Eric Basmaijan is the founder of EPB Research, who has done a remarkable job in the past few years and developed an actionable and systematic macro framework for identifying the business cycles in the US.

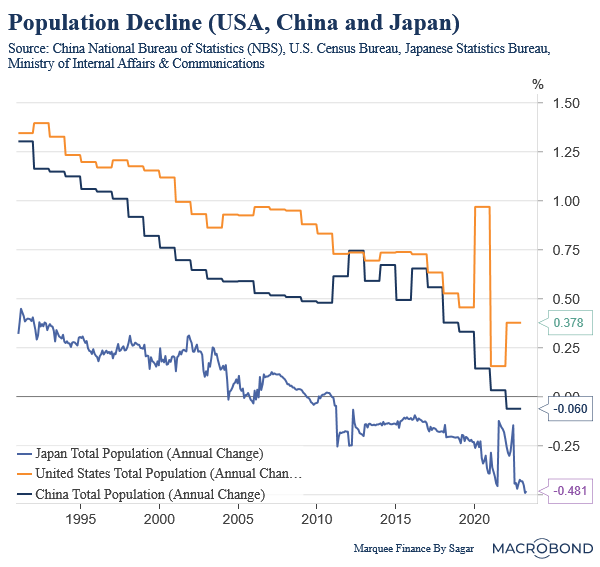

Timestamp: 0.50 mins (Demographics: Secular Trend)

We started by discussing the secular trends in the global economy. Lately, we have seen that declining demographics have become evident since the beginning of the century in Japan and in Europe.

In fact, China last year, for the first time, reported more deaths than births.

Eric said that demographics is the most critical trend to analyze when looking at a country's long-term growth, potential or inflation.

According to him, in the last four-five decades, the world's biggest economies: Japan, the US and China, obtained most of their growth from a real estate-based construction model.

And as the depopulation occurs, the real estate model collapses, leading to below-trend growth for decades and delivering a tremendous deflationary impulse (for example, Japan and China).

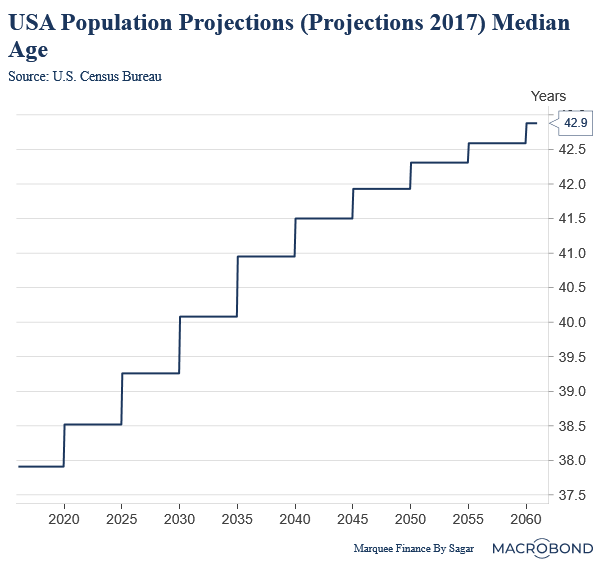

Timestamp: 6.20 mins (US Demographics)

When we look at the US, it’s still witnessing positive population growth. But, according to Eric, the population growth across the 15 to 64-year-old bracket (which matters the most) is seeing flattish growth, and the birthrate has fallen far below the replacement rate. Thus it’s too late to turn the ship around.

Nevertheless, he believes the magnitude of depopulation in the US will be lower than what we have seen in Japan and Europe.

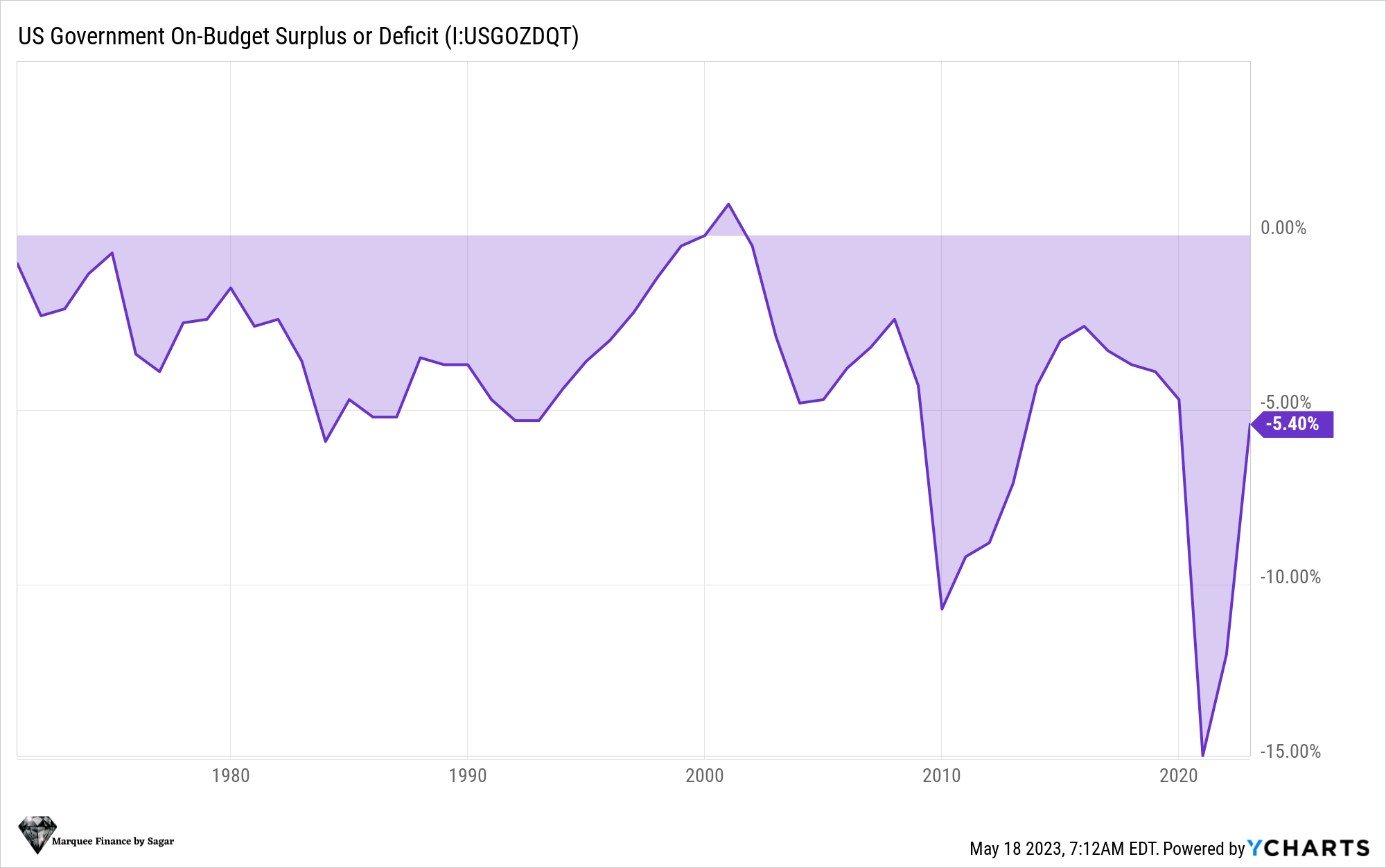

Timestamp: 10.40 mins (Path of Fiscal Policy)

As per the US Census Bureau, the median age in the US will climb to 43 by 2060 from the current 38. This will have far-reaching consequences for the government. This will likely lead to burgeoning social security needs, low savings rates and thus, a higher deficit for the government.

Eric believes that there are three possible paths for fiscal policy.

Government can cut spending by scaling down entitlement benefits which is, however, politically challenging.

Government can increase taxes but doesn’t curtail the benefits.

Fund the rising costs with ever-increasing deficits!

As per Eric, in all of the above three outcomes, we will end up with a lower real GDP growth rate and a worsening standard of living.

Nonetheless, he believes the third outcome will be the worst for the economy.

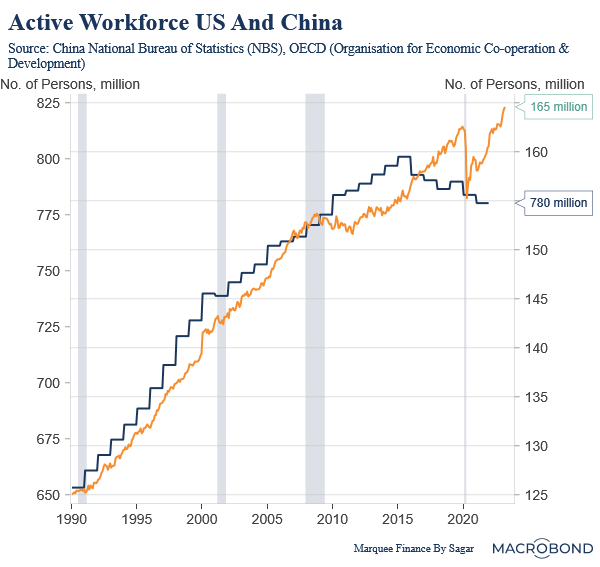

Timestamp: 16:15 mins (Labor Market: Secular Trend)

One of the most considerable deflationary forces post-2001 was China being the world's industry and the cheap labor (globalization) a tailwind for lower “global” inflation.

Nevertheless, the active workforce peaked in China in 2015 and has been since decreasing, which will also be a reality in the US in the next few years.

However, with technological advancements such as AI and Machine learning, we may get enormous productivity gains which have the potential to outweigh the labor shortages.

On this topic, Eric believes that in the last decade, a large part of the global economy (Japan and Europe) was in a quasi-recession.

He believes that there will be a significant deflationary impulse from China as the demand for industrial commodities wanes, which will likely offset the labor shortages.

Furthermore, the productivity gains will also offset the inflationary impulse arising from the reduction in labor force.

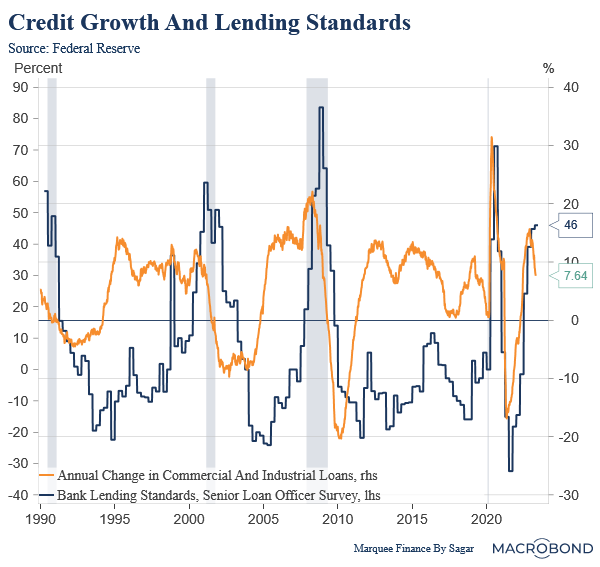

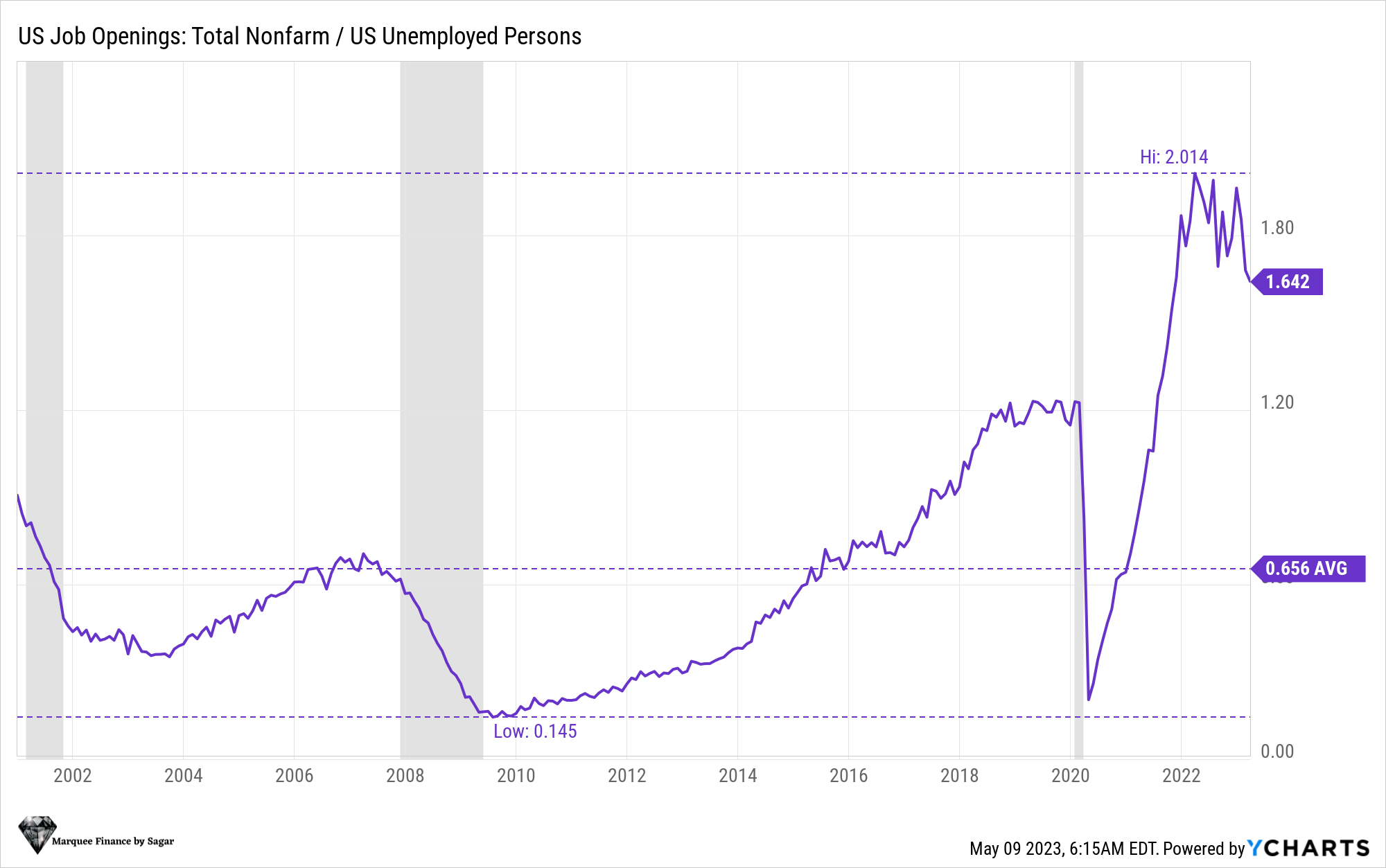

Timestamp: 20:40 mins (SLOOS)

Then we discussed the Fed’s Senior Loan Officer Opinion Survey (SLOOS), which reported that 46% of the banks have reported tightening lending standards. In fact, the highlight was the divergence in auto, CC, and personal loans, which saw an uptick in demand, while the C&I loans witnessed a contraction in demand.

Here Eric concurs with my view that the divergence between auto, credit cards and personal loans is because the broad labor market has not deteriorated to the extent expected in early recessionary periods.

However, he believes we are witnessing initial signs of cracks in the labor market. Furthermore, according to Eric, the final leg of credit tightening will happen when the labor market officially starts to decline, which always occurs in the middle of a recession.

Timestamp: 28.35 mins (Housing)

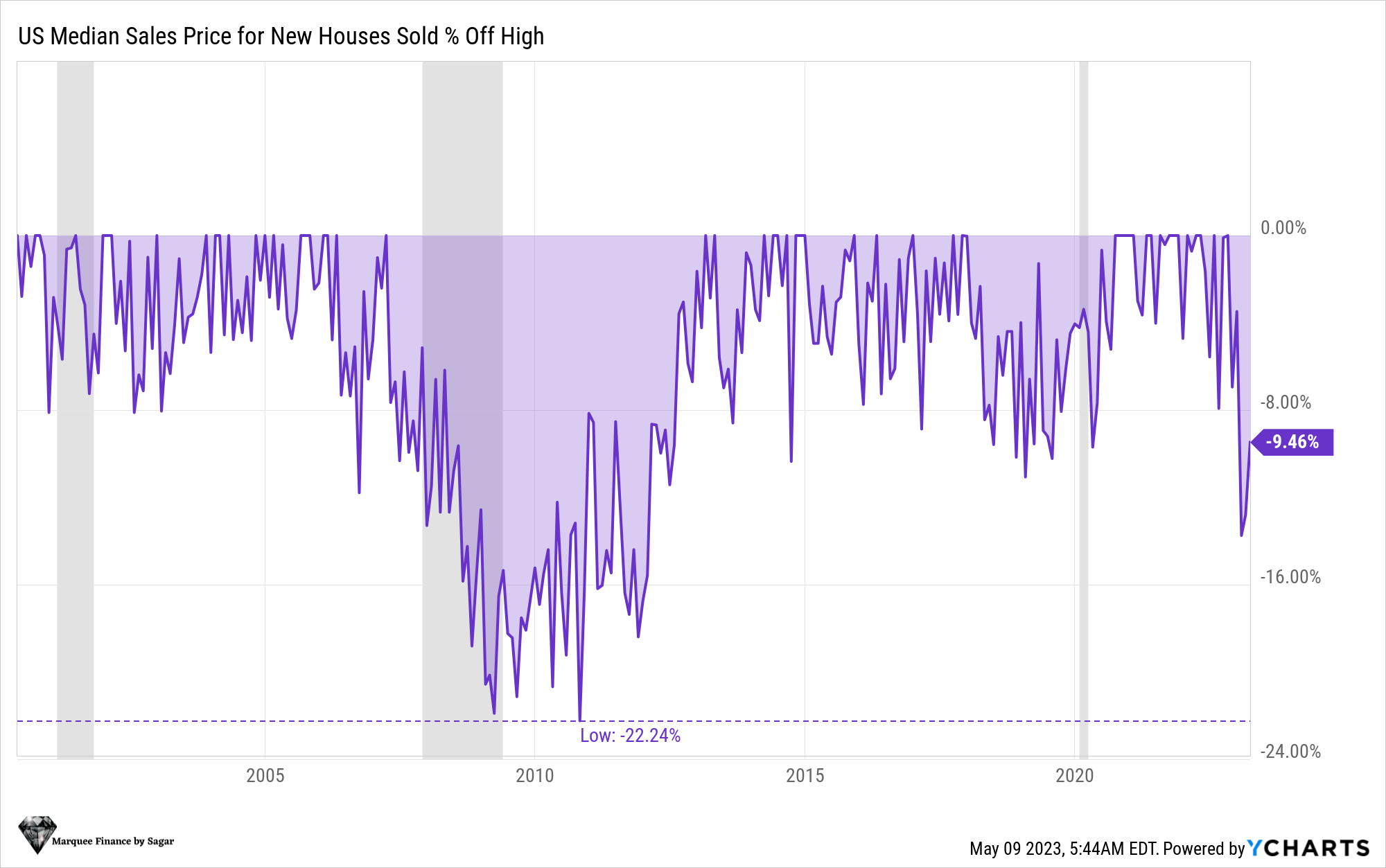

Eric has done some really deep dives into the housing sector in the past two years. Last year, Eric guided for a correction of around 15-20% in the median price of new homes. While the median price for new homes witnessed a drawdown of 14% and is now rebounded, the Case Shiller Index is down around 5% from the peak. Furthermore, months of supply is now down to 6 months.

Eric believes that since mortgage rates have stabilised, housing activity has recovered from the lows as buyers get more comfortable with the new reality.

He further stated that as and when the labor market deteriorates, we would get a second leg of decline in demand and a significant increase in inventory.

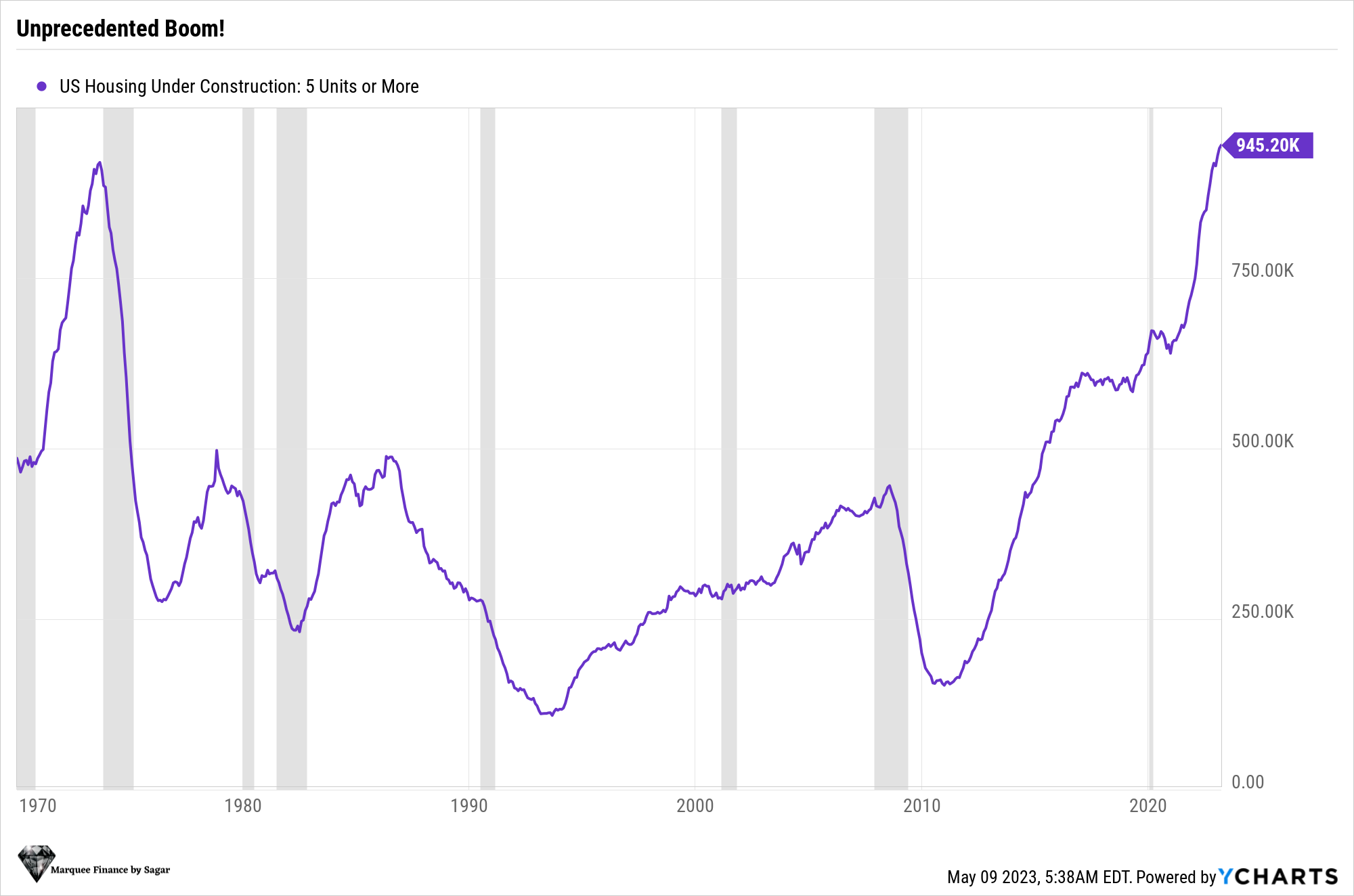

Timestamp: 33.30 mins (Multi-Family Housing)

While single-family housing peaked last year and has been downward trending since last year, multi-family housing continues to witness an unprecedented boom.

Eric suggests that there was a significant migration of people from New York and California to Florida, Texas, and other low-cost areas, which led to a lot of speculative building. This led to an increase in demand for housing, but it also led to oversupply.

Eric refers to the analogy of speculative real estate boom along the canals in the 1800s mentioned in the book Mania's Panics and Crashes by Charles Kindleberger.

He also mentions that price declines will be very granular, unlike the homogenous fall we witnessed in the 2008 GFC.

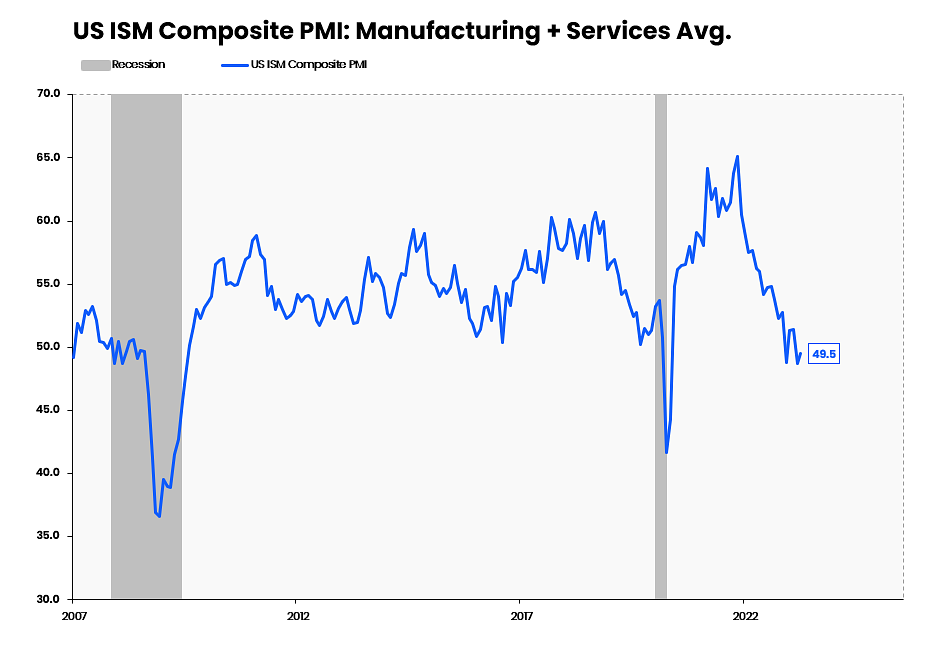

Timestamp: 40.50 mins (ISM)

The other leading indicator that Eric closely tracks is the ISM numbers. The latest ISM reading suggests that it has started rising. Furthermore, consumers are still flush with excess savings up to the tune of $500 billion, helping consumption.

Eric is of the view that three factors are holding up ISM:

First, the new orders component is falling dramatically.

Second, production is still holding up as manufacturers work off some of their backlogs.

Third, the employment number is hovering around 50 and hasn’t fallen significantly as residual production keeps the number higher, causing employers to hold on to staff a little bit longer.

As a result, Eric believes the ISM will trend lower once the backlog is cleared across the industries.

Timestamp: 44.30 mins (Inflation)

CPI data was released last Wednesday, and there is a raging debate that inflation might remain sticky as labor market remains tight and AHE is still hovering above the 4% mark. As a result, we might head into a stagflationary scenario.

Eric is a big believer of Money-Price-Wage spiral. As the monetary aggregate contracts, prices correct, and the wage pressure ease. Furthermore, according to him, inflation will only reaccelerate if various monetary aggregates start to shoot higher.

PS: Eric looks at real growth, not the nominal growth in monetary aggregates, which the social media is abuzz with.

Timestamp: 52.15 mins (Asset Allocation)

Lastly, I asked Eric about the asset allocation for a portfolio during a recession.

Eric says that he believes that by the time this recession is over, interest rates will be at 0% or close to 0%, and thus one with a risk appetite can look to buy long-term bonds.

Risk-averse investors can sit on cash yielding 4%+.

Last but not least, Eric believes there is a 50%+ probability of a hard landing.

It was a really interesting discussion, and I hope you enjoyed it as much as I did.

Do check out the community at EPB Macro (Click Here)

Disclaimer

This publication and its author is not licensed investment professional. Nothing produced under Marquee Finance by Sagar should be construed as investment advice. Do your own research and contact your certified financial planner or other dedicated professional before making investment decisions. Investments carry risk and may lose value; Marqueefinancebysagar.substack.com or Sagar Singh Setia is not responsible for loss of value; all investment decisions you make are yours alone.

Share this post