Don't Fight The........Fed!

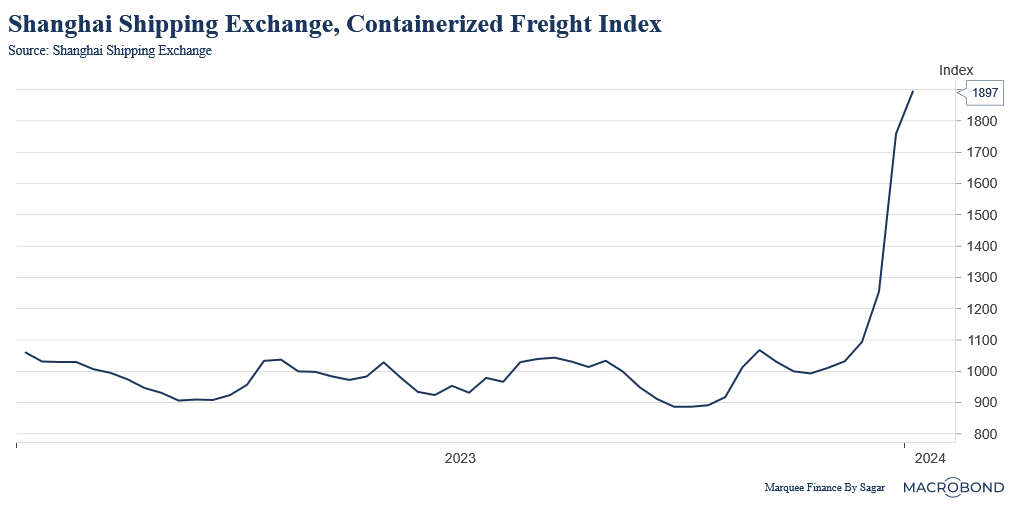

Last week, we wrote about “The Disruption” and how elevated geopolitical risks have the potential to spill over to broken supply chains “IF” the disruption is prolonged.

Nonetheless, we couldn’t have imagined in our wildest dreams that the disruption would begin as soon as this week.

Tesla halted production in its Berlin factory for two weeks due to a lack of components as the Red Sea disruption took a toll.

Furthermore, one of the world’s largest shipping companies, Maersk, raised significant red flags:

“It could potentially have quite significant consequences on global growth...At this time when inflation is a big issue, it’s putting inflationary pressure on our costs, on our customers, and ultimately on consumers in Europe and the US.”

As we strive to become better investors/traders, one lesson we should remember is to remain unbiased and join the dots across the spectrum.

One thing that we notably missed out on last year (and even discussed in Report Card 2023) was the liquidity circumstances in the US.

Though we gave high preference to global liquidity and repeatedly pointed out the disconnect between West and East (West sucking out and East pumping), the finer details were as important as the more comprehensive global liquidity framework.

Today, we will look at the nuances of liquidity, which becomes super important in light of the recently released Fed minutes and statements of Fed members, which sparked the rumours of an imminent restart of the QE program in 2024.

The end of QT and the likely beginning of the QE program have widespread implications for the cross-asset markets.

Let’s make sense of the economic data released globally and dip deep into the liquidity outlook!

PS: We also initiated multiple positions this week, with one partial profitable exit of 15%.

US!

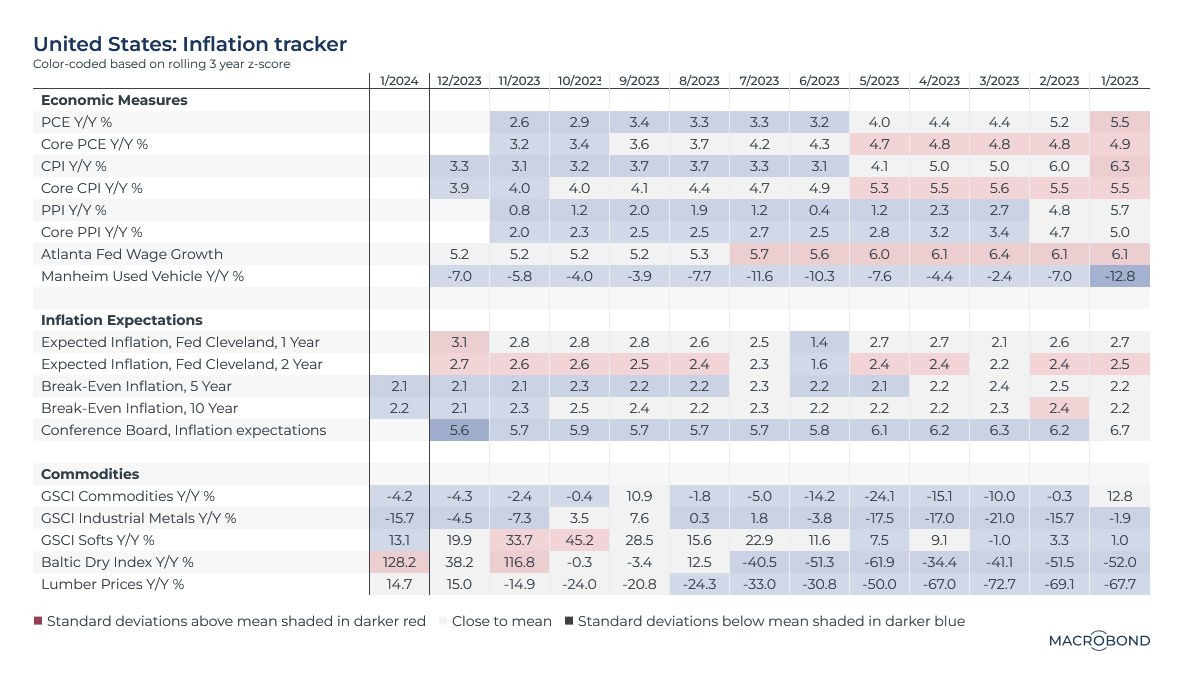

The much-awaited CPI data in the US came in slightly hotter than expected, 3.4%, primarily due to the “lagging” shelter costs, which refuse to bulge down.

Our most important takeaway was that despite a significant base effect (December 2022 YoY inflation was 6.5%), inflation came in above estimates.

As the base effect wanes by the end of Q1, inflation can spring a big surprise, especially if crude spirals up and the disruption in the shipping routes continues unabated.

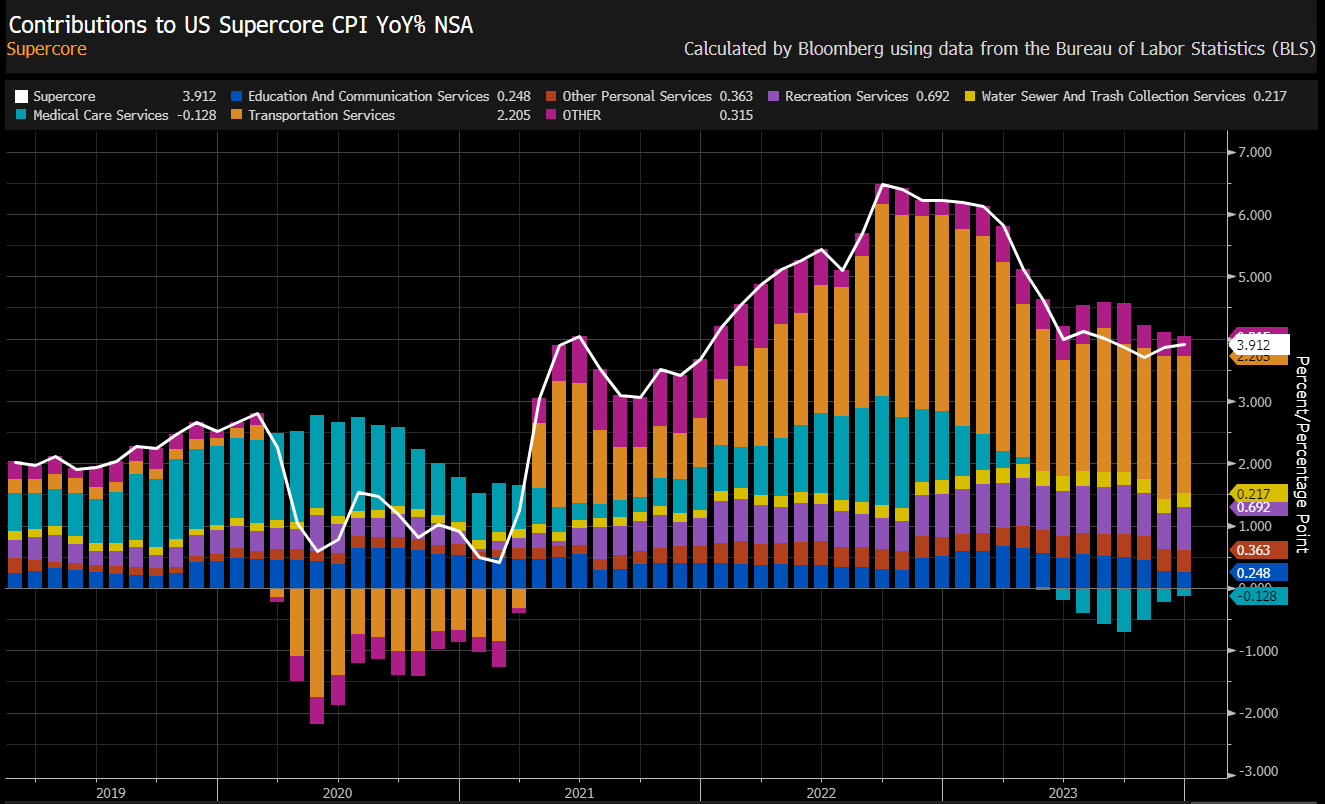

Digging further, Fed’s preferred Supercore CPI inched higher after stabilising at 4% mark.

The “sticky transportation services” is leading the gains while medical services, which can rebound anytime, is being a headwind.

Now, let us move to the highlight of this week, which I want to cover in detail.

Earlier this week, the Fed minutes came out, which sparked a risk on move across markets.

The statement that led to the move:

Keep reading with a 7-day free trial

Subscribe to Marquee Finance by Sagar to keep reading this post and get 7 days of free access to the full post archives.