The Macro Shocker!

While many market participants believe that markets are immune to the macro developments, in the long run, most returns across various assets are attributed to the macro fundamentals of the economy and the business cycles in the developed world.

If one had not dug deeper into the macro fundamentals of countries like Argentina, Venezuela, Turkey, Egypt, etc., one would have lost a lot of money betting on these nations, once pitted as one of the best investment destinations in their respective continents.

In fact, in the developed world, macro matters a lot as these economies are driven by consumption, which depends on where we are in the business cycle.

Nonetheless, with narratives floating around like never before, getting the macro perspective of the world’s largest economy has become challenging.

From the US to Japan, we witnessed some of the most significant “macro” shockers of the recent past this week.

While a hot CPI print led to a minor shakeout, the GDP Data across Europe and Japan created ripples across the investment community.

The market’s positioning was skewed to one side with a perfect soft landing priced across assets (bonds, stocks, vol and credit markets). Thus, a hotter CPI led in the US to the unwinding of positions across the board.

As a result, markets aggressively priced out rate cuts from the curve (more than 80 bps of cuts).

Today, we will examine the macro shockers and comprehend where markets and the economy are headed.

PS: Before we begin, we wish to inform you that we will increase our paid subscription prices to $24.99/M or $ 249.99/Yr starting 1st March.

Note that the subscribers who are currently enrolled or will enrol by 1st March will be subscribed at the mouth-watering current prices ($14.99/$149.99) “FOREVER”.

So, somebody who wants to take advantage of a massive 40% discount for a lifetime can subscribe till midnight on 29th Feb at the current prices.

US!

The week's highlight was the US CPI reaction and the market’s response to the “hot” number. There was a lot of debate about how the “lagging” OER Rents was the most significant contributor to the upside surprise, and market participants even suggested that the January data was an outlier and should be ignored as the disinflationary trend is intact and the “soft landing” is in process.

Nonetheless, we will be very specific and look at the Fed’s “preferred” measure to interpret the CPI data and analyse the market’s reaction.

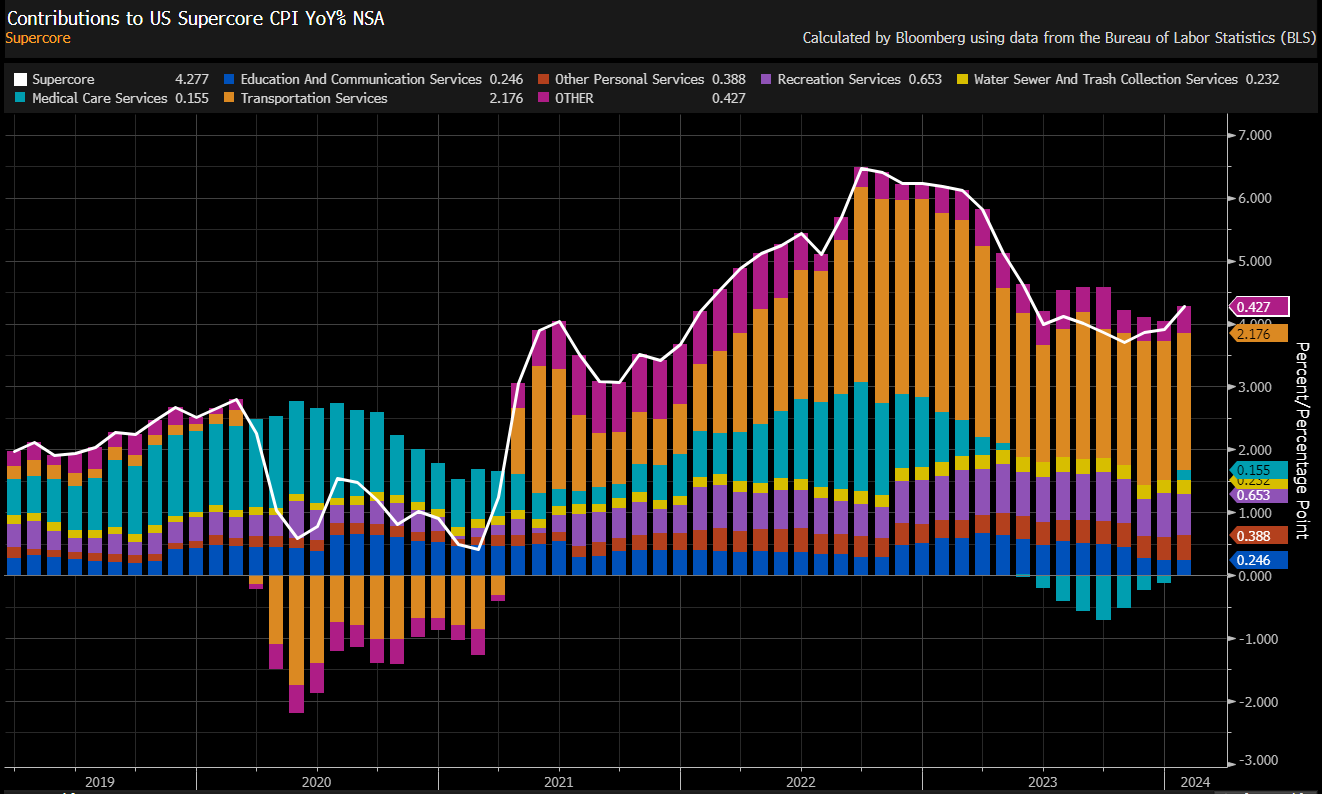

Ironically, the “Supercore” CPI, popularised by JayPo, doesn’t include the “Shelter” anomaly and is focused on Services Ex-Housing.

As we mentioned last month, there is no money for guessing that the Supercore has bottomed out. As we can observe, it inched significantly higher as the negative contribution of “Medical Services” vanished.

Long-time readers would appreciate that we extensively wrote in November and December that medical care services would turn positive and lead to higher super core.

However, what today matters is the future trajectory of inflation, as trillions of dollars are at stake. To simplify, this chart makes it clear where we are heading.

Keep reading with a 7-day free trial

Subscribe to Marquee Finance by Sagar to keep reading this post and get 7 days of free access to the full post archives.