The "Masterplan"™!

“Every empire, however, tells itself and the world that it is unlike all other empires, that its mission is not to plunder and control but to educate and liberate”. Edward W. Said.

History is reminiscent of the fact that the foundation of empires is built on expansionist policies. Notably, whether it is the British Empire or any other empires from ancient history to medieval to modern, the world’s most powerful countries of their times extended their clout in resource-rich territories.

Post the breakup of the Soviet Union, the US became the undisputed leader of the uni-polar world and the territorial gains continued in the “energy” rich Middle East. Nevertheless, with the admission of China into the WTO and its successful transformation into the manufacturing hub of the world, China became the biggest hoarder of the greenback.

Post the Global Financial Crisis 2008, China using its “mega” state-owned firms like PetroChina and Sinopec, began to dominate the worldwide acquisitions of energy assets and other commodities to “secure” its burgeoning energy needs. However, the pretext of “energy security” continued, and under the leadership of President Xi, China stunned the world by unveiling its mega “expansionist” policy: “One Road, One Belt Project”.

The “Debt-Trap Diplomacy” gathered pace, and the seeds of it have started to bear fruits as the might of Chinese influence over countries like Pakistan, Srilanka, and other African countries are visible.

Post-war, China has now initiated one of its most ambitious policies ever. The implications of the recent Chinese moves will be far-reaching and can’t be overlooked at any cost.

Today, we will dig deep and understand the Chinese Masterplan™, which can potentially disrupt the lifeline of our world.

Disrupting The Commodities Trade?

Iron Ore is one of the most crucial raw materials vital for producing steel, and you guessed it right, nothing can be built without steel. China is the largest iron ore importer and the largest steel producer, as decades of breakneck GDP growth were fuelled by enormous construction and infrastructure activity.

We can observe that Australia, Brazil, China and India tightly control iron ore production.

Even after its humongous production of 380 million tonnes, China imports 1.1 billion tonnes of iron ore every year to feed its guzzling steel industries, thus consuming the majority of iron ore produced worldwide.

Nonetheless, the recent actions unveil how China wants to upend the $160 billion global iron ore trade.

Similar to its large state-owned energy firms, China recently formed the China Mineral Resources Group (CMRG), which will buy iron ore on behalf of the 20 largest steel companies in China.

This step will make CMRG the world's largest iron ore buyer. As a result, CMRG will call the shots in the global iron ore market and will have unprecedented power to influence the pricing of the commodity.

The buck doesn’t stop with iron ore; it is an emerging trend which will put China in the driver’s seat as long as commodities are concerned.

Upheaval In The Natural Gas Markets?

You won’t believe me, but if Europe’s energy fate rested in Russia’s hands last year (before the weather Gods showered their blessings on Europe to steer out of one of the worst crises since WW2), this year it’s China which will determine whether Europe will be able to secure its energy supplies.

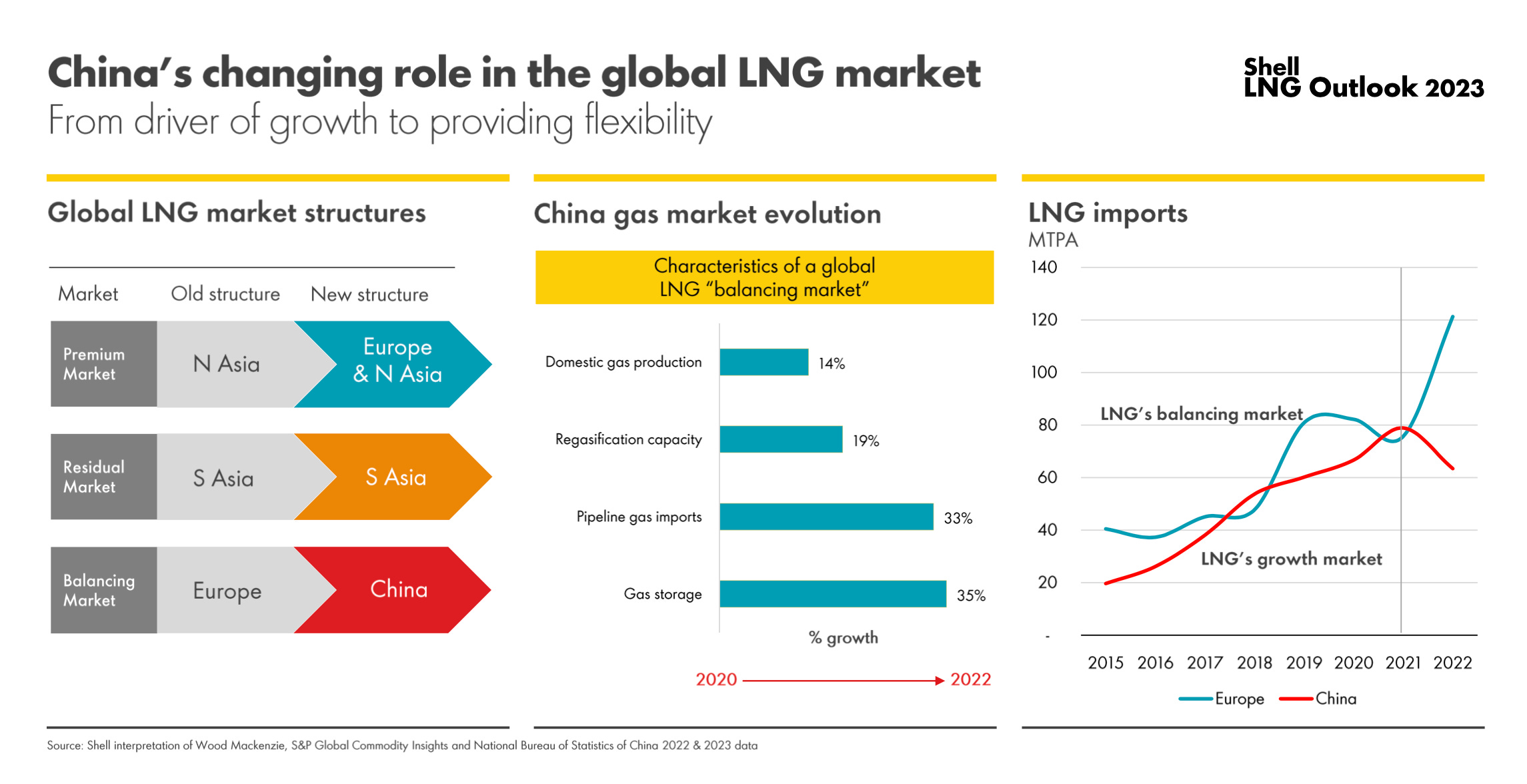

In its annual LNG Report, which is a must-read for the energy guys, Shell mentioned that: “China is evolving from being a rapidly growing import market to playing a more flexible role with an increased ability to balance the global LNG market”.

This statement by Shell can be cemented by the fact that China resold a whopping 5.5 million tons of LNG1 last year, contributing to roughly 6% of the total spot market volume. Moreover, China could resell huge volumes as lockdowns at home led to plunging domestic consumption.

We already know that lower Chinese LNG demand (I wrote this last year) helped alleviate the extreme stress in the LNG markets. All hell would have broken loose in Europe if China had been free from the shackles of the draconian covid zero policy.

Lower Chinese demand helped Europe to squeeze out the markets as LNG imports skyrocketed by a record 60%. However, 2023 will be entirely different as Chinese demand will witness a sharp rebound due to the reopening of the economy after multi-year lockdowns.

Nonetheless, the Chinese building LNG terminals and reselling LNG is one of the moving parts in its ambition to control the world’s energy supplies (along with other commodities).

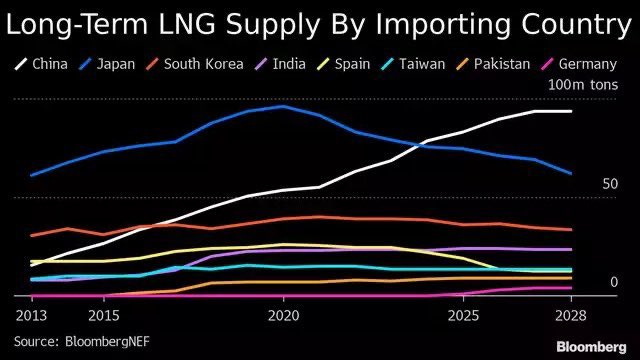

According to Bloomberg: “Firms based in China account for roughly 15% of all contracts that’ll begin delivering LNG supply through 2027.”

When we look closely, 80% of the incremental supply of LNG by 2030 will be from Qatar and the US, meaning that China is signing multiple contracts with US firms.

The plan is simple: Lock in the supplies by signing long-term SPA with producers around the globe and resell the LNG at profits while controlling a large part of the global trade.

But wait?

Don’t you need intermediaries to scout for buyers when you trade?

Well, China has plugged this loophole as well.

The influence of the Chinese state-owned energy firms Sinopec and PetroChina is observable as they have offices all around the globe in major trading units from Singapore to London.

It’s no brainer that a European buyer scouting for a US LNG shipment will have to contact the Chinese state-owned firm to receive cargo.

Furthermore, China has begun buying equity stakes in international trading giants responsible for global commodities trade.

In a recent development, Chinese state-backed investment fund CNIC bought a 5% stake in Swiss-based global energy giant Mercuria.

Note that Mercuria is one of the top five global oil traders, moving around two million barrels per day of crude oil and refined products.

Is Controlling Commodities Trade Part Of The Big Reset?

Spearheaded by Russia, BRICS countries have made it clear that they want to create an alternate currency backed by physical commodities.

The key to this incredibly never-tested currency system will be controlling the supply, transport and pricing of commodities, including energy. However, the energy part of the equation can be cracked if some of the petrodollar2 trade moves to yuan as and when MBS/Saudi Arabia decides to join the BRICS countries, as the geopolitical pundits predict.

Thus, we can conclude that China’s grand ambitions to control the commodities trade are part of the big plan which involves challenging the greenback hegemony.

Nevertheless, upending the colossal dollar trade is not easy as the current account surpluses countries like Russia, China, and Saudi will need to recycle their excess export earnings; and unfortunately there is no safe haven except the US Treasuries to park their earnings.

On the contrary, some geopolitical analysts are also speculating that the Chinese meticulously planned strategy indicates that it’s securing its energy security and commodity supplies in case sanctions are imposed against the world’s second-largest economy due to escalation in tensions against the West.

The grandiloquent plan of replacing the dollar with an alternate BRICS currency will take decades, but if we are indeed in a multi-polar world which will be marred by chaos and regional conflicts, then the role of the world’s superpowers will be of utmost significance to maintaining peace and stability.

Conclusion!

Chinese Masterplan™ to take “total control” of the worldwide commodities trade is an alarming trend. In a scenario where a flare-up of geopolitical tensions remains a high probability, China can choke the commodities supply, which can be catastrophic for the global economy.

In fact, China can resort to the weaponization of commodities (including energy) akin to Russia in retaliation for sanctions if the situation deteriorates.

Already, the might of China in the global supply chains is unmatched. We are very well aware that the South China Sea trade route is one of the most significant and busiest trade routes in the world. China has been proactively taking steps to increase further its influence, which has also led to occasional skirmishes in the Indian Ocean.

The proliferation of state-backed Chinese firms in trading major commodities, including oil and gas, and the desire to influence the pricing can lead to an uncertain environment prone to exogenous shocks.

As the world gears up for the transition to EV and green energy, the role of commodities will be super important (I covered it in detail in “First Come First Served”), and one can’t ignore the Chinese moves.

Generally, uncertainty entails a “premium”, and I will not be surprised if, in the coming future, commodities start to price in the “Chinese Risk Premium”.

Disclaimer

This publication and its author is not licensed investment professional. Nothing produced under Marquee Finance by Sagar should be construed as investment advice. Do your own research and contact your financial advisor before making investment decisions.

Liquefied natural gas (LNG) is natural gas that has been converted to a liquid form for the ease and safety of natural gas transport. Natural gas is cooled to approximately -260 F, creating a clear, colourless, and non-toxic liquid that can be transported from areas with a large supply of natural gas to areas that demand more natural gas. Source: Investopedia

Petrodollars are crude oil export revenues denominated in U.S. dollars. Petrodollars are not a distinct currency; they are simply U.S. dollars accepted as payment by an oil exporter. Global crude oil exports averaged approximately 88.4 million barrels per day in 2020.2 That pace would generate an annual global petrodollar supply of more than $3.2 trillion annually, assuming an average price of $100 per barrel. Source: Investopedia

Awesome article 👏