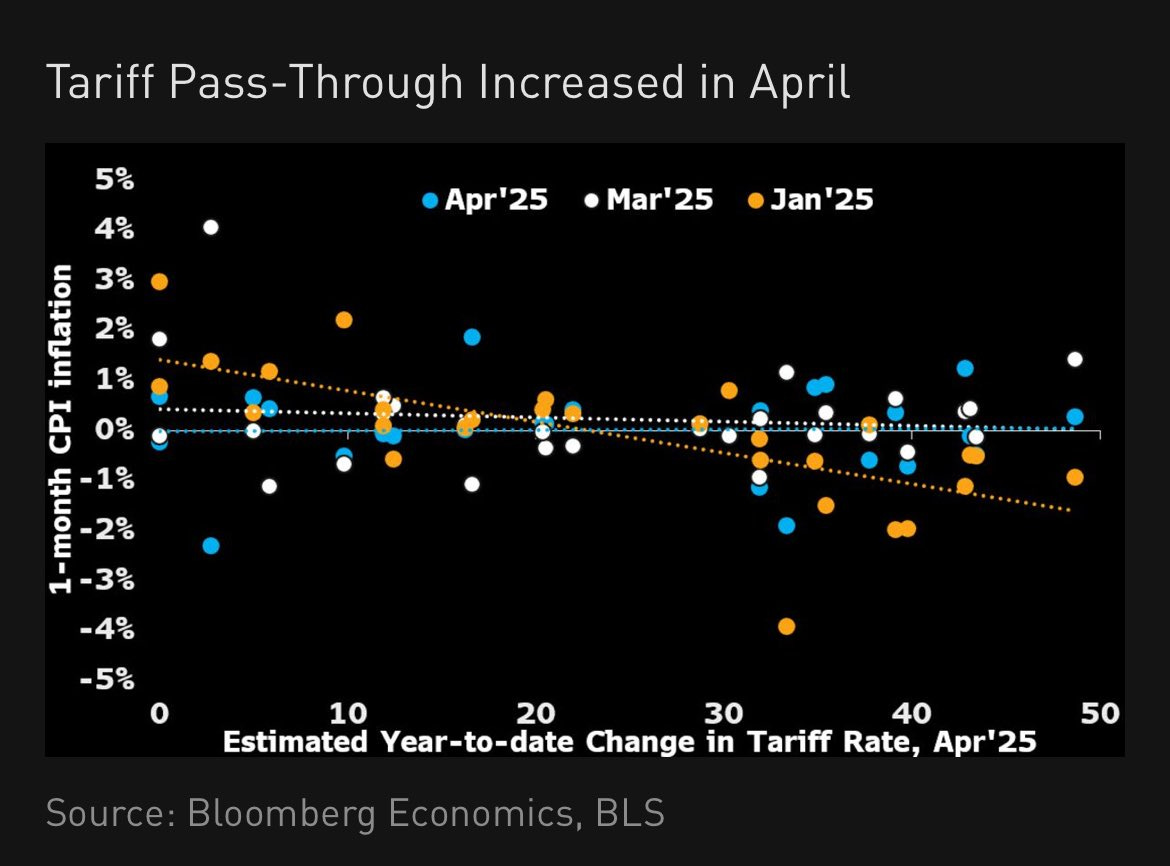

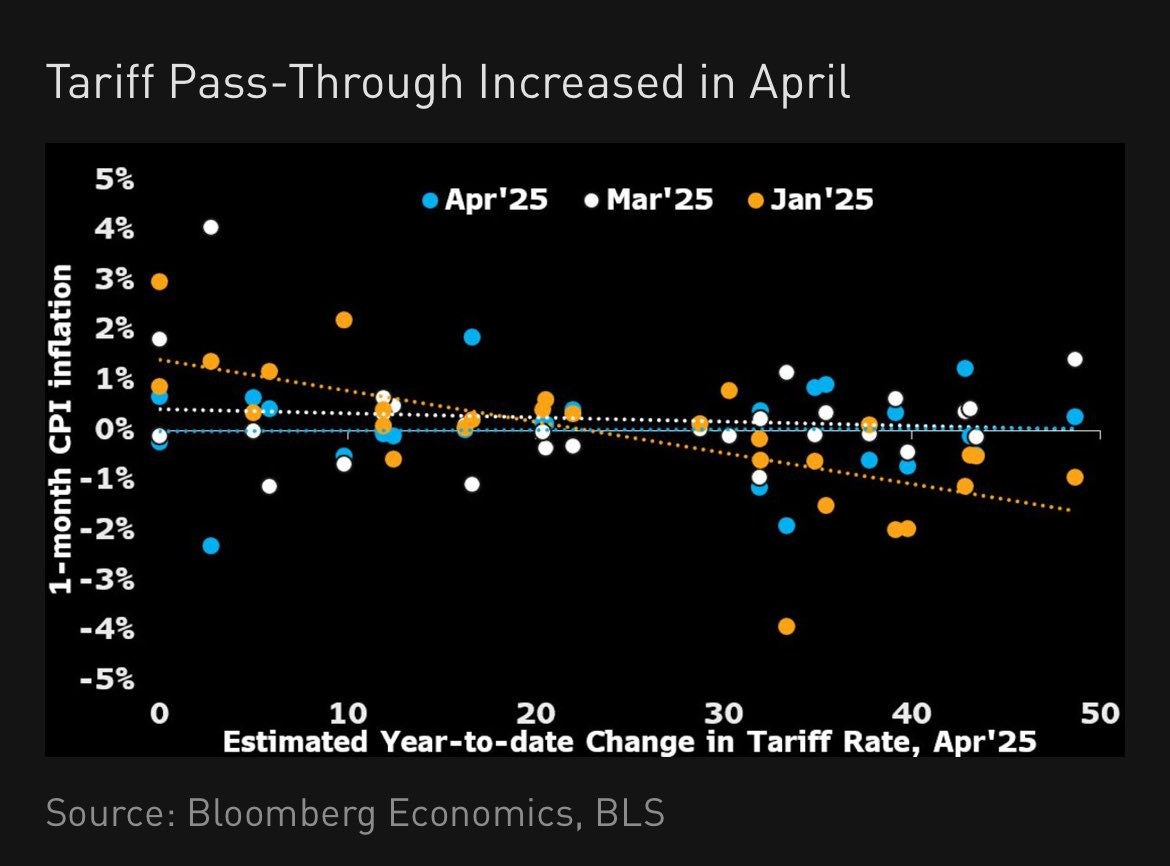

We can’t end the US section without talking about tariffs.

Companies have already passed on the tariffs to consumers in the US as the retail prices of Chinese products have risen.

Nevertheless, one must carefully gauge the impact of the tariffs on inflation, as the weight of the goods basket is smaller compared to the services basket.

Source: FT

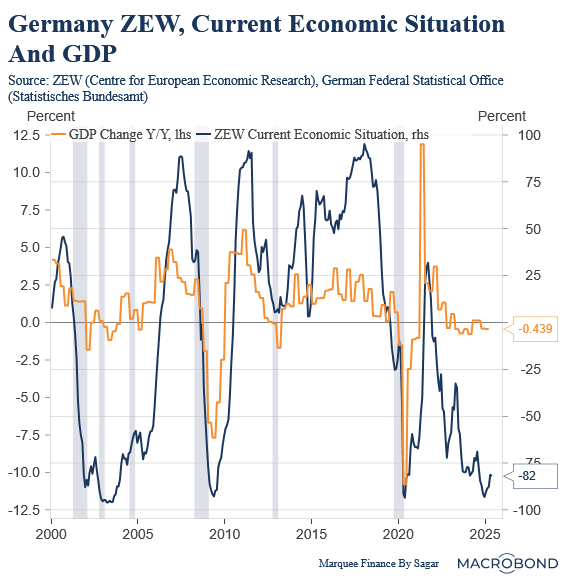

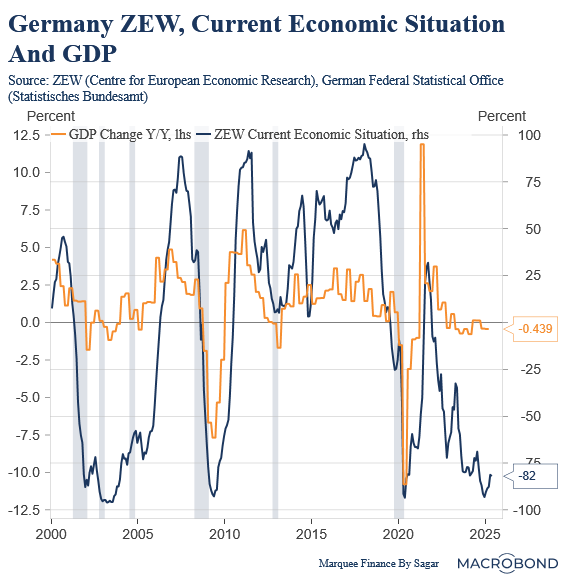

The German economy appears to have bottomed out, according to the soft data.

The ZEW Current Economic Situation index has been on an upward path, despite uncertainty about the tariff situation.

Nonetheless, one must be watchful of the trend in the coming months.

Inflation in the UK came as a surprise, as it exceeded the estimates.

It’s important because this could be the turning point in the inflation trajectory, which has been behaving lately.

Note that the rise in the UK could partly be attributed to the increase in electricity and gas bills.

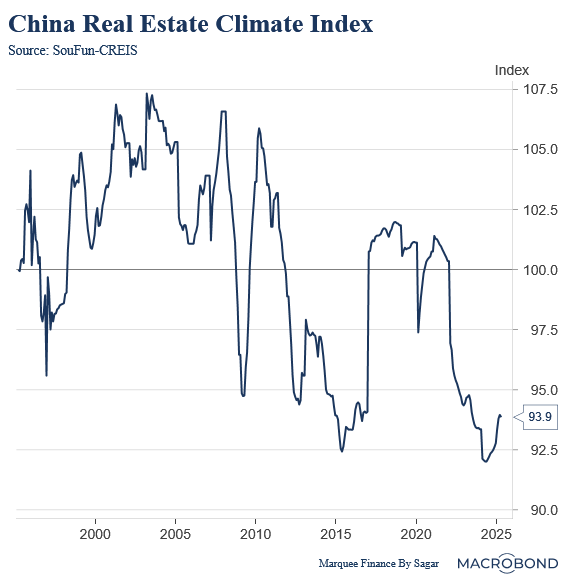

China has reported deteriorating macro data (sluggish manufacturing activity) in the past few days due to the trade embargo.

However, there were signs last month that China’s real estate market has finally bottomed out.

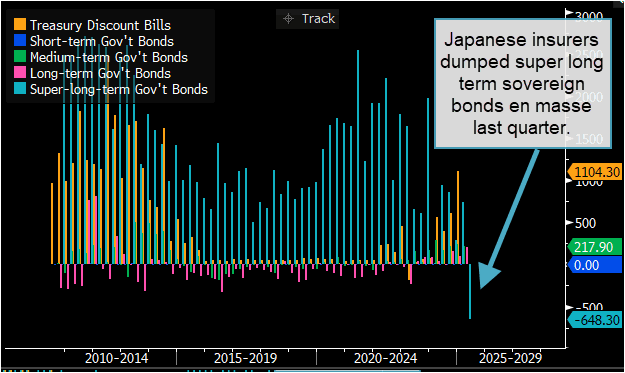

In the land of the rising sun, the bond markets sent global shockwaves after a failed auction led to a massive 20 bps rise in the 30Y Japanese Government Bond Yield (JGB).

Furthermore, the data released by the Japanese Ministry of Finance (MOF) demonstrates that Japanese insurers sold long-term JGBs as market participants raised concerns about the asset-liability management (ALM) of insurance and pension companies in Japan.

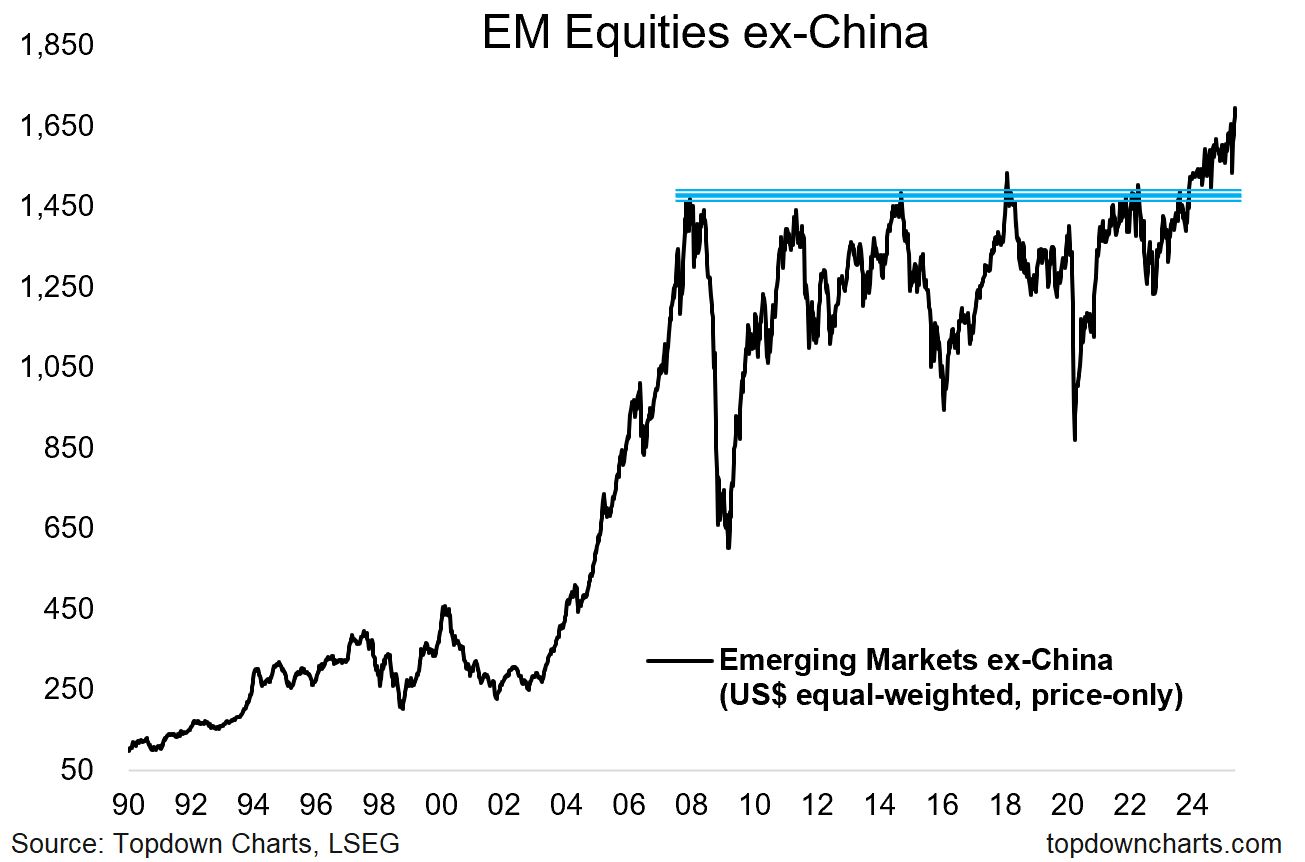

While everyone has been talking about European equities, the EM equities (excluding China) have been slowly breaking out.

It’s partially due to the currency appreciation, but also the valuations, which have been depressed for a very long time.

Some countries in LATAM, Poland, and South Korea have experienced a raging bull market due to political developments.

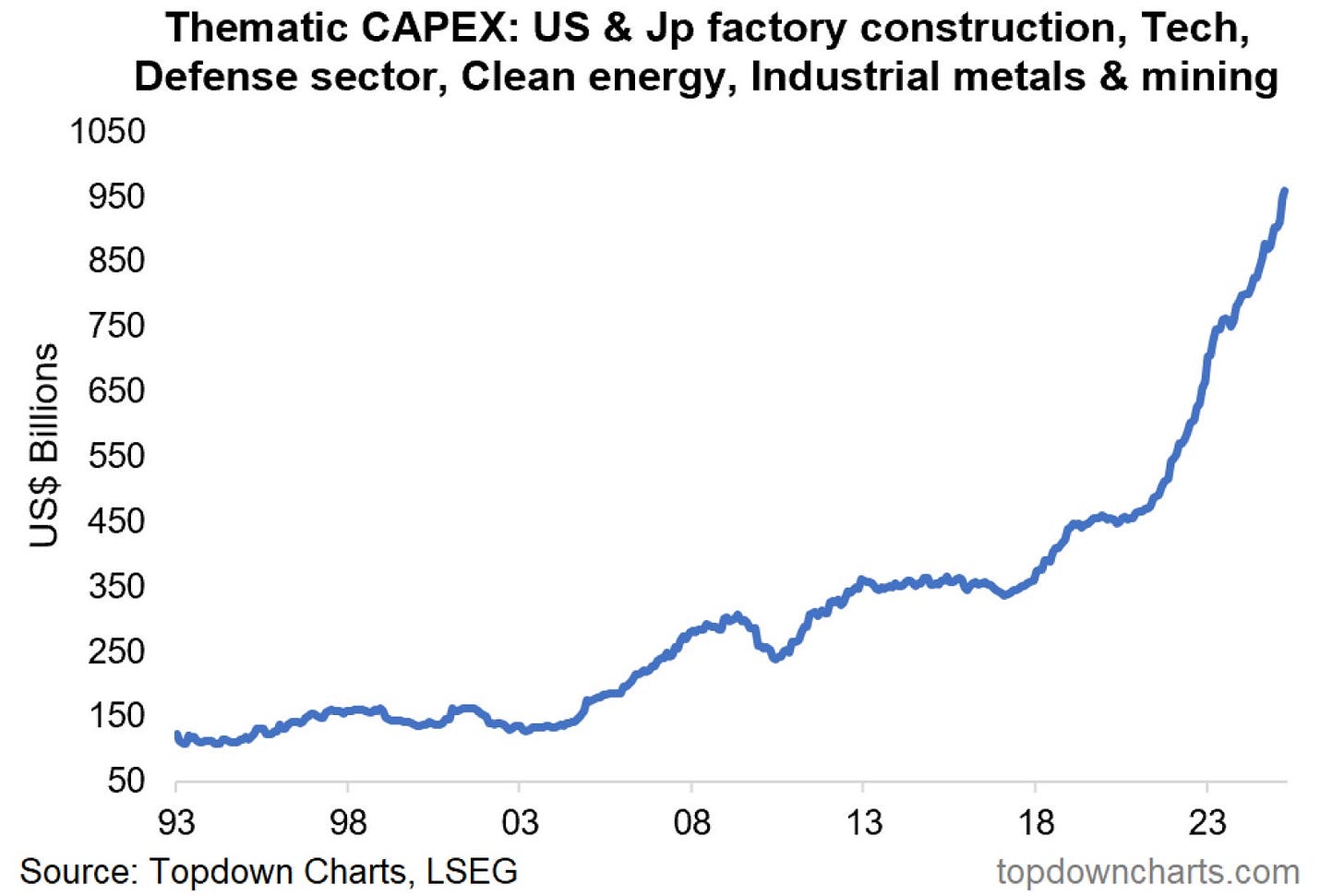

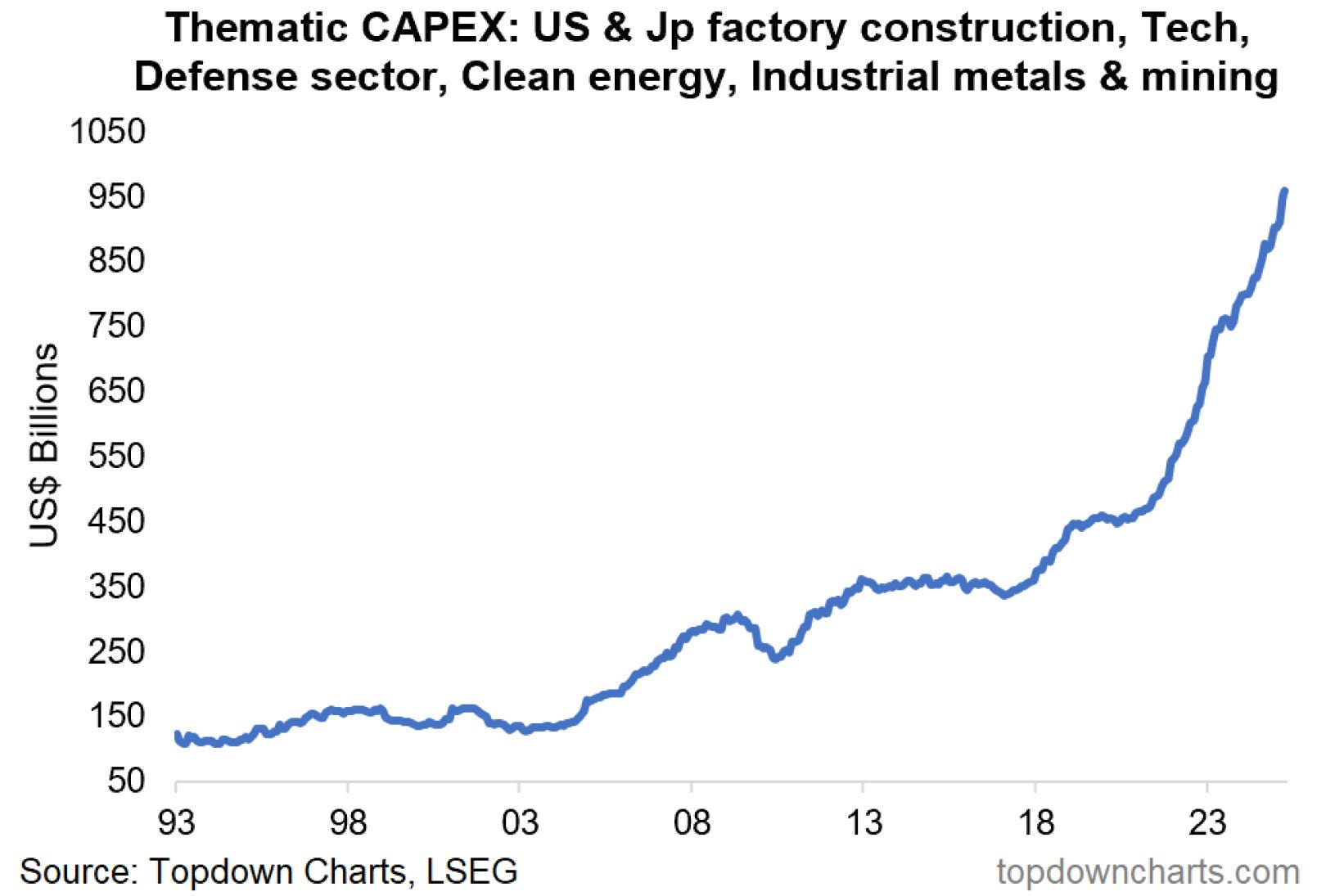

BONUS CHART: After a lull of more than 15 years, we are now witnessing a capex boom across manufacturing. Whether it’s the enormous defence spending in Europe, the chip manufacturing in the US (CHIPS Act), or the clean energy spending globally, the world is unprepared, as only one country holds access to the rare earth metals.

Two years ago, we briefly covered the “Chinese Masterplan.”

PS: We are invested in a few stocks (Thematic Investing bets).

Disclaimer

This publication and its author are not licensed investment professionals. The author & any other individuals associated with this newsletter are NOT registered as Securities broker-dealers or financial investment advisors with the U.S. Securities and Exchange Commission, Commodity Futures Trading Commission, or any other securities/regulatory authority. Nothing produced under Marquee Finance by Sagar should be construed as investment advice. Do your research and contact your certified financial planner or other dedicated professional before making investment decisions. Investments carry risk and may lose value; Marquee Finance By Sagar LLC, Marqueefinancebysagar.substack.com or Sagar Singh Setia is not responsible for loss of value; all investment decisions you make are yours alone.