The Macro "Train Wreck"!

“We are not looking for inflation to go all the way down to 2%, but we do need more evidence”: Jerome Powell, 6th March 2024.

Since the end of Bretton Woods, particularly since the 2008 GFC, governments worldwide have gone on an unprecedented debt splurge to revive growth and inflation.

The Debt pile (primarily the US) was compounded post-COVID as the world’s largest economy ran (and continues to do so) enormous peacetime deficits of more than 6-7% of the GDP.

Economists commonly use a metric known as the marginal productivity of debt to understand how debt issuance affects economic growth. For every dollar of debt issued, the corresponding increase in GDP is calculated.

Guess what?

In Q4 last year, the US government’s debt pile grew by more than $880 billion while the GDP grew by just $329 billion. This indicates that productivity is down the drain as it requires more debt than ever to generate a single dollar of GDP growth.

Furthermore, it’s not rocket science, but it's pretty clear that the GDP growth will be buoyant if the debt binge continues unabated.

This is the primary reason markets are extremely worried. Thus, we are witnessing parabolic moves in some inflation hedges, such as gold and BTC.

Today, we will further explore what’s driving the strange price movement across assets and, in a new format, discuss the macro developments (what we guided, where we are and what the future guidance is).

US!

Last week, we got the crucial PCE data, which is the Fed's preferred measure.

JayPo has explicitly mentioned that he will be comfortable only when the core PCE sustainably reaches its target of 2% (unlike this week when the narrative changed due to political compulsions?)

While the Core PCE came in at 2.8%, and the trend has been encouraging, the worrying factor in the report, which the markets ironically shrugged off completely, was the Services Ex-Housing (a measure popularised by the Fed itself).

The markets have already cheered the Core Goods disinflation by pricing in a “perfect” soft landing.

Any reacceleration in the Core PCE above 3% can spoil the party at Wall Street.

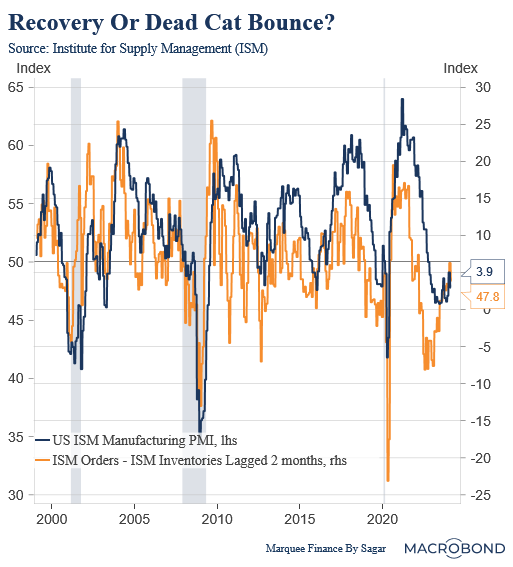

We also got the ISM Manufacturing shocker, which came in below estimates.

We have repeatedly mentioned that a single reading doesn’t confirm the trend, and we need multiple readings below the critical level of 45 or above 50 to confirm the direction of the cyclical economy.

Our favourite measure, Orders Less Inventories, also fell; thus, we must be wary of further lower readings.

What We Guided?

Keep reading with a 7-day free trial

Subscribe to Marquee Finance by Sagar to keep reading this post and get 7 days of free access to the full post archives.