The Big Short 2.0?

“How did you go bankrupt?”

“Two ways. Gradually, then suddenly.”- Ernest Hemingway.

The recent events that have unfolded in the last month have everyone left wondering about the dominos that will fall next as the transmission of the unprecedented tightening of the monetary policy slowly seeps into the economy.

Analysts, journalists and other famed market participants have now begun to scratch their heads and use their microscopic lenses to look in detail about the next time bomb to explode in the financial markets.

If you haven’t watched the movie “The Big Short” until now, I recommend watching it first thing this weekend and comprehending the nuances of how Michael Burry uncovered the cracks in the housing market (subprime mortgages) at a time when the markets were still in the bull run.

Today, the story is entirely contrasting. Nobody in the markets knew where the risks lay until SVB blew out. The deposit flight was happening for the last six months, but indeed it accelerated post the SVB fiasco, and now the regulatory authorities are well prepared for the worst-case scenario.

Commercial Real Estate (CRE) risks are spreading like wildfire and taking centre stage among online communities.

Nevertheless, are the market participants again looking at the wrong corner?

Today, we will dig deep to understand how material the CRE risks are and where the real Big Short 2.0 lies!

Let’s understand!

Commercial Real Estate (CRE)-Background!

Much has been said and written since the last fortnight about CRE as market participants scrutinize the sector and the exposures in detail. A lot of data and number crunching indicates that the situation is grim and warrants attention.

Nevertheless, though the situation is alarming but is manageable.

First, let us understand the CRE market, and then we will move on to the exposure and the banks.

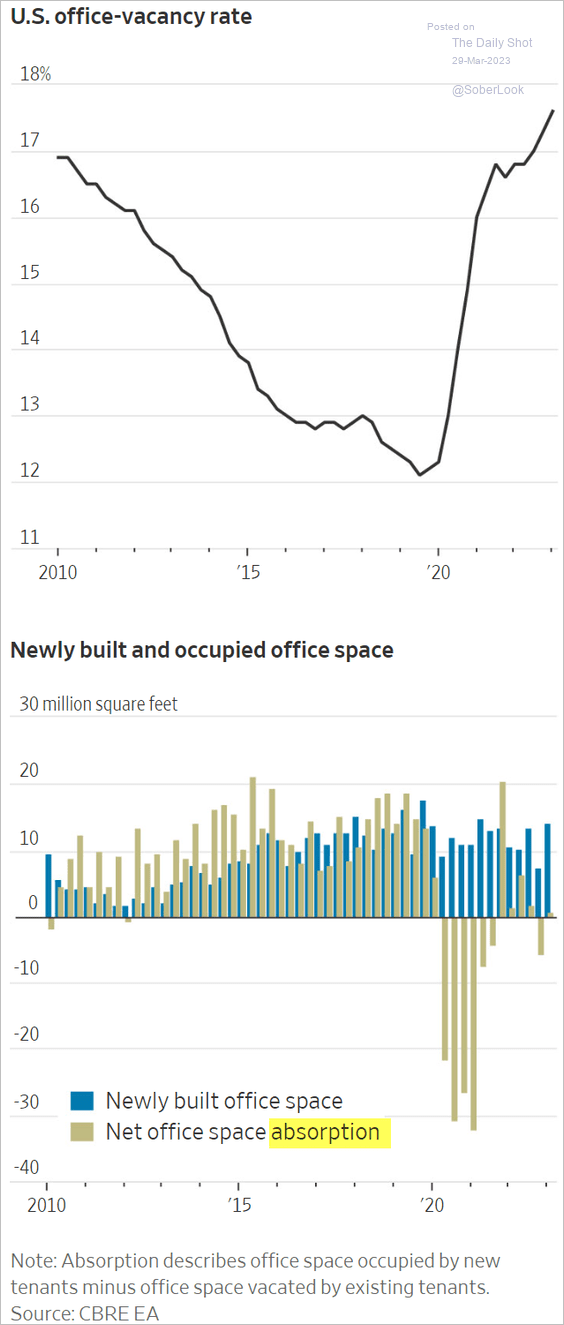

CRE market is divided into office spaces, retail, hospitality (lodges/resorts), storage, data centres, hospitals etc. The problem area for the CRE market has been the office spaces since covid. Though initially, since travel halted due to the lockdowns and restrictions, other markets also suffered setbacks.

Nonetheless, retail and hospitality have rebounded sharply as the economy has been strong and the pent-up demand surprised on the upside. However, the office spaces have been languishing.

The hybrid mode of work, ample supply, rising vacancy rates, sky-high refinancing rates and stagnant rents have exacerbated the pain for office space developers and REITs (Real Estate Investment Trusts).

The vacancy rates have climbed to the GFC levels as net office space absorption has remained negative for most of the time post covid.

As the talk of an impending recession grows, the sentiment remains weak, and companies resort to slashing costs with layoffs and surrendering the extra office spaces. Thus, the outlook remains negative, and the recovery uncertain.

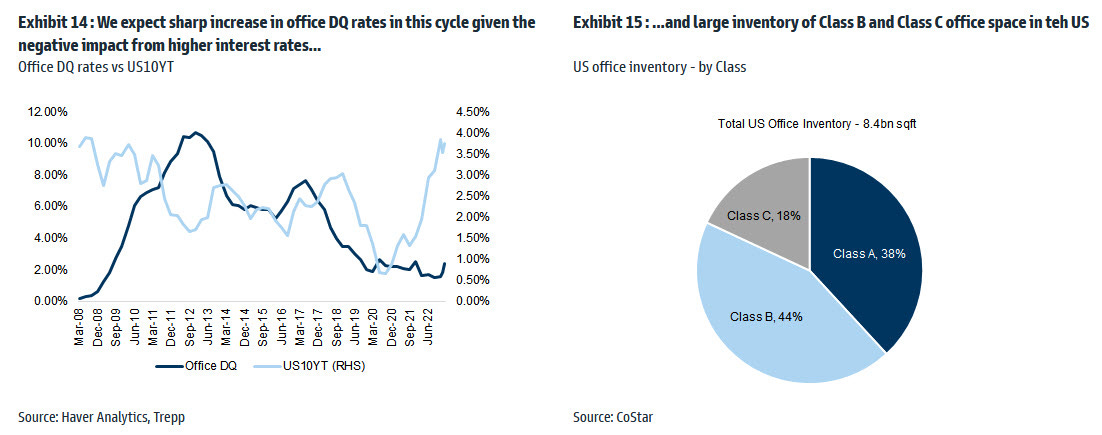

Nevertheless, the delinquency rates (DQ) remain low as of now, as the defaults are expected to rise whenever the loans are due for refinancing.

As we can see that the office DQ rates reached highs in 2012. This is because, as I mentioned, the developers default whenever the loans reach maturity, and thus the DQ rates rise with a lag.

So the million-dollar question is: When do the maturities come?

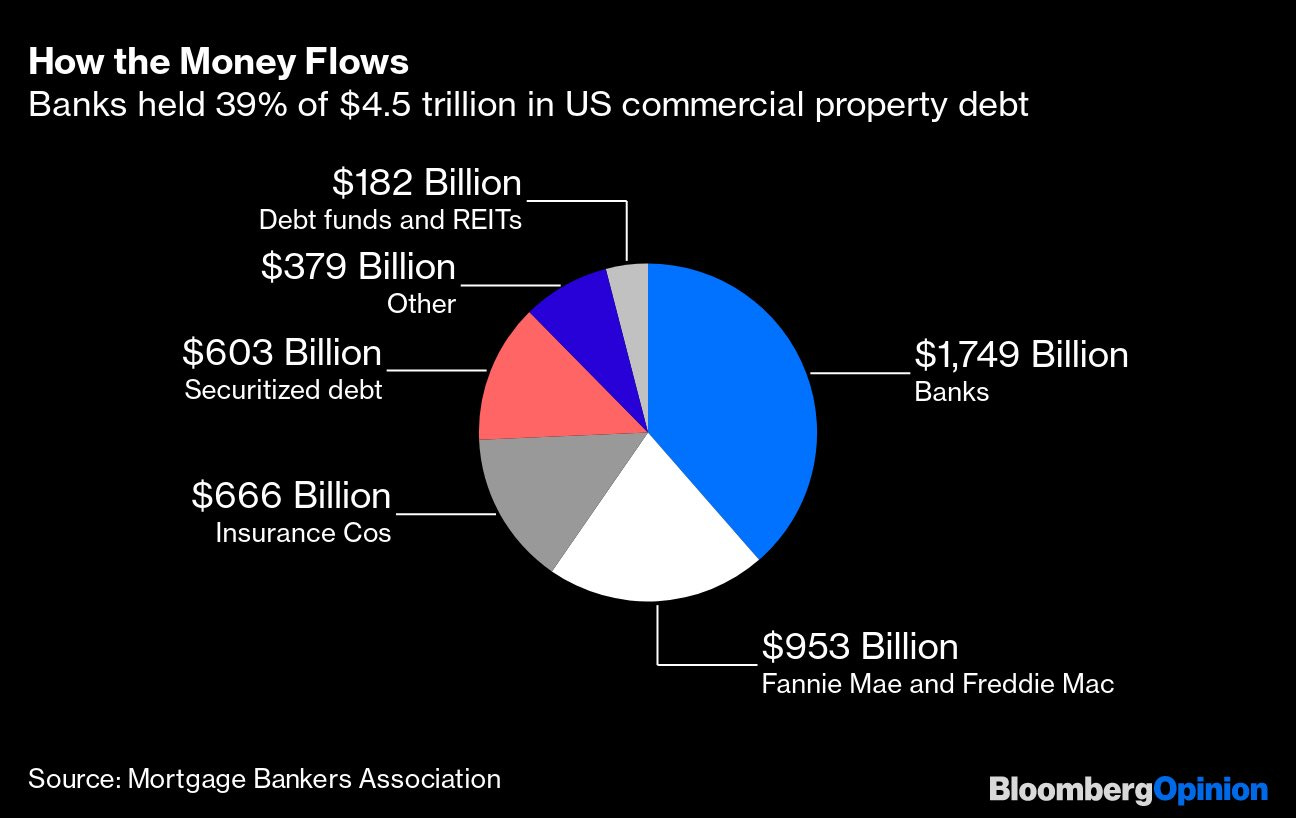

The total CRE market is $11 trillion, of which $4.5 trillion is the total outstanding debt. However, as we all know, the stress is visible only in the office space while the rest of the CRE market is resilient. Nevertheless, the situation might change if a hard landing ensues.

As per market participants, the total office space debt is around $1 trillion.

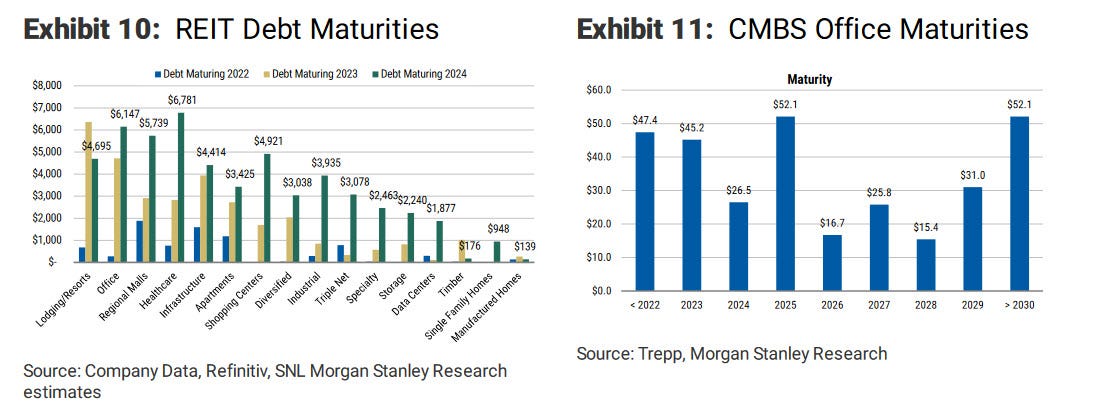

The office space REIT has a debt maturity of around $5 billion this year, while $45 billion worth of CMBS (Commercial Mortgage Backed Securities) is due for maturity.

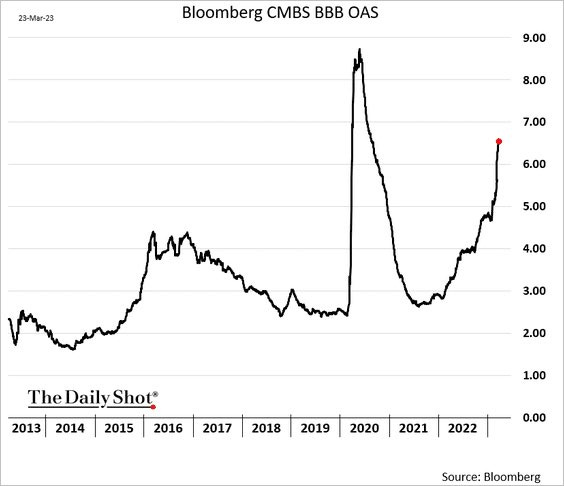

The markets are pricing in an imminent default for the CMBS as the price action here is getting really scary. The OAS (Option adjusted spreads) on CMBS have started to blow up.

The Exposure!

The bank’s exposure to the CRE market is roughly 39%. On the other hand, Fannie Mac and Freddie Mac and the insurance companies, hold the second and third largest exposures, respectively.

Nevertheless, the office space CRE exposure is of our prime concern. While banks may have less overall exposure, the real worry lies when we dig deeper into the bank’s balance sheets.

There are two parts to the equation of a bank’s balance sheet:

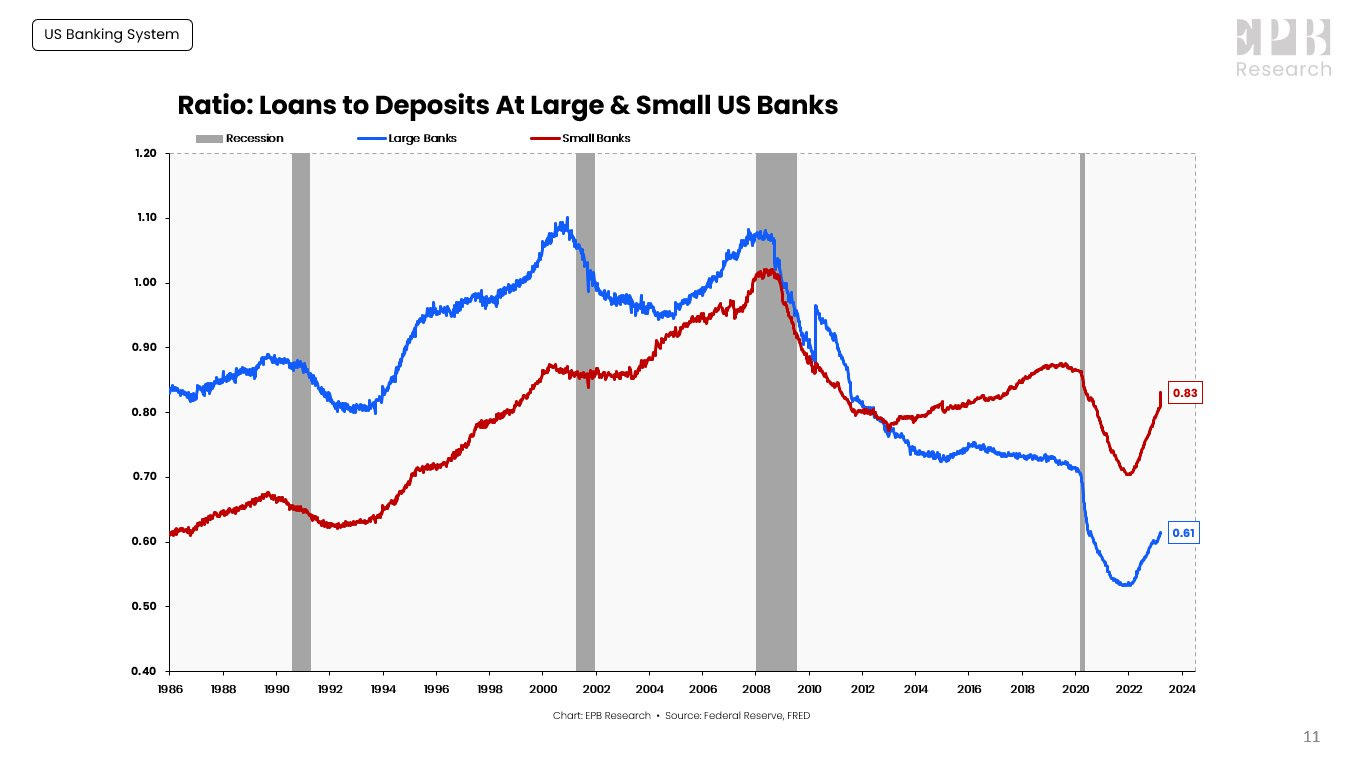

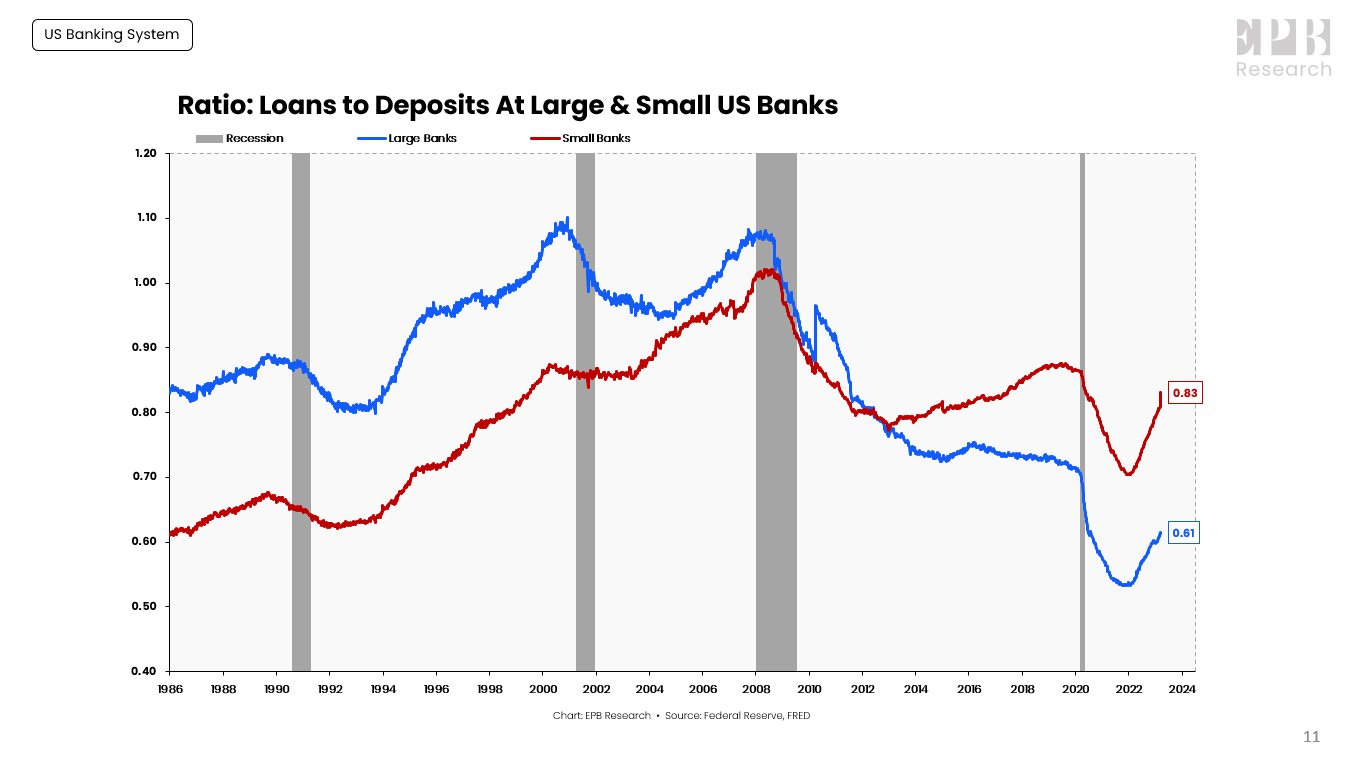

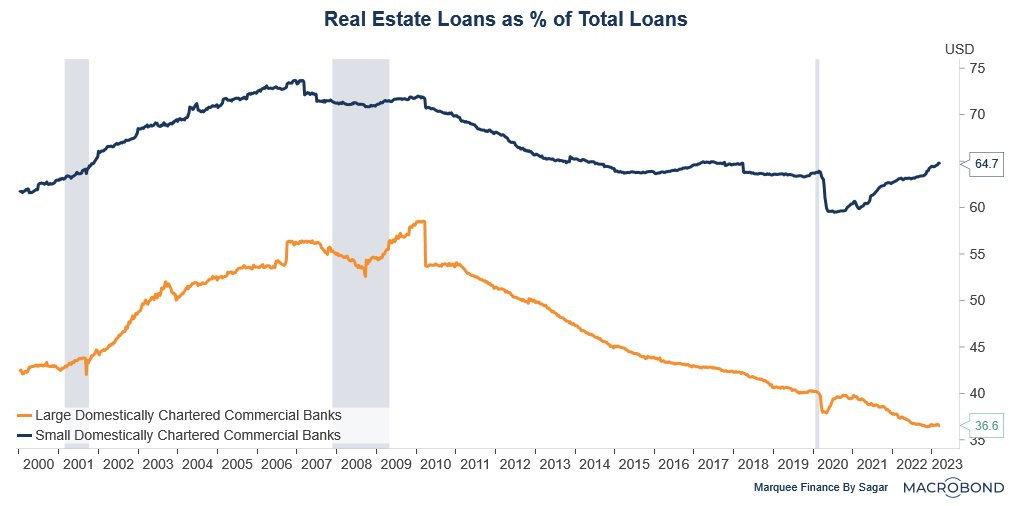

First, loans as % of total assets have remained higher for smaller banks post-GFC while having fallen for larger banks, thus making smaller banks vulnerable to solvency risks in times of extreme credit stress. Furthermore, loans to deposits ratios are significantly higher for small banks than for large ones.

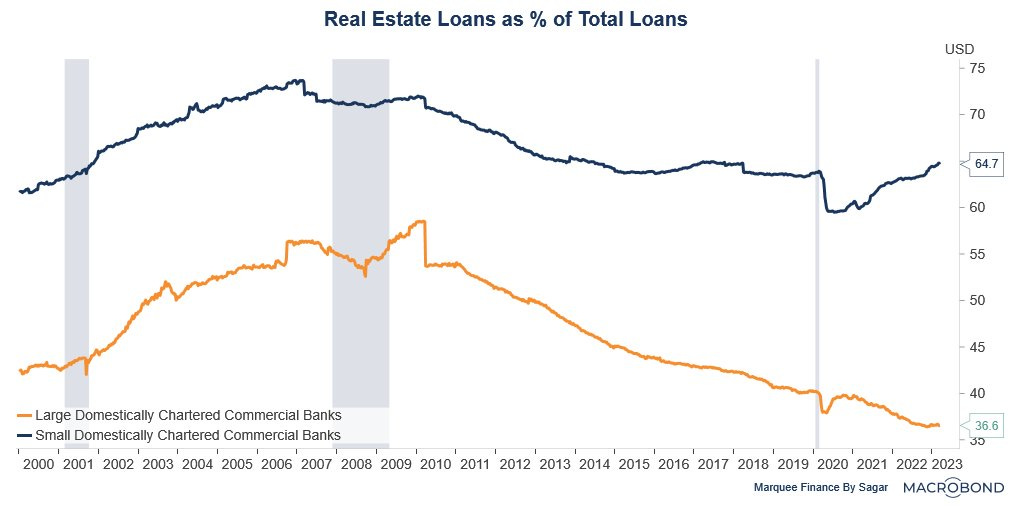

Source: EPB Macro The other notable feature is that smaller regional banks heavily concentrate their lending towards real estate loans while the larger banks have diversified their loan books.

Source: Macrobond

On top of it, smaller banks surprisingly have around 67% of their total real estate loan exposure to CRE, while 33% is towards residential RE.

As a result, 43% of the total loan book of smaller banks is towards the CRE space, which is highly concentrated for banks that are lifelines to the US economy.

Residential loans were doled out at a fixed rate for 30Y when rates were as low as 1%. In fact, banks are earning virtually nothing on their residential loans, and looming defaults will plague the office CRE loans.

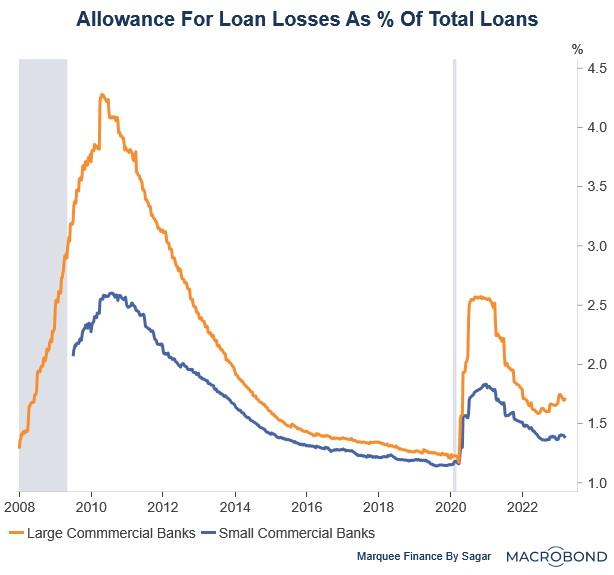

Furthermore, small banks have already provided less for loan losses as of now; I expect this to zoom more than the peak in 2010 as loans go sour.

As a result, we might see some nasty losses for regional banks in the coming quarters. The loan losses will be enormous whenever the delinquencies rise for CRE, personal loans, auto loans (DQ rates are at an all-time high here) and credit cards.

Thus, it’s a no-brainer that smaller banks are facing multiple headwinds, from deposit outflows to contraction in Net Interest Margins (NIMs) to most probably rising loan loss provisions in the future.

Overall, small bank failures have just started, and we will see 100s of bank failures in the next two years.

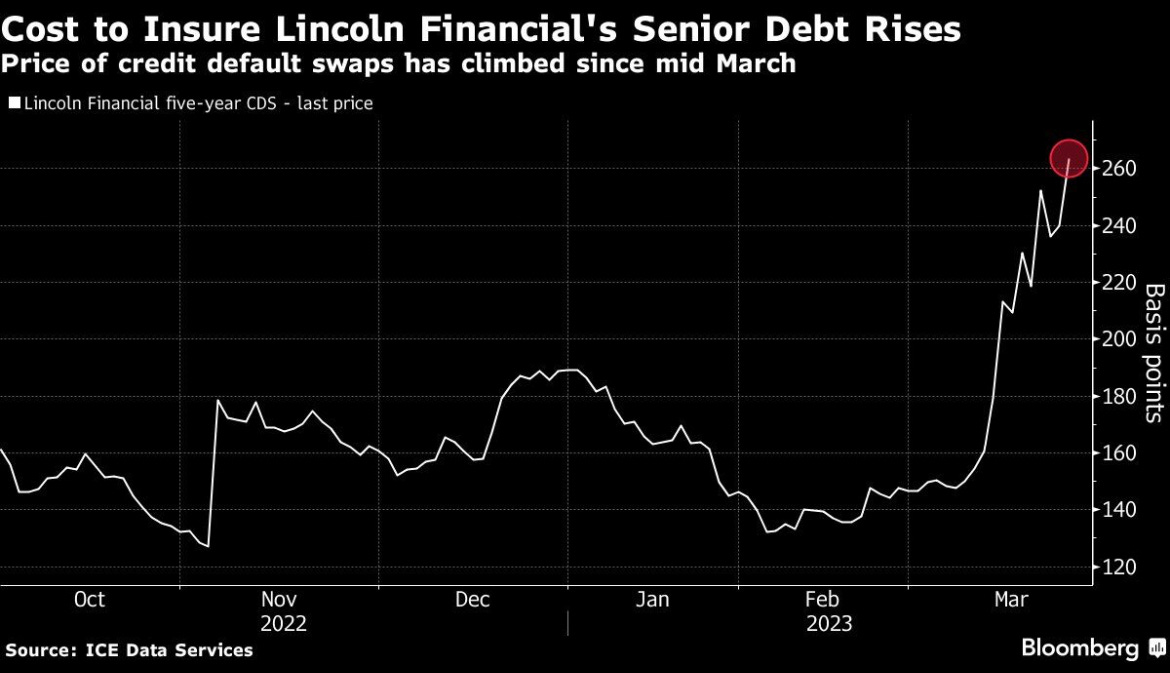

Next in line are the insurance companies. Though I am not an expert on how insurance companies manage the risks, especially the duration risk, insurance companies have $666 billion of CRE exposures.

Weak links will also undoubtedly break here, and some of the small players might go belly up.

The markets seem to be concerned about a certain name which is doing rounds on social media.

It’s Lincoln Financial.

Thus, as with every other, this cycle will see significant bank failures.

Nevertheless, the real risk lies elsewhere.

Canary In The Coal Mine: The Big Short 2.0?

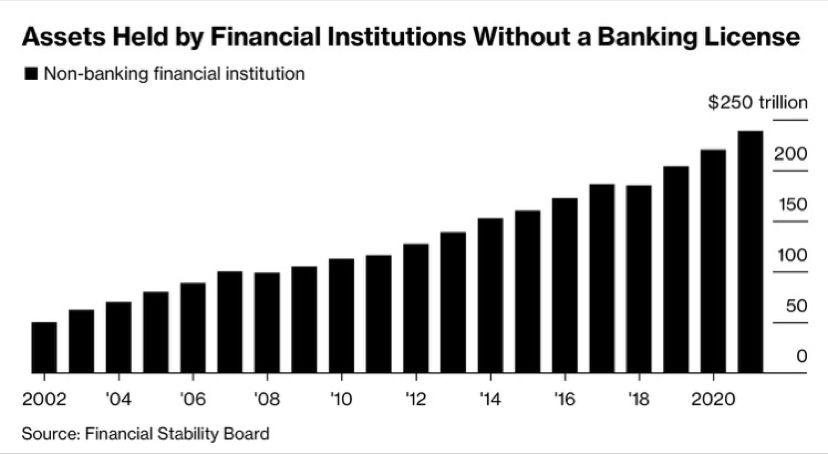

Folks, the real risk in our financial system lies in the Private Credit or, as some people like to say, it as “shadow banking” (as these don’t come under regulatory purview)

The risk is magnified as the shadow banks have been the biggest lender to the opaque and obscure private equity and the VC space. In fact, private equity was the space which has benefitted the most from the ZIRP (Zero Interest Rate Policy) post-GFC.

If we talk globally, the shadow banks hold a gargantuan $250 trillion of assets.

Most of this money likely flew into illiquid startups that have seen their valuations crash after the CB tightening. (incremental money)

As per Bloomberg:

“An increasingly popular area is net-asset-value lending, a type of borrowing where buyout firms raise money against a bundle of assets they own. As sponsors struggle to sell businesses amid rising rates and challenging financing markets, they increasingly rely on such loans to shore up portfolio companies and keep distributing money back to their investors.”

Liquidating the assets when the valuations have crashed, and when the appetite for fresh funding in loss-making tech remains low means taking a massive haircut. Lenders often find no buyers for the assets, which may exacerbate the problems.

Since our financial system is interconnected, a rout in the shadow banks might lead to a “ credit event”.

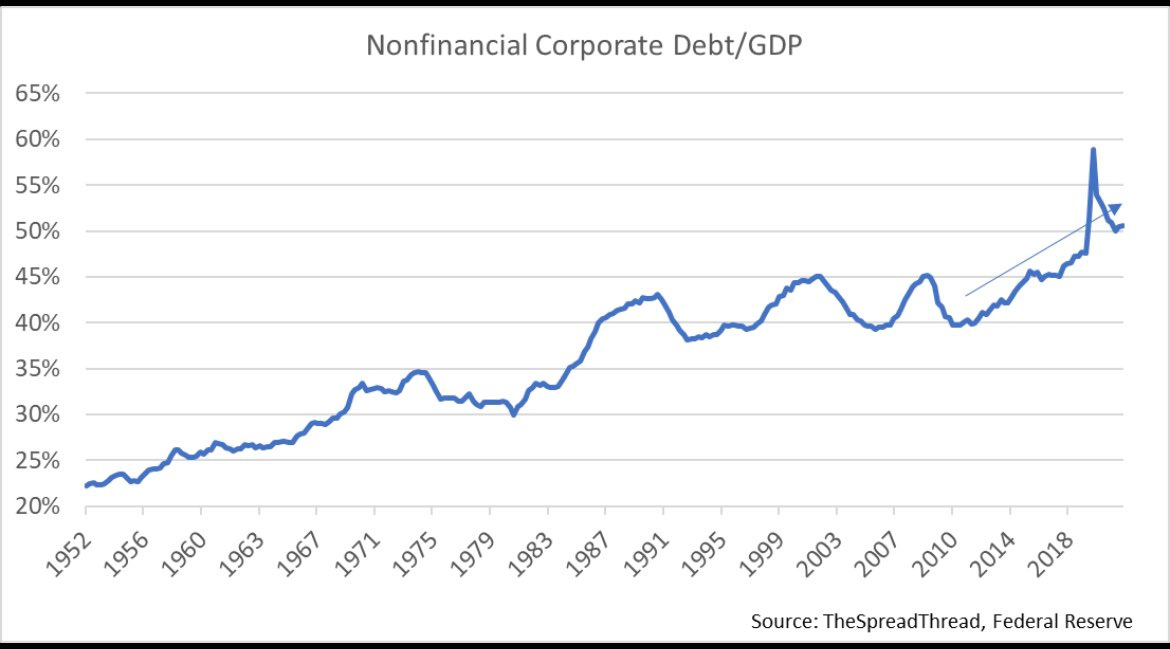

When we talk about the US, there is a notion that the corporates have delevered post the GFC; however, when we dig deep, the non-financial corporate debt as % of GDP has climbed to more than 50%.

And guess what?

The leverage came from:

Non-Financial BBB Bonds, which are up 3X since 2008 GFC.

Leverage Loans which are up 2.5X

Private Credit from virtually zero to $1.3 trillion!

PS: Data from TheSpreadThread Twitter

The low-interest rate regime, coupled with the massive liquidity expansion via QE by the CBs, led to “hidden” leverage which inflated assets in the zombie space.

Somewhere today in the US, a new Michael J Burry is born! :)

Conclusion!

If a credit event leads to a hard landing for the US economy, the vacancy rates will likely jump to 25%-30% with a lag. It will be mayhem across the CRE space (office) in that scenario.

This may also lead to a long-term setback for the construction sector as developers will go extremely slow in building new office spaces.

The construction spending on office buildings is presently 10% or $96 billion of all non-residential construction spending in the US. At the heights, this was 11% compared to 6% post-GFC.

The office defaults should peak somewhere in 2024/2025, considering the lag of covid and the tight monetary policy/higher interest rates. Furthermore, I believe this time, the share of office space can fall below 6% because other components of CRE (Ex-office) "might" remain resilient due to changing consumer preferences.

Note that spending has changed to services, particularly travel and leisure, instead of goods post covid.

Thus, retail and hospitality have been outperforming office spaces.

The real Big Short 2.0 lies in the unregulated private credit space and is the largest lender to the frothy Private Equity and VC space.

The warning signs are all over the place, and it’s time to be cautious, especially on regional banks, sectors connected to the Private Equity and VC space, other cyclical sectors and REITs.

Disclaimer

This publication and its author is not a licensed investment professional. Nothing produced under Marquee Finance by Sagar should be construed as investment advice. Do your own research and contact your financial advisor before making investment decisions.

You gave the example of Lincoln Financial but indicated that this is not where the real risk is. But it would be helpful to know more about the risk of CRE exposure among insurance companies for the simple reason that this helps one move towards an actual shorting strategy. For example, an investor could simply buy long PUTS on Lincoln Financial and presumably other insurance companies as well.

But for your broader conclusion about the risk of CRE as a whole, and in particular as pertaining to regional banks, getting to an actual shorting strategy is considerably more difficult.

I wonder if hundreds of small banks will go down as you predict here.

It seems like the last sentence of this paragraph is doing a lot of heavy lifting here:

The total CRE market is $11 trillion, of which $4.5 trillion is the total outstanding debt. However, as we all know, the stress is visible only in the office space while the rest of the CRE market is resilient. Nevertheless, the situation might change if a hard landing ensues.

If office space blows up but overall CRE space is OK, is this still a systematic problem that will lead to 100s of bank failures?