Regime Change?

“We need greater confidence before we reduce policy rate”- Jerome Powell, 31st January 2024.

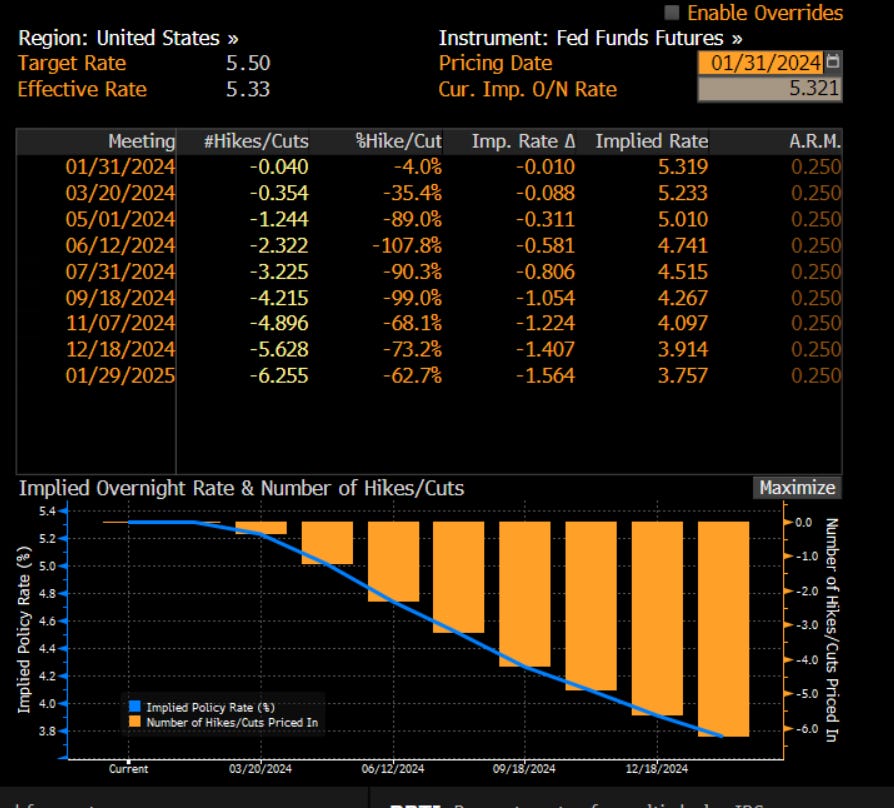

Dashing all hopes of Mr Market’s fairy tale landing, Jerome Powell stunned markets with a hawkish tone in the first FOMC meet of 2024.

Markets took note of JayPo’s words and pushed out the much “anticipated” March rate cut.

JayPo categorically mentioned that the March Rate Cut was not on the radar “yet” as the economic data has been resilient in the past few weeks.

Once again, we were right about the macro trajectory. Since publishing Global Outlook 2024, we have every week mentioned that the March rate cut will be pushed to May/June by the markets, and the consensus call (long-duration bonds) in late December was simply “wrong”.

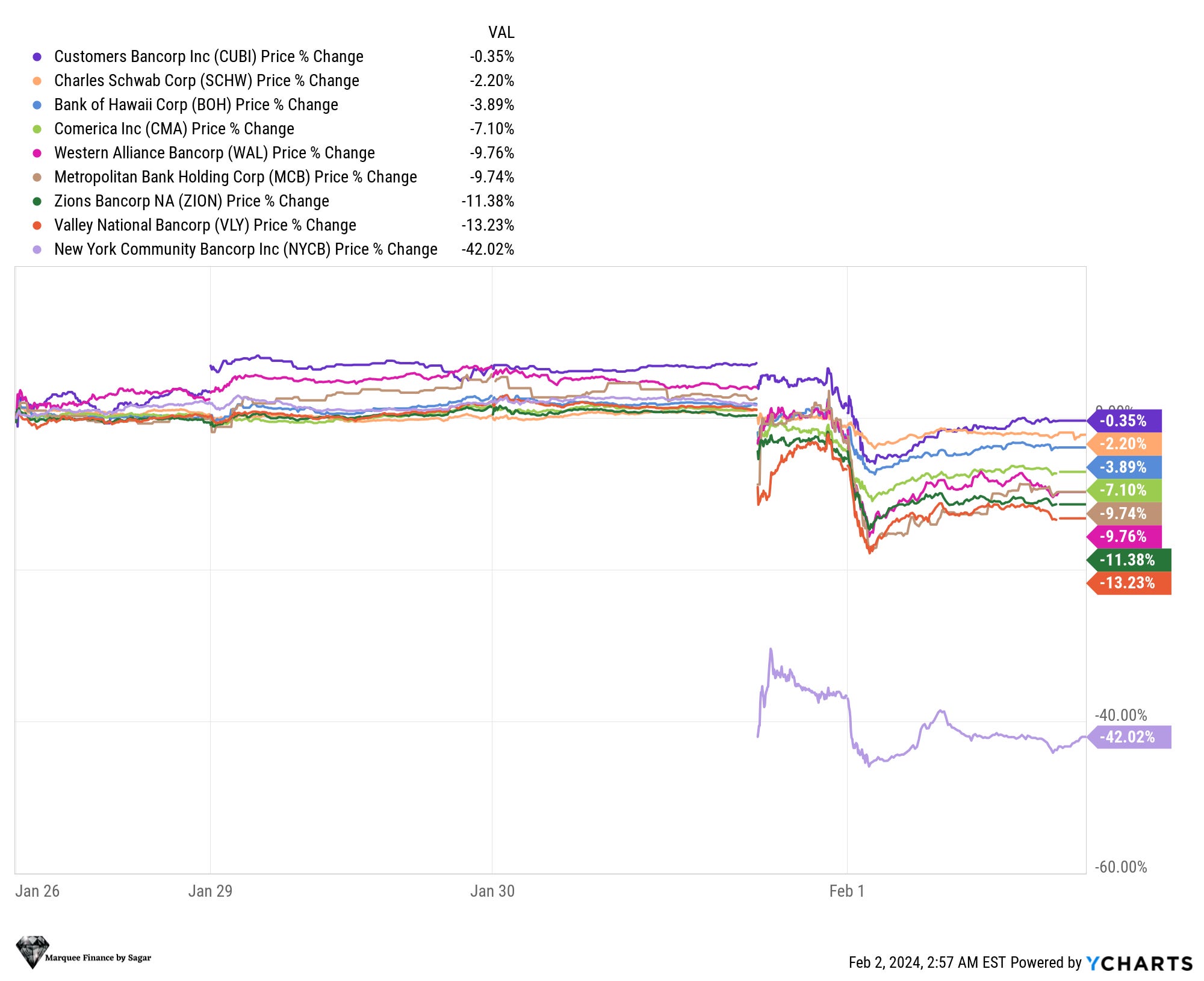

However, despite markets pushing back rate cuts, bonds rallied as the regional bank sell-offs accelerated after the shocker from NYCB.

We also have a very precise opinion in this regard, which we will share later on.

Furthermore, we remain adamant about our guidance about the US economy, which we will explore later.

We will also discuss in detail why we think we are at an inflection point regarding the stock-bond correlation, as our title mentions (Regime Change)!

PS: Before we begin, we wish to inform you that we will increase our paid subscription prices to $24.99/M or $ 249.99/Yr starting 1st March.

Note that the subscribers who are currently enrolled or will enrol by 1st March will be subscribed at the mouth-watering current prices ($14.99/$149.99) “FOREVER”.

So, somebody who wants to take advantage of a massive 40% discount for a lifetime can subscribe till midnight on 29th Feb at the current prices.

Let us begin!

The US!

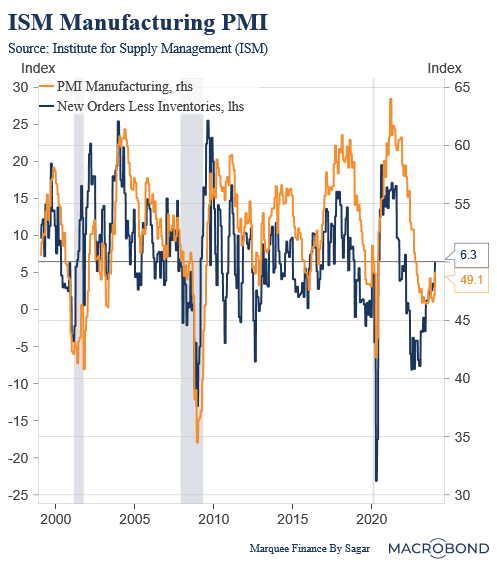

Let us begin with our favourite leading indicator of the cyclical economy, which has now been in a contraction for 16 consecutive months (the third longest in history).

My favourite measure, New Orders Less Inventories, has jumped significantly higher as new orders moved back above 50.

The manufacturing strength as we have mentioned earlier as well can be attributed to the CHIPS and Inflation Reduction Act.

As a result, higher fiscal spending is directly contributing to the recovery in the manufacturing/ cyclical economy.

Nonetheless, while the headline number is strong, the higher prices paid is a red flag, which indicates that the pricing pressures exist in the economy.

Furthermore, the employment component came in at 47.1, which exhibits a weaker labour market in the cyclical economy.

Undoubtedly, the biggest event of the week was..

Keep reading with a 7-day free trial

Subscribe to Marquee Finance by Sagar to keep reading this post and get 7 days of free access to the full post archives.