The Historic "Unwinding"!

As we approach the monetary easing by the Western Central Banks (as predicted by Mr Market), there are ominous signs contrary to the expectations of the central bankers.

While inflation is proving stubborn and sticky on most parameters, the premature “dovish” pivot by the world’s largest central bank in December last year has resulted in a relentless rally in risk assets, leading to a historic easing of financial conditions.

On a lighter note, to give you an idea of where we have reached:

Nevertheless, the dual mandate of the Federal Reserve will be a headache as “maximum employment” will be contested by the data that implies the labour market is poised for gradual weakening.

In the East, the stage is set for unwinding the most significant monetary experiment in human history. One can’t ignore the repercussions of the end of the YCC (Yield Curve Control), QQE (Qualitative Quantitative Easing), and the likely end of the NIRP (Negative Interest Rate Policy) by the Contrarian Central Bank, a.k.a. Bank Of Japan (BoJ).

With the backdrop of “historic unwinding” that will begin from next week’s BoJ Policy, we got some intriguing macro data this week, which led us to do some rejig in our portfolio (discussed on chat).

Furthermore, as the political landscape heats up in the US, markets are becoming increasingly nervous about the long-term prospects of the debt binge that the US Government has addicted itself to.

Let’s begin by digging deep to comprehend the nuances of the macro data.

US!

The most awaited data point of the week was the US CPI. We have been mentioning since Q4 last year that the second wave is upon us.

Furthermore, last month, we wrote in detail the reasons for the rise in inflation.

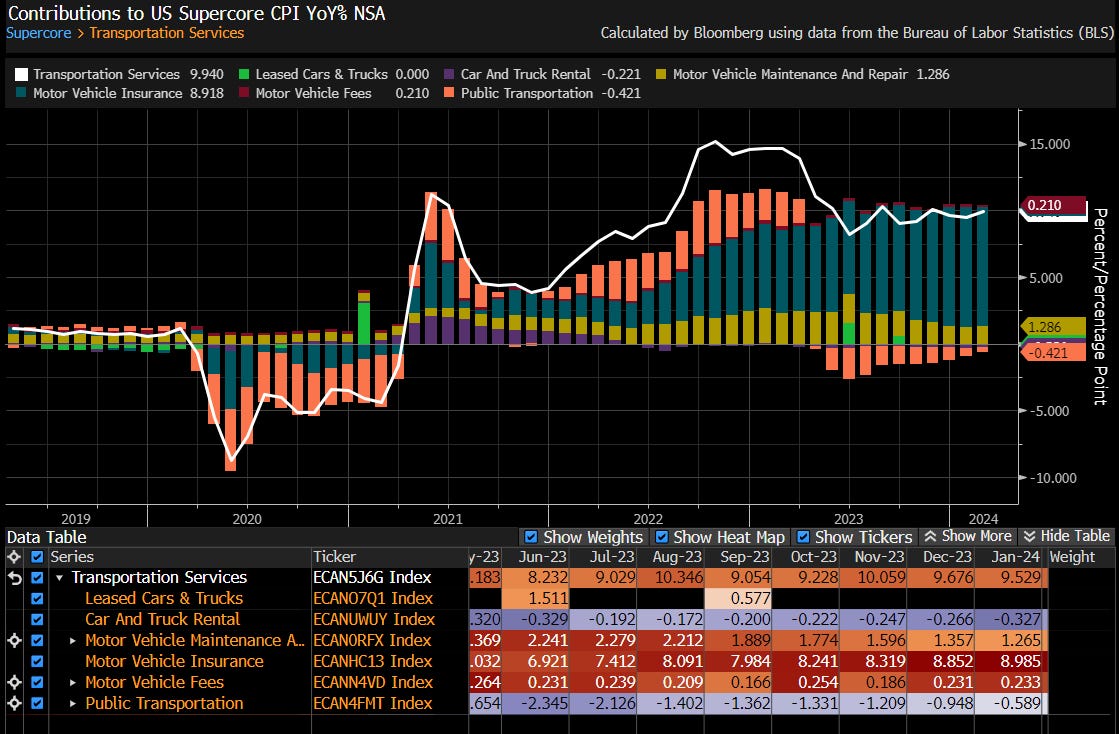

INFLATION!

The biggest concern is that the measure popularised by the Fed—in fact, the reason JayPo justified the last three rate hikes—was the sticky component of inflation: Supercore CPI (Services Ex Shelter).

While the Supercore CPI moderated from January’s enormous 0.8% MoM increase, the February print was still hot at 0.47%.

Whether you look at MoM, YoY or on a 3M, 6M annualised basis, there is no denying that the inflation is reaccelerating, and thus, January print was “NOT” a one-off.

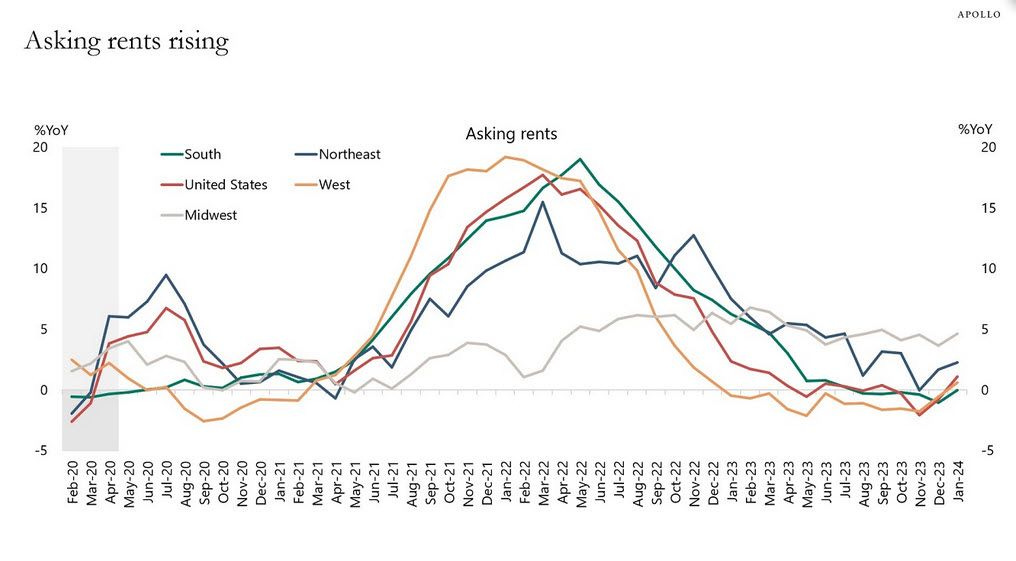

Furthermore, since the housing markets are buoyant with prices at ATH, rents have begun to rise in some places (bottoming out everywhere).

PS: To make matters worse, the Biden Admin has announced a rebate for purchasing homes, which will further fuel the fiscal deficits.

As a result, one or the other component of headline CPI will keep the number higher and way above the Fed’s 2% target.

Due to the stubborn nature of inflation, as per our forecasts, the June/July inflation print will be around:

Keep reading with a 7-day free trial

Subscribe to Marquee Finance by Sagar to keep reading this post and get 7 days of free access to the full post archives.