The "Disruption"!

Months after the deadly virus caused havoc around the globe in 2020, most economists and central bankers declared that inflation was “transitory” and was led by once-in-a-century lockdowns that distorted the supply chain beyond anybody’s control.

In fact, it took more than 24 months for the entire supply chain to heal, and in the process, the goods inflation reached unprecedented levels in the developed world.

Nonetheless, the 70s experience reveals that occasional “disruptions” in global trade (note that we are more globalized than ever today) lead to bouts of inflationary episodes irrespective of the demand scenario.

Though low demand can cushion the blow of disruption and reduce the time frame eventually, it leads to crashing margins and thus earnings for the companies with low “pricing power”.

Furthermore, market positioning across assets (thanks to leveraged bets) can witness a shakeout, and the “pain trades” across assets get exacerbated “swiftly.”

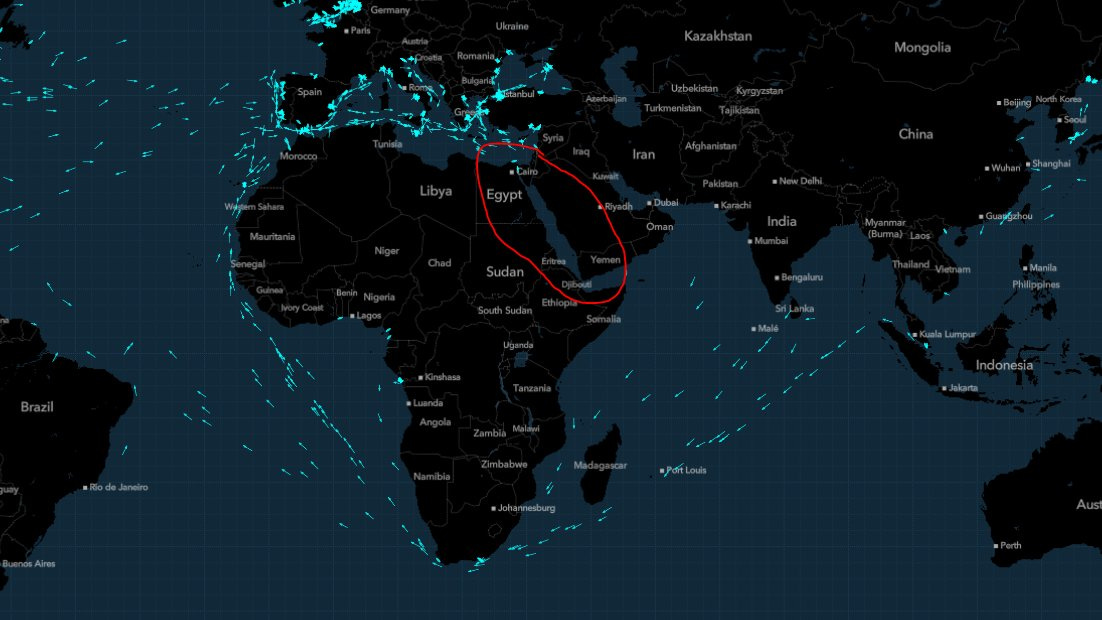

As discussed in the global outlook, geopolitical concerns are again at the forefront, and we are witnessing unusual “disruption” across one of the major shipping routes in the world.

Today, we will look at the extensive economic data released worldwide and analyze how the current “disruption” affects the growth/inflation dynamics, with its effect across assets.

Let’s go!

US!

We start with the crucial economic data which was released in the US.

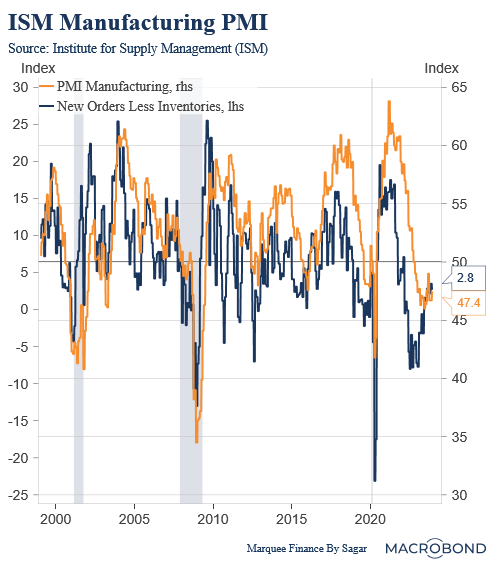

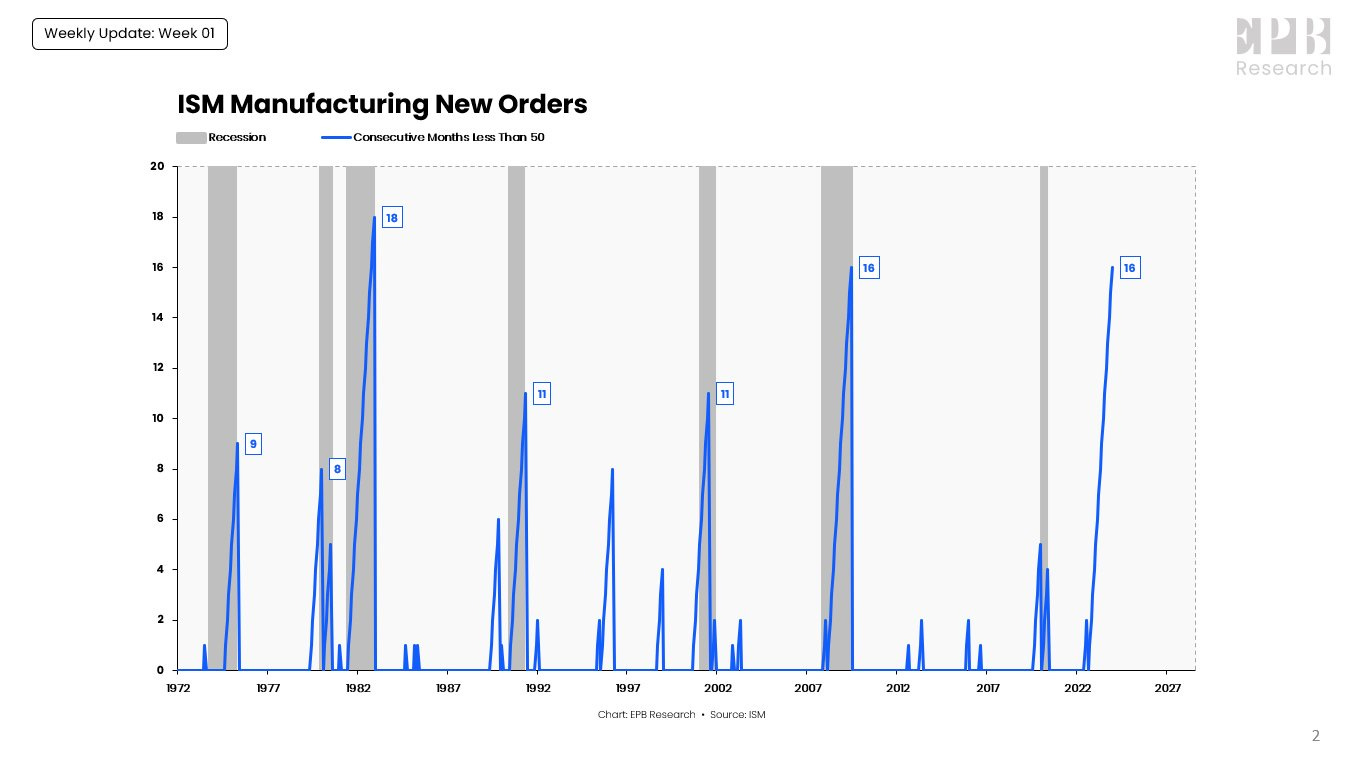

Long-time readers would remember that ISM Manufacturing remains my favourite “leading” indicator to gauge cyclical activity.

ISM Headline number came broadly in line with estimates, and the new orders less inventories data also implies a stagnation at the current levels (though in contraction territory).

Nonetheless, the New Orders have been less than 50 for 16 consecutive months, which is comparable to the 2008 GFC and the second largest since 1982.

The long stretch can partly be attributed to the excesses of the covid, which led to an enormous rise in inventories.

Though goods manufacturing has been weak, the manufacturing sector has seen a big boost from government measures, namely the CHIPS ACT and the Inflation Reduction Act, which is keeping the activity buoyant (IMO, we would have got an ISM number below 42-44 if it had been absent).

Nevertheless, we will closely monitor the data as the year progresses.

Moving on, today’s biggest concern is the geopolitical events transpiring in the Middle East.

Some people would argue that it would have been a non-event, but in my opinion (IMO), things have gotten too far this time (though de-escalation can always ensue).

Long-time readers will reckon I am a big believer of “mean reversion”. The three charts which point out “painful” mean reversion are:

Keep reading with a 7-day free trial

Subscribe to Marquee Finance by Sagar to keep reading this post and get 7 days of free access to the full post archives.